In Mid-March The North America Construction Framing Dimension Softwood

Lumber Market Turned; From The Habit Of Just-In-Time Buying, To A Start Of

Stocking Inventory.

As better weather finally began to materialize across the continent, demand

for solid wood products increased which sent lumber prices higher. Sentiment

still remained very much toward caution, so the actual sales volumes

continue to be lower than normal in advance of the spring construction

season.

Most of the wisdom regarding US new home building for this year is for

ongoing muted activity.

There is a significant amount of lumber manufacturing volume able to come

back online at sawmills across Canada and the US, as capacity utilization

rates trend

experienced a meaningful drop from previous years. As true home building

gets going this year, it will become more clear how much actual demand there

will be for wood.

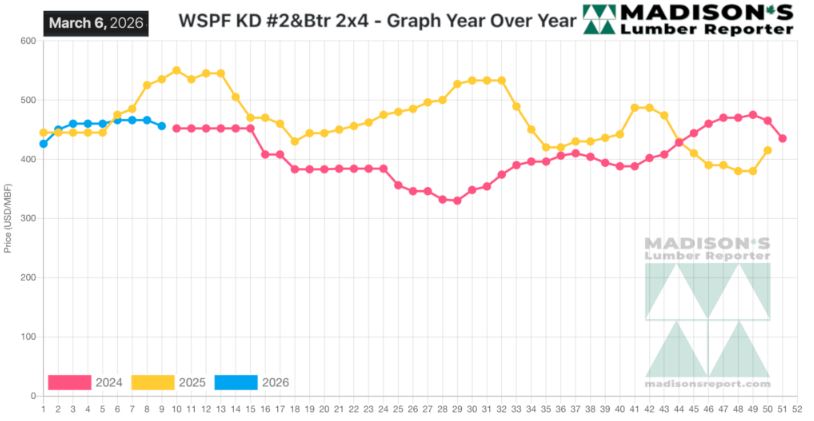

In the week ending March 13, 2026, the price of benchmark softwood lumber

item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$466 mfbm. This was up

+$10, or +2%, from the previous week when it was $456, said weekly forest

products industry price guide newsletter Madison’s Lumber Reporter.

That week’s price was up +$2, or +0%, from one month ago when it was $465.

Compared To The Same Week Last Year, When It Was Us$550 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending March 13,

2026 Was Down -$84, Or -15%.

Compared To Two Years Ago When It Was $452, That Week’S Price Was Up +$14,

Or +3%.

Lumber traders had an increase in inquiry, as on-ground prices showing

signs of strengthening. Freight rates rose precipitously week after week.

KEY TAKE-AWAYS:

The Western-SPF market in the US was driven by short supply.

Improved business south of the border precipitated a wave of demand for

Western-SPF material in Canada.

Sawmills maintained order files within a two- to three-week range.

Producers were much more firm on their numbers than in recent weeks.

Price concessions were increasingly relegated to secondary suppliers.

In Western Canada trucking capacity again required advance scheduling;

exacerbated by driver shortages typical for the season.

As cheap street prices evaporated in the US southeast, demand naturally

flowed to Eastern-SPF.

Sawmills in the northeast were reluctant to push their order files further

out than late-March, as prices there remained soft.

Sales of Southern Yellow Pine pivoted as customers became more focussed on

covering forward inventory positions.

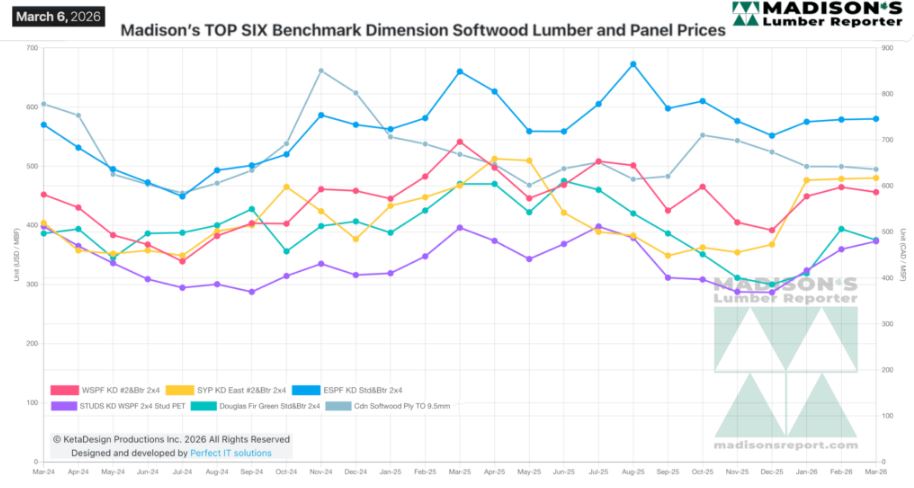

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: