September has waned, and as this autumn dawned north american construction

framing dimension softwood lumber prices levelled off.

The downward corrections into summer’s end reversed to close September up

slightly. Indeed; current levels were almost even to the start of this year

as well as closely matching the same weeks last year and in 2023.

This is a return to historical price trend, with regular swings up and down

throughout the year as construction increases then slows down for winter.

Ongoing questions by industry folks over the past two years of what are the

new price highs and lows seem to be answered.

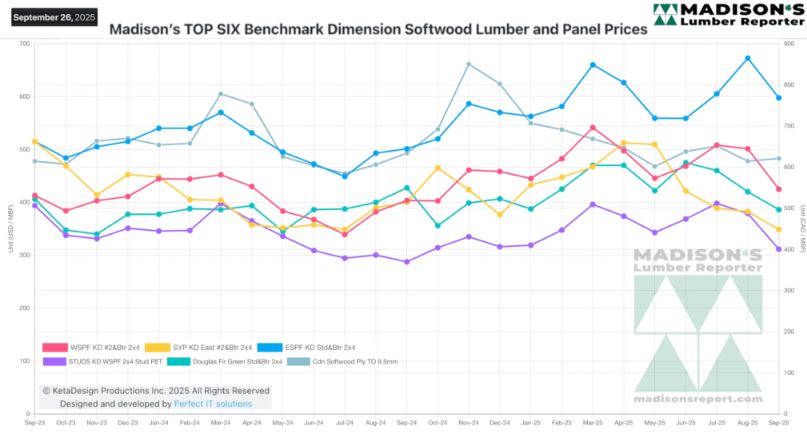

This year the annual price cycle ranged by approximately $160 mfbm,

providing good price stability for operators.

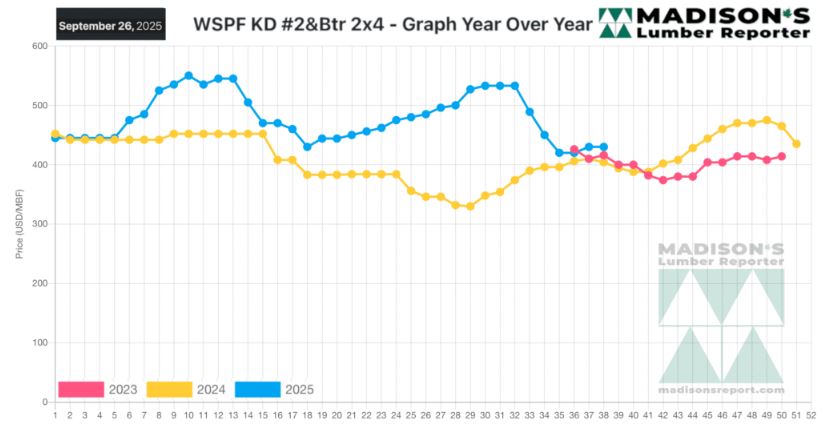

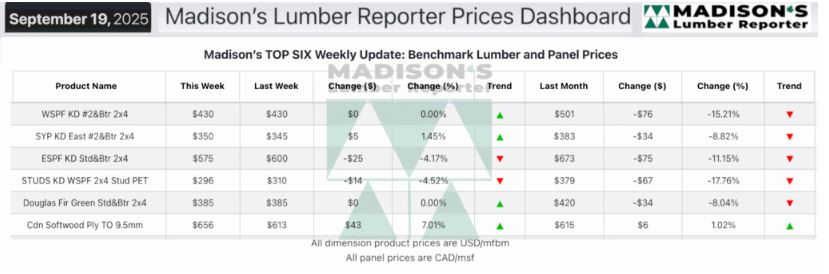

In the week ending September 26, 2025, the price of benchmark softwood

lumber item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$430 mfbm. This

was flat from the previous week when it was $430, said weekly forest

products industry price guide newsletter Madison’s Lumber Reporter.

That week’s price was down -$71, or -14%, from one month ago when it was

$501.

Compared to the same week last year, when it was us$404 mfbm, the price of

western spruce-pine-fir 2×4 #2&btr kd (rl) for the week ending September 26,

2025 was up +$26, or +6%.

Compared to two years ago when it was $416, that week’s price was up +$14,

or +3%.

..

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Suppliers of Western-SPF in the United States reported sales only marginally

improved.

Western-SPF sales in Canada gained traction on perception that prices had

bottomed out.

Large national producers were able to extend their sawmill order files and

refuse most counteroffers.

Eastern-SPF sellers had their heads on a swivel, with weakening prices,

tight availability, and low field inventories.

Last-minute purchasing was still common as buyers had gotten used to finding

what they needed for quick shipment with ease.

Southern Yellow Pine commodities firmed as mills held their prices steady

and didn’t chase counters as stridently as in September.

Supply accumulations were mostly cleaned up, SYP suppliers had leaner

inventories.

Eastern stocking wholesalers were frustrated there wasn’t much time for

autumn construction before snow starts to fly.

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source:

madisonsreport.com

More Reports: