As Canadian Operators Were Off For The August Long Weekend Holiday, Sales Of

Lumber Across North America Remained Muted.

Customers in the US south had pre-ordered wood from the north and west to

arrive before the full force of softwood lumber duty came into effect this

month. Demand flowed mostly to reloads and wholesalers, with new orders

placed at producers still mostly for fill-in needs only.

Even with that, sawmills in most regions reported order files at one-to-two

weeks. This largely because manufacturing was being kept at lower volumes to

stay in line with soft demand. Wildfires continued to burn in northern

Manitoba,

while new raging forest fires sparked on the east coast of Canada in New

Brunswick and Newfoundland/Labrador.

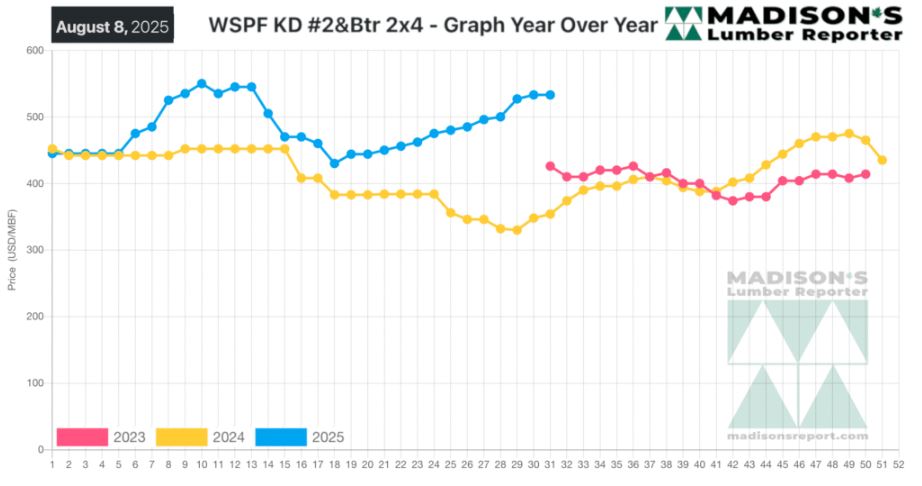

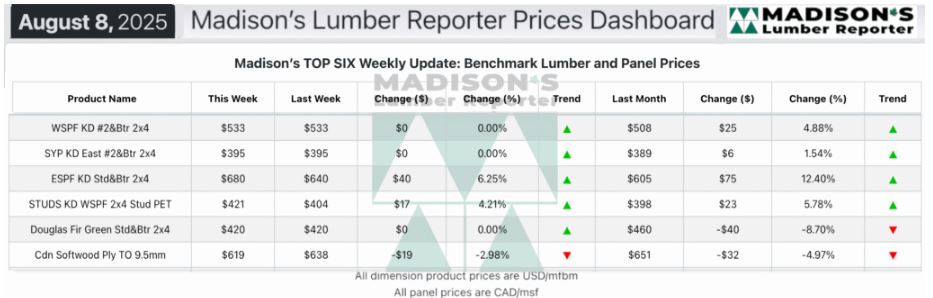

In the week ending August 8, 2025 the price of Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was US$533 mfbm, which is flat from the previous week when it

was $533, said weekly forest products industry price guide newsletter

Madison’s Lumber Reporter.

That week’s price is up +$25, or +5%, from one month ago when it was $508.

Compared To The Same Week Last Year, When It Was Us$354 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending August 8,

2025 Was Up +$179, Or +51%.

Compared To Two Years Ago When It Was $426, That Week’S Price Was Up +$107,

Or +25%.

Already-subdued softwood lumber demand was further restrained by

previous and upcoming duty hikes on Canadian softwood lumber, as well as

lukewarm trends in broader economic indices.

.

..

KEY TAKE-AWAYS:

Traders of Western-SPF in the US were able to buy prompt lumber below market

value in some cases.

In Canada asking prices for Western-SPF remained firm as consistent takeaway

continued to put pressure on tight supply.

Canadian customers stuck to immediate coverage only, while US purchasers

were figuring out the new pricing landscape with higher duties factored in.

Sales of Eastern-SPF were tepid to start the week as Canadians were off for

the holiday Monday.

Eastern-SPF customers south of the border focussed on stateside material

that had crossed into US reloads before increased duties were implemented.

Demand for Southern Yellow Pine was unsure; with price softness appearing in

some products while others were firm.

With 7- to 10-day sawmill order files, producers in the US South tried to

hold onto their prices.

Bouts of sweltering heat put a damper on construction activity in the US

Northeast.

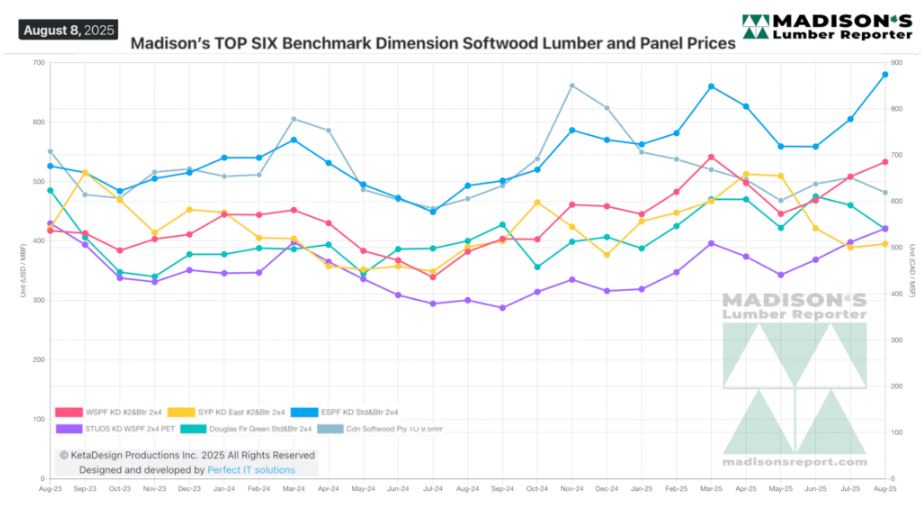

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source:

madisonsreport.com

More Reports: