|

1.

CENTRAL/ WEST AFRICA

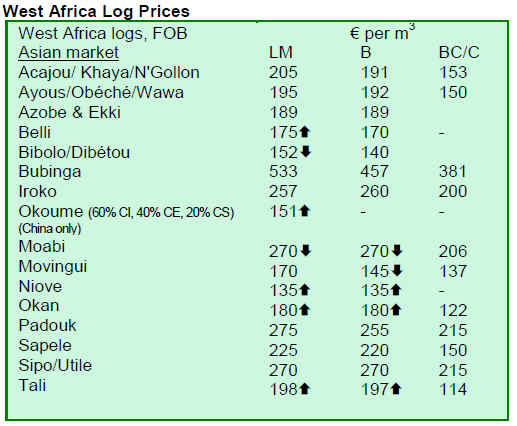

Prices for West African logs show slight strength

Over the last fortnight, prices for some West African log

species have shown some strength where there has been

demand from India, China and Vietnam. However, the

majority of prices were unchanged due to the dull market

conditions. A few species have shed around EUR3 to

EUR5/m³ or so through lack of buyer interest rather than

the result of actual sales. Demand has been only moderate

and exporters had no great expectations of any sudden

revival in the short to medium term, and production

remains at an ongoing low level.

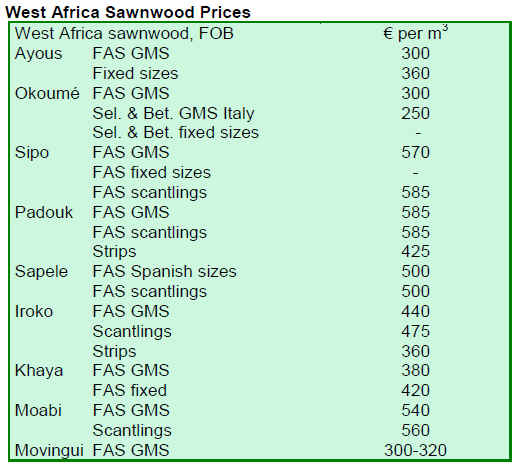

Europe was still very quiet and demand for logs for

traditional French and German buyers was extremely

limited. Sawn lumber prices were stagnant and seem likely

to remain so through the current quarter. Even the

European spring weather that usually turns buyers¡¯ minds

towards topping up stock levels for a more active phase in

building activity has this year not led to a rise in inquiries,

and even fewer new contracts. Sapele prices were still low,

while other prices seem once again to be unchanged. West

African sawmills in most areas have either closed or were

operating at low capacity. In other news, the Gabon

government released details of the 2009 log quota, which

is set at just above 1.5 million m³.

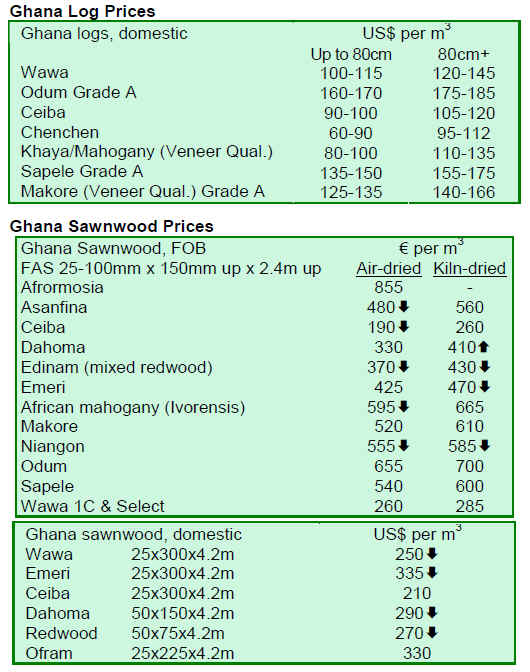

2. GHANA

Plywood contracts show gains in fourth quarter 2008

A total contract volume of 152,244 m³ and 9,507 pieces of

furniture parts were processed and approved during the

quarter under review. These represent drops of 10.2% and

38.2% respectively, when compared to the figures

achieved during the third quarter of 2008. With the

exception of plywood contracts, which increased 68.3%,

and were 75,882 m³ by volume, the volume of contracts

processed and approved for all major exportable products

fell during the quarter under review when compared to the

previous quarter.

Export volumes of lumber, rotary veneer and sliced veneer

decreased by 26.5%, 9.8% and 7.5% respectively. There

was a sharp drop in the export volume of

logs/poles/billets, which were 13,732 m³, representing a

decrease of 70.95% when compared to the previous

quarter. The difficulty in securing contracts from the

European and the American markets shifted the attention

of most integrated mills to the West African sub-region

where plywood is readily available. This resulted in a

high volume of plywood contracts being issued during the

quarter under review. Plywood contributed 49.8% to the

total wood products export volume.

The TIDD contract offices in Kumasi, Accra and Sunyani

processed and approved 14.5%, 0.5% and 48.5%,

respectively, of total wood products approved during the

quarter under review. These three offices together

contributed 63.5% of the total volume of wood products

approved. The high percentage of contracts attributed to

the Sunyani office was mainly due to the high volume of

plywood approved during the quarter. The office

approved 58,607 m³ of plywood, representing 38.5% of

the total contract volume.

Regarding price and market performance, prices were

generally down, especially during the last month of the

quarter under review. This has been attributed to the

global economic downturn and the credit crunch in

Germany, the UK, Italy and the US, the major destinations

of Ghana¡¯s wood products. Inquiries from most buyers

also revealed that this situation has seriously affected the

building industry, which is the main consumer of Ghana¡¯s

wood products. It has become very difficult to obtain

credit from financial institutions and debtors have taken

advantage of the situation by not paying for already

bought timber.

Prices generally dropped between EUR5/m³ and

EUR20/m³ below the TIDD minimum Guiding Selling

Prices (GSP) for lumber and rotary veneer. Odum lumber,

for example, fell as low as EUR40/m³ below the TIDD

minimum Guiding Selling Prices (GSP). Notwithstanding

the above, plywood to West African markets performed

notably well during the quarter under review. Depending

on the thickness, plywood prices increased between

USD10/m³ and USD50/m³ over the TIDD minimum

Guiding Selling Prices (GSP).

3.

MALAYSIA

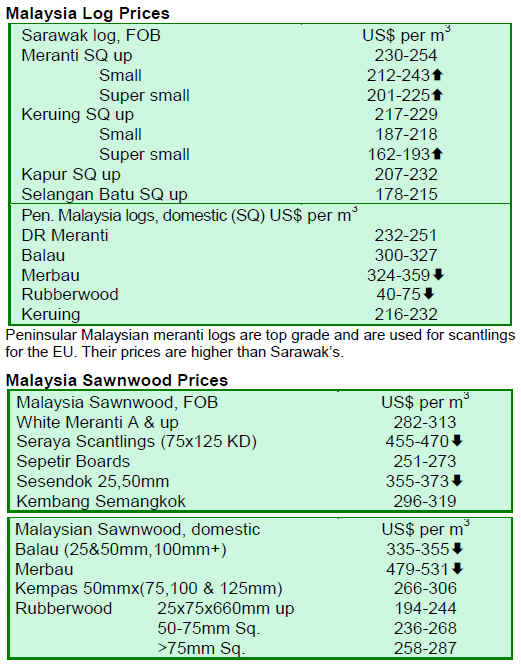

Sarawak state government reduces timber royalty

The Sarawak state government has reduced the 2009

timber royalty to a flat rate of RM50 for all timber with a

diameter of 30cm or more, reported The Star. The

reduction derived from an appeal by the Sarawak Timber

Association (STA), after the state forestry department had

increased the royalty to RM65 four months ago. However,

the government rejected STA¡¯s appeal for a 50% discount

on the timber royalty extracted from agri-conversion land

and for timber with a diameter of between 30cm and

40cm. The royalty will increase to RM55 by 2010 and

RM65 in 2011.

Minister expects exports to reach RM20 billion

According to Bernama, Deputy Plantation Industries and

Commodities Minister Mr. A. Kohilan speculated that

demand for Malaysian timber products from Central Asia,

India and Eastern Europe could help Malaysia achieve at

least RM20 billion in exports in 2009. He also said the

federal government has launched an afforestation

programme, which is managed by the Malaysian Timber

Industry Board (MTIB). A target of 25,000 ha has been

earmarked for afforestation yearly over a period of 15

years, which would result in a total of 375,000 ha

afforested. Fourteen companies are said to be participating

in this programme, with an area of nearly 60,000 ha

afforested to date.

Malaysia¡¯s exports fall 15.9% in February

Malaysia¡¯s exports fell 15.9% in February 2009, when

compared to February 2008 exports, as reported on

CNBC.com. Exports in January 2009 declined 27.8%

compared to the previous year, the steepest decline in

nearly 30 years. Economists commented that the current

economy is performing better than predicted, but

cautioned that a decline in exports at least over the next

few months will hover in the realm of 20%.

Timber prices steady but may not hold

Prices of Malaysian timber products remain weak but

steady as thunderstorms continue to hammer the country,

making timber extraction difficult. However, prices are not

expected to hold. Foreclosures of both private and

commercial properties were on the increase in the wake of

massive layoffs by major MNCs and a slump in domestic

demand. At the forefront of the layoffs were suppliers of

major building/construction material and household

accessories.

Prices of residential properties, often propped up by

foreign investors and speculators, may actually decline for

the first time. Some analysts commented that the

Malaysian economy will take 2 to 3 years to recover, and

will do so only after there is some upturn in the US

economy.

4.

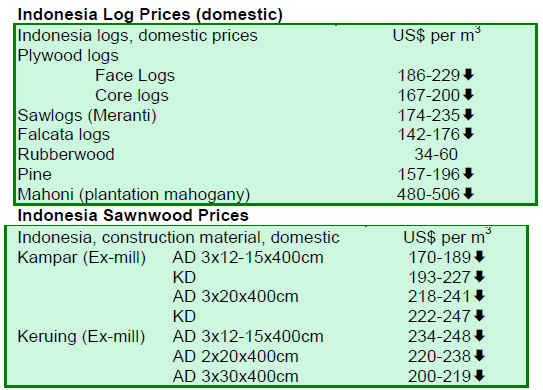

INDONESIA

Indonesian economic stimulus package to be released soon

According to Antara News, the Indonesian government is

currently processing its Rp73.3 trillion economic stimulus

package and will begin to allocate funds by end April

2009. Indonesia, the most populated state in South-East

Asia has been facing its worst recession in modern history.

The government was hopeful the stimulus would help

address the various issues posed by unemployment in the

country.

Sales of forestry equipment plunge for PT United Tractors

Forestry Minister MS Kaban said ¡®chronic ailments¡¯

affecting Indonesian forests would take a long time to fix.

As reported in Antara News, the minister indicated weak

government control and mismanagement by forest

concessionaries, timber estates and licensed plantations

had contributed to the damage in the forests. Kaban noted

the ailments were also affecting forest industries and

timber companies, which had cut the state¡¯s foreign

exchange earning and spurred illegal logging and theft. To

address some of these problems, Kaban drew attention to

forest plantation activities undertaken by the government

on the last three years, during which a total of USD1.9

million trees had been planted and which were expected to

boost recovery of the forests.

Price declines trigger fears for mill owners and workers

Reports are emerging that some sawmill and plywood mill

owners in Indonesia may resort to arson to recoup their

financial losses from recent months. Prices of Indonesian

timber products declined sharply as exporters to traditional

markets, e.g. Japan and the US, struggle under the weight

of heavy corporate debts.

Potential investors in the Indonesian timber industry added

that aging machinery, poor infrastructure and illiteracy are

some of the biggest hindrances to investors. The high rate

of illiteracy in Indonesia makes it difficult for companies

to train and provide skilled workers required by the

downstream and value-added timber industry.

Experts also noted that any collapse in prices of

Indonesian timber products could trigger a similar chain

reaction among timber producers in the region.

5.

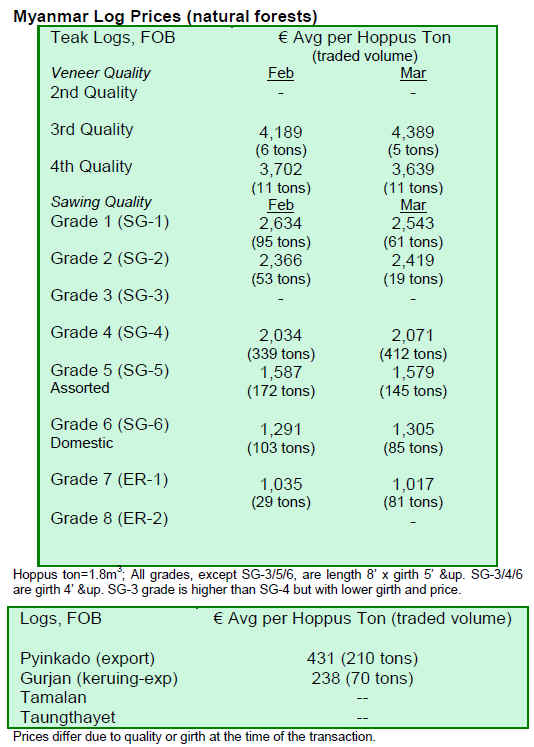

MYANMAR

Low trade expected as a result of holiday period

Analysts expect not much work to be undertaken during

April, with stock taking being done at the end of the

Myanmar fiscal year and the Myanmar new year holiday,

which occurs during 11-21 April. The last tender on 30

April resulted in some price rises for specific grades.

Nevertheless, the quantity traded was small, so the price

gains do not reflect the actual state of the market. April¡¯s

tender prices will be in FOB prices, with the remaining

sales being done on an ex-works basis. Most analysts

believe this will keep prices up, unless log parcels are

graded poorly. The tender lots were reported to be mostly

above average in quality.

In general, the market was reported to be very slow. Not

many new orders for sawn teak were reported. However,

some reports indicate the log market was showing slightly

increasing strength. One analyst expected the situation to

become clearer around June.

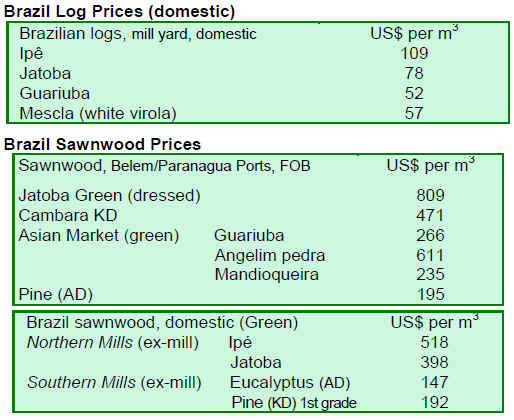

6. BRAZIL

AIMEX anticipates future problems in Par¨¢¡¯s forest

sector

According to Folha do Progresso, the Association of

Timber Exporters Industries of the State of Par¨¢ (AIMEX)

has indicated 2009 will be a problematic year for the forest

sector in Par¨¢. Exports from the state in January and

February 2009 fell 60% by value and 65% by volume

when compared to year 2007 results. Entrepreneurs

working in the international market have recognized the

global economic crisis has strongly impacted Par¨¢¡¯s

industrial and manufactured timber products trade.

However, the delay in government approval of

environmental permits has been cited as the primary

reason for the current difficulties. Many noted that

negative indicators in Par¨¢¡¯s timber sector have preceded

the economic downturn, seemingly due to the delay in

permit approval and the lack of available raw material,

which has lasted for nearly five years.

The situation has become so serious that the state of Par¨¢

has begun to import timber, particularly from Bolivia. Par¨¢

was also buying timber from planted forests in other

Amazonian states. These are considered emergency

measures to meet the terms of the medium and long-term

contracts with the European and American markets.

According to AIMEX, these are illustrations of the crisis

facing the forest sector over the last two decades.

Experts have urged the government to set policies that

promote forest activities. Representatives from the timber

sector have asked the government to invest quickly in

forest concessions and forest plantation policies. AIMEX

has said, given the timber sector¡¯s severe financial crisis,

the state government should take concrete actions to

reduce the impact of the crisis in Par¨¢¡¯s economy. AIMEX

also stressed that measures recently undertaken by the

government, including the restructuring of the State

Secretariat of the Environment (SEMA), were positive, but

were insufficient to cope with an unprecedented crisis like

the current one.

IBAMA and SEMA on the hunt for ¡®ghost companies¡¯

The Brazilian Institute of Environment and Renewable

natural Resources (IBAMA), in collaboration with the

Par¨¢ Secretary of the Environment (SEMA) and IBAMA

regional offices, has continued to conduct investigations to

identify ghost companies, which have fraudulently

engaged in trade of forest products and by products.

According to EcoDebate, the investigations, which were

started in March 2009 (see TTM 14:5), have already

stopped more than 100 companies selling illegal timber in

the state capital (Belem) and other timber clusters of the

state. According to the IBAMA regional office, the

operation has generated nearly BRL100 million in fines,

and fines are expected to reach over BRL1 billion at the

end of the operation.

The operation focuses on companies that exist only on

paper. The ghost companies are established to create a

façade for the company to sell illegal products from

protected areas, public forests and indigenous lands. In

2008, illegal trade in these products was responsible for

over BRL 250 million. As part of the operation, IBAMA

and its partners will block the operation of the ghost

companies and seize any illegally traded timber or

charcoal from the company. The amount of logs and

charcoal seized so far has reached 10,000 m³ and 5,000

m³, respectively.

Business events expected to generate nearly USD13

million for furniture exporters

The ¡®International Purchaser Project¡¯ Fair, held from 10-

12 March at the Movelpar 2009 Furniture Fair in the state

of Paran¨¢, promoted 402 businesses among 20 importers

and 48 furniture manufacturers, fair exhibitors and

participants, and was organized by Apex Brazil and

ABIMOVEL (the Brazilian Furniture Association).

Research conducted among importers from 17 countries at

the Movelpar Fair indicated 75% of the meetings resulted

in prospects for future business, estimated at USD12.9

million by value. A survey among the furniture producers

indicated deals closed at the end of the business rounds

were worth about USD3.8 million.

Portal Moveleiro has reported that one of the main

obstacles for furniture manufacturers to overcome is the

export crisis. Recently, Brazil has had to undertake

measures to maintain its competitiveness in international

markets. In recent months, the federal government had

been asked to reduce taxes on particleboard imports to

maintain the furniture sector¡¯s competitiveness.

Additionally, ABIMOVEL is establishing a partnership

with design professionals to produce high quality furniture

in order to heighten its competitiveness in the international

market. To some, Brazil is considered to be more

competitive than China in the international furniture

market, since Brazil is known for having higher raw

material quality and design. According to ABIMOVEL,

Chinese furniture is more expensive due to a number of

factors, including freight costs for exports and a reduction

in the weekly working hours now set at 40 hours, whereas

Brazilian workers clock over 44 hours.

Brazil exports about 10% of its furniture production.

According to the Federal Secretary of Foreign Trade

(SECEX), furniture exports fell 1.7% in 2008 compared to

2007. In January 2009, it dropped 27.4% compared to

January 2007. Despite these negative indicators, there is a

prospect of a 5% increase in sales to the domestic market

and a 3% rise in sales to the international market.

ABIMOVEL is also requesting the federal government

reduce tax on industrialized products (IPI) from 10% to

5% and to include the furniture sector in the Growth

Acceleration Program (PAC) for housing, which is

expected to cost about BRL90 billion by 2010.

Furniture exports to Argentina drop 51%

Sharp declines in Brazilian furniture exports to Argentina

have been appearing, similar to a cycle observed in 2000

and 2001. This has been caused by a strong deceleration of

the Argentinean economy, noted Gazeta Mercantil. The

Association of Furniture Companies of Rio Grande do Sul

(MOVERGS) reported that in the first bi-month of 2009,

Brazil¡¯s exports to Argentina were 51% less than the same

period of last year (USD6.4 million in 2009, compared to

USD13.1 million in 2008).

This was the worst fall since 2004. The average annual

growth in exports to Argentina between 2004 and 2008

was 72% per year. However, the average drops to 39.5% if

the first two months of 2009 are included. The annual

average growth rate of Brazilian furniture exports between

2004-2008 was 10.6%, but if including results from the

first two months of 2009, it slows down to only 2.1%.

Additionally, a new trade rule in Argentina requires

importers to have an import license for Brazilian furniture

products, which is considered to some a new obstacle in

the bilateral relationship. The measure has been the subject

of negotiation between the governments. Venezuela has

already adopted the license system and Ecuador has

recently increased import tax from 24.5% to 60.5%. These

markets do not have enough mills to meet their demand.

One-third of shipments of Brazilian furniture go to the

European Union (EU). However, the situation there is not

unlike that in Argentina. In the first two months, exports to

France decreased 38.6%, 19.1% to the United Kingdom,

11.1% to Germany, 11.5% to the Netherlands and 50% to

Spain. Brazil closed its January - February balance with a

31.7% drop in furniture exports over the same period of

2008 (USD96.5 million against USD141.2 million in

2008).

Leadership transition in Brazilian Forest Service

Antonio Carlos Hummel has been appointed the new

Director General of the Brazilian Forest Service (BFS),

replacing Tasso Azevado. Azevedo will now act in the

capacity of special advisor to the Minister on forest and

climate change issues and on matters relating to the

Amazon Fund, an organization implementing forestry

projects in that region. The new Director General of the

BFS has been a career employee of IBAMA and in the last

six years was responsible for overseeing the Department

of Biodiversity and Forests. He has extensive experience

on forestry issues, especially in the institutional

development of the sector. As director of the BFS, he will

be responsible for implementing and expanding the

Brazilian forest concessions and for sustained production,

and will oversee BFS¡¯s role as focal point of the ITTO for

Brazil.

7.

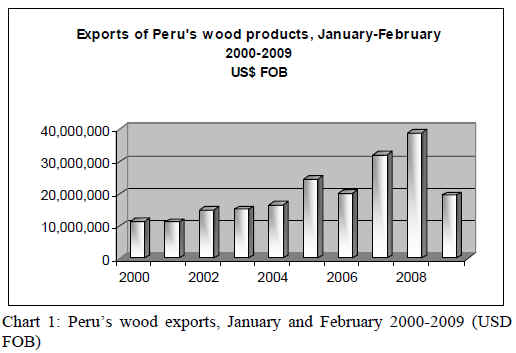

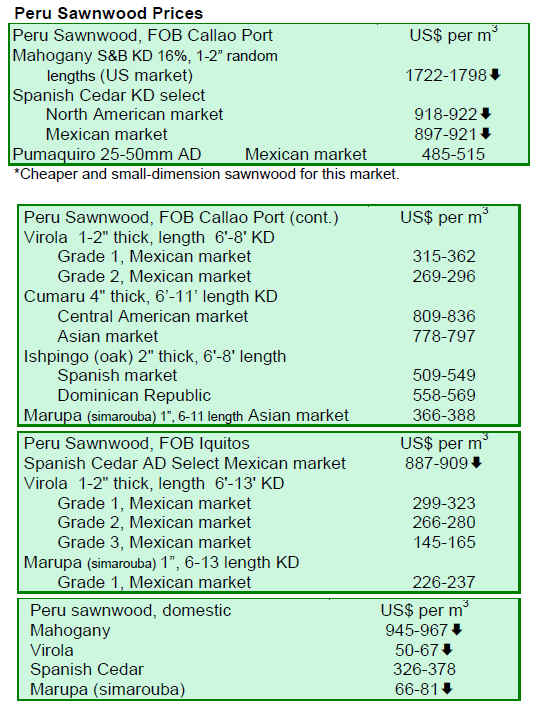

PERU

Early 2009 exports drop 50%

According to the Export Association of Peru (ADEX),

Peru¡¯s wood exports from January-February 2009 dropped

50% by value, when compared to the previous year.

Exports also fell to USD19.6 million during 2009 from

USD39.2 million from the same period in 2008.

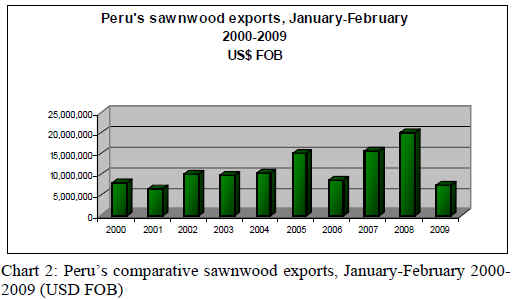

Sawnwood represented 37.6% of sector exports. Exports

in January-February 2009 were just over USD7 million,

while for the same period in 2008 exports were USD20

million, a year-on-year decrease of 63%. The main

markets for this sub-sector were Mexico, China, the US,

and the Dominican Republic, which received 41%, 22%,

14%, 8% of sawnwood exports, respectively.

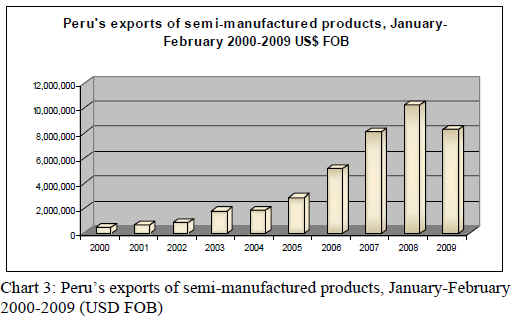

Semi-manufactured products accounted for 42% of wood

sector exports and ware the principal export item in the

wood sector. Exports in January-February 2009 were

valued at USD8.3 million, while exports for the same

period in 2008 were valued at USD10.3 million, marking a

19% drop in exports against 2008 levels. The main

markets for this sub-sector were China, the US and Hong

Kong, which received 80%, 9% and 5% of semimanufactured

products, respectively.

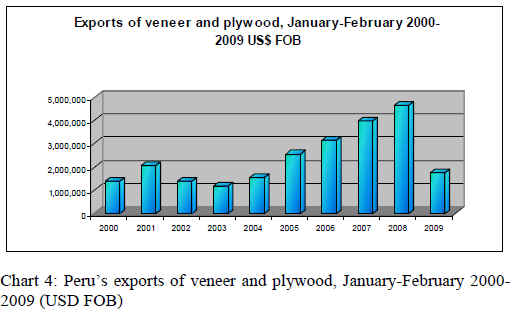

Veneer and plywood exports for the January-February

2009 period were USD1.7 million, while exports for the

same period in 2008 were valued at USD4.7 million,

falling 62.6%. Results from the sub-sector show Mexico

as the main market for Peru¡¯s exports (78.7%) followed by

Venezuela (15.4%), with other countries making up the

remaining 5.9%.

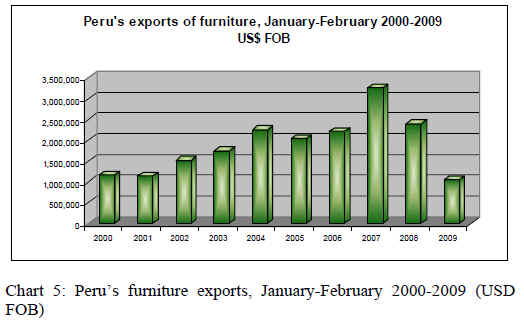

Furniture exports were worth a value of USD1.1 million

during the January-February 2009 period, a 56.2%

decrease from the same period in 2008. The main market

destination for these products was the US (58.7%),

followed by Italy (21.5%).

During the January-February 2009 period, exports were

concentrated in three markets representing 81.1% of total

wood products exports. China represented 42.6% of

exports in the sector, dropping 6.5% when compared to the

previous year. Mexico followed, receiving 23% of exports,

although this was a 70% drop in exports received in the

previous year. The US was the third destination market,

representing 15.3% of exports, although its level of

imports has fallen 68.9% when compared to the same

period in 2008.

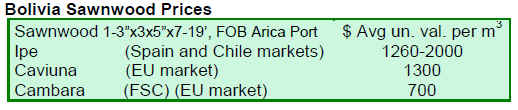

8. BOLIVIA

9. Mexico

Mexico lowers annual deforestation average

Mexico¡¯s annual average deforestation rate fell from

348,000 hectares to 260,000 during the period from 2000

to 2005, according to data provided by the national forest

inventory. This was considered encouraging for national

policies designed to improve the state of Mexico¡¯s

vegetation and forests. This information on Mexico¡¯s

deforestation rate was included in the State of the World¡¯s

Forests 2009, published by the Food and Agriculture

Organization of the United Nations (FAO) and presented

at the nineteenth session of the Committee on Forestry

(COFO) in Rome, Italy, from 16-20 March 2009.

During the last decade, the financial resources invested by

Mexico have helped initiate or fortify processes of

community development in 2,000 agrarian centers. In the

present administration, this investment has reached 565

million pesos for communitarian forest management over

334,391 ha, through the national programmes ProTree and

the Programme of Communitarian Forest Development

(PROCYMAF). In the same period, it has addressed the

technical management of 3.6 million hectares of forest and

obtained sustainable forest management (SFM)

certification for over 244,719 ha of land.

Additionally, forest representatives of 115 countries

recognized Mexico¡¯s contributions to mitigating climatic

change, to prevent deforestation and fight the poverty in

forest zones, particularly by way of community forest

management and application of SFM. At the COFO

session, Mexico suggested that SFM was an important

element to address climate change and noted SFM and the

Reduction of Emissions by Deforestation and Degradation

(REDD) should be more broadly addressed in UN

Framework Convention on Climatic Change. Mexico is in

the process of elaborating a national program on climatic

change and is considering how to adapt to and mitigate the

effects of the phenomenon.

10.

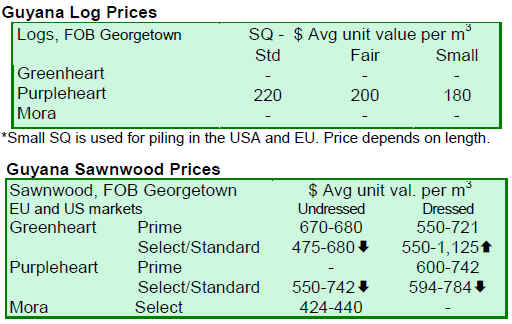

Guyana

Guyana¡¯s prices show relative stability

A comparison of prices from the period 16-31 March 2009

with the corresponding period in 2008 showed relative

stability in log prices. Sawnwood prices have shown

significant increases when compared to the same period of

2008. Plywood and roundwood prices have remained

stable for the same period in 2008. Value-added products

such as doors have shown a moderate increase in export

value when compared to same period. The Caribbean

market was the main destination for value-added exports.

Outdoor garden furniture for the period under

consideration recorded a comparatively high export value

to the UK market. Mouldings have also shown a higher

export value when compared to the same period of 2008.

Guyana to convene regional chainsaw milling workshop

A regional workshop on chainsaw milling in the Guiana

Shield/Caribbean will be convened in Georgetown,

Guyana within the framework of the project ¡®Developing

alternatives for illegal chainsaw lumbering through multistakeholder

dialogue in Ghana and Guyana¡¯. The chainsaw

milling project focuses on the broad theme of forest

governance in Ghana and Guyana, where there has been a

prevalence of chainsaw lumbering and different

approaches have been taken to regulate this activity. The

regional workshop targets decision-makers and scientists

in the regions where chainsaw lumbering activities occur

and aims to present issues and options for regulating

chainsaw lumbering.

The project, from which the workshop originates, is

funded by the EC and Tropenbos International and has

embarked on research into the causes and consequences of

chainsaw lumbering, to better understand the phenomenon

in Ghana and Guyana. This research is being compiled

into case studies for the two countries and will serve as

inputs into two regional meetings designed to identify the

main issues in West Africa and the Guiana

Shield/Caribbean region. The findings from the regional

meetings will be summarized in a synthesis paper that will

be discussed and refined with participation from experts

around the globe. The outputs of these exercises will be

documented and distributed in a publication of the

European Tropical Forest Research Network (ETFRN)

News.

|