|

1.

CENTRAL/ WEST AFRICA

Gabon bans harvest of four major timber species

Very slow market conditions continue in West Africa.

However, significantly, the government of Gabon

indicated that from 1 January 2009, four major species of

timber, afo, douka, moabi, and ozigo, are no longer

permitted to be harvested. Producers will have three

months in which to dispose of all stocks of these species.

The impact of this measure on market prices and the

volume of annual harvest in Gabon has yet to be assessed.

Moabi is a major species for the market in France,

although French importers are currently overstocked with

moabi. Despite this, there may be a rush to secure the

limited stocks that remain in the pipeline. Although

individually the volumes of each of the four species are

not that significant, the ban will mean a noticeable

reduction in the harvest volumes per hectare. This is

expected to impact the viability of some concession areas.

At this stage, there is no information as to whether or not

concession holders will be able to increase annual

allowable concession areas or harvest volumes per hectare

of other species to compensate for the lower output.

As to the markets, the current very cold weather in Europe

is expected to exacerbate the already very low activity in

the housing and construction industries. All the major

importing countries are struggling with their respective

financial sectors, and housing loans and development

finance are very difficult to find. The UK is particularly

badly affected because of the slump in the value of the UK

pound against the euro and the US dollar, making imports

priced in euros much more expensive. Currently, there are

no price changes to report for logs or lumber, and it is not

clear how the market will develop in the first quarter,

although there are no forecasts from industry of any real

upturn in the European market.

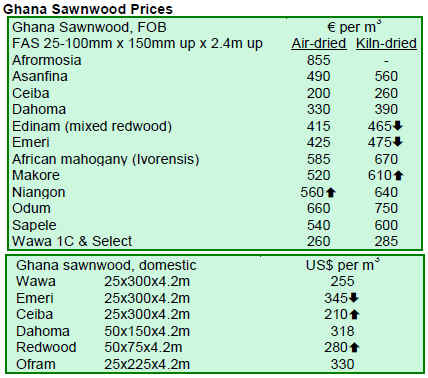

2. GHANA

Ghana¡¯s third quarter export permits take slight fall

According to data provided by the Timber Industry

Development Division (TIDD) of the Forestry

Commission (FC), 2,196 export permits were vetted,

processed, approved and issued to exporters during the

third quarter of 2008 to cover shipment of various timber

and wood products through the ports of Takoradi and

Tema as well as for overland exports to neighboring

countries.

Compared to the number of export permits issued in the

second quarter of 2008, which totaled 2,319, third quarter

results fell 5.30%. This decrease could be attributed to the

slump in trade due to the summer holidays in the European

Union and North America, which are Ghana¡¯s two main

markets.

Lumber kiln-dried (KD) and air-dried (AD) consisted of

45.49% of contracts, registering the highest number of

export permit applications for the period under review,

resulting from higher demand for these products than for

tertiary wood products such as furniture parts, moldings,

floorings, dowels, broomsticks and profile boards.

Substantial decreases in the number of permits were issued

in the third quarter for the export of blockboard, layons,

floorings, dowels, moldings, boules, sliced veneer and

rotary veneer. Nonetheless, there were significant

increases in the number of permits issued during the same

period for the export of teak billets/poles/logs. This

increase may be attributed to heightened demand for this

product by India and Hong Kong.

Three hundred and thirty eight export permits, with a total

volume of 32,937m3 and valued at EUR10.30 million,

were issued to a number of timber companies for overland

export of lumber, plywood and/or blockboard by road to

Burkina Faso, Nigeria, Niger, Mali, Benin and Togo.

Celtis rotary veneer in the US market commanded an

average price of USD500/m3, which was USD9/m³ more

than the GSP of USD491/m3 in the quarter under review.

During the third quarter of 2008, two rubberwood

contracts were given to Best Glow Wood Limited to

supply 2000 m3 each of rubberwood lumber to Tan Eng

Hout & Sons and Hsin Foogn Manufacturers Limited,

Chinese buyers of wood products from Malaysia. These

were the largest contracts signed by the company since

July 2007 and secured an improved price for rubberwood

of USD160/m³, up from the previous level of USD130/m3.

Smaller volumes of sliced veneer contracts were approved

for John Bitar & Company Limited and Logs & Lumber

Limited to supply this product to buyers in China, India,

Russia and Singapore, which previously had not been a

preferred destination for the product. It is anticipated that

these markets would be further expanded to receive larger

volumes in the future.

3.

MALAYSIA

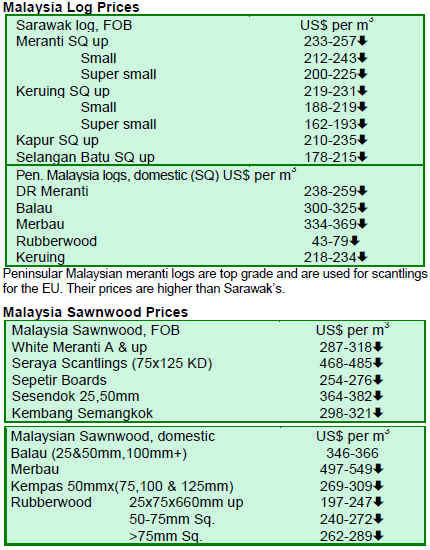

Malaysian timber prices suffer sharp declines

Prices of Malaysian wood products have declined sharply

as the global economic slowdown began to deeply impact

the industry. The price decline was the steepest since the

Asian financial crisis in the late 1990s.

Timber merchants and wood products manufacturers alike

were rushing to reduce inventory by offering bulk

discounts to buyers. Some timber merchants lamented that

many of them had not received any new orders from

buyers beyond January 2009.

Both manufacturers and sawmillers were facing the grim

prospect of scaling down businesses in the near future.

Between 30% to 50% of small and medium-sized

businesses may be forced to shut down by end March

2009. There was a fear that up to 70% of workers in the

timber industry may be laid off before end 2009.

Limited demand for Malaysian timber debilitate furniture

industry

The recession in the US, reflected in the latest job data

revealing a total job loss of 2.6 million in 2008, has

brought the Malaysian furniture industry nearly to a

standstill. Manufacturers are now counting on existing

demand from the Middle East to keep their factories in

operation for the next six months.

Any expectation of fresh orders from European buyers for

sawn timber has mostly evaporated. Many European

buyers have opted to have their deposit forfeited than to

take delivery of any stock of sawn timber.

A number of sawmills are expected to close down

permanently after the Chinese New Year at the end of

January 2009. An increasing number of warehouses in

Malaysia are also experiencing slow moving stockpiles of

plywood and other panel products, reported The Star.

Malaysia and EU to sign VPA in early 2009

Bernama reported that Malaysia and the EU were

expected to sign a Voluntary Partnership Agreement

(VPA) within the first three to four months of 2009. The

announcement by Vincent Piket, the EC ambassador to

Malaysia, indicated that the EU was continuing

negotiations on the EU¡¯s acceptance of Malaysia¡¯s

certification system for timber. He noted that acceptance

of the new system would mean that Malaysian timber

would not require further certification in the EU market.

4.

INDONESIA

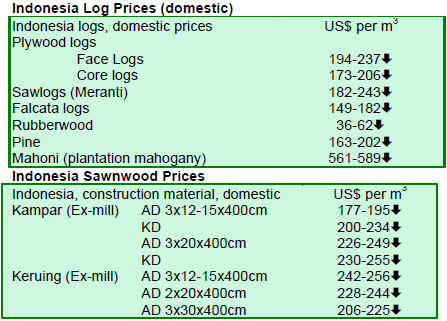

Prices decline despite slide of rupiah

News that China is gradually increasing its export tax

rebates for plywood sent jitters throughout the Indonesian

plywood industry, which is already struggling to cope with

the global economic downturn. Prices of Indonesian wood

products continue to decline sharply even as the Indonesia

rupiah depreciates against major traded currencies.

Nevertheless, the lower exchange rate has not been able to

encourage more buyers of Indonesia¡¯s plywood.

According to The Jakarta Globe, the Indonesian

government is stepping up its effort to assist the industry

by creating a USD4.64 billion economic stimulus plan.

Indonesia is counting on infrastructure projects that will

help stimulate consumption within the local population.

However, layoffs within the Indonesian wood products

industry are already taking place as several timber

concessionaires and forest plantation owners begin

curbing logging operations. With many development

projects coming to a standstill in major cities across

Indonesia, demand for logs is low due to a glut in sawn

timber supply.

Pulp and paper industry to use wood from natural forests

Antara reported on the Indonesian forestry ministry¡¯s

reversal of an earlier decision to ban paper and pulp

companies from harvesting wood from natural forests. The

reversal was taken as the ministry was facing problems

with a deficit in log supply from forest plantation projects

for the pulp and paper industry, caused by some

companies delaying the start of plantation projects and

premature harvesting of plantations, causing greater

uncertainty in wood supply. As a result, the ministry was

forced to reconsider its policy of preventing pulp and

paper companies from using wood from natural forests.

The pulp and paper industry will now be able to use wood

from natural forests, if supply from timber estates is not

available.

5.

MYANMAR

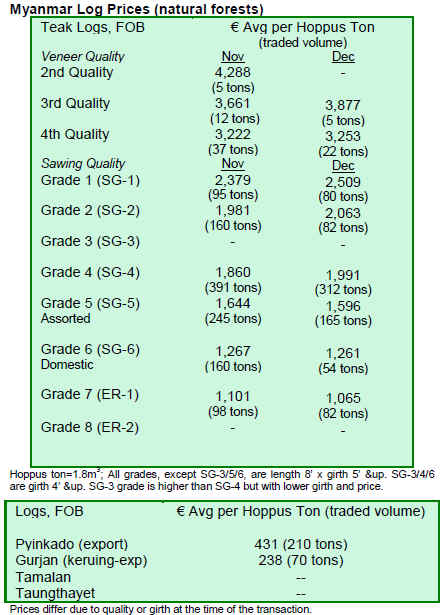

Average tender prices for teak hold stable in December

2008

Teak prices for December 2008 were generally stable

except for some of the higher grades, with MTE selling

about 800 tons in the tender. This limited quantity helped

tender average prices stay at previous levels. Buying and

selling were slow, given the current low level of demand

in the market. With poor economic outlook in developed

countries, Myanmar producers did not expect a dramatic

turnaround in the trade situation in the near future. Some

exporters were also reported to be planning for higher

sales to the domestic market.

6. BRAZIL

Para to soon launch sustainable forest concession

O Liberal reported that the state of Par¡§¢ will soon accept

the first bid for a sustainably managed forest concession.

The Para Forestry Institute (IDEFLOR) has indicated that

the concession area will be about 150,000 hectares within

a total area of 1.3 million hectares and will have a forest

use plan prepared by the state, which will be released in

February 2009. Studies on land use restrictions are

currently being concluded in the concession area. These

restrictions will assist land use planning to identify

traditional community areas, biodiversity preservation and

conservation areas and areas to be used for economic

purposes.

Of the over 15 million hectares of state forests, IDEFLOR

states that when management plans for state conservation

areas of the Calha Norte region are completed in 2010,

there will be a supply of over 8 million hectares of legal

concessions in Par¡§¢. The new plans are anticipated to

revamp the forest economy for the state and solve land

conflicts.

According to IDEFLOR, 2008 was a key year for many

reforestation activities such as the establishment of seed

labs of native forest species in the Tailândia, Altamira and

Marab¡§¢ municipalities. These initiatives will stimulate

seedling production and expand reforestation programmes.

In addition, other actions will be taken to revitalize forest

nurseries, establish West Par¡§¢ University and the Santarem

Technological Complex focusing on forest products

technologies.

Northern Mato Grosso municipalities lead in timber

sales

The municipality of Sinop has led in timber sales in the

state of Mato Grosso for the last three years, representing

15.5% of the state¡¯s total trade, according to the State

Secretary of Environment (SEMA). These statistics,

reported in S¡§® Noticias, take into account the participation

of each municipality in the volume of sales for exports, at

the domestic level and sales within the municipality itself.

Within the state, Aripuanã is the second leading

municipality, with 9% of sales, followed by Juina (7.6%),

Colniza (6.7%), Juara (4.8%) and Alta Floresta (4.7%).

The remaining 135 municipalities make up 51.6% of the

remainder of sales.

SEMA also published a report on wood species

commercialized under the GF3 Forestry Control Bill (Guia

Florestal GF3). The report indicates the volume of

commercialized species in cubic meters, the value and

average price, including sawnwood, laminated veneer,

sliced veneer, wood chips, block and logs of native tree

species, among others. The top commercialized species is

Cedrinho (12.4%), with Ip¡§º ranking second (9.8%) and

followed by Jatoba (8.4%), Ita¡§²ba (5.9%), Garapeira

(5.2%), Cambara (4.7%), Amescla (3.8%), Angelim Pedra

(3.5%) and Cumaru (3.1%).

Paras forest sector continues to experience declines

O Liberal reported that in 2008, a large number of

companies and employees of the Brazilian forest sector

were negatively affected, with exports decreasing about

35% from the state. The state of Par¡§¢ reported a 19.4% fall

in exported volume compared with results for 2007.

According to the Association of Timber Industries

Exporters of Par¡§¢ State (AIMEX), the state of the timber

industry in 2009 will depend on how the new US

government supports its key economic sectors. According

to the latest survey released by the Department of

Statistics and Socio-economic Studies (DIEESE), seven

thousand jobs were lost in the forestry sector in Brazil in

2008. The main factors were the North American financial

crisis, which began with the real estate sector, eventually

impacting the entire financial sector and causing sharp

falls on stock exchanges and reduction in access to credit.

The crisis has also impacted major consumers of forest

products, including the civil construction sector.

It is hoped that after the US financial situation stabilizes,

Para¡¯s business opportunities will improve. However, the

forestry business will also have to overcome the slow

process of approving forest management in natural forests

by environmental agencies. The Industry Federation of the

State of Par¡§¢ (FIEPA) noted that the global financial crisis

has caused the suspension of sale contracts with

companies located in Para, and those who have continued

selling have had to revise product prices. Importers are

also revising their approaches to adapt to the fluctuating

market, with many creating new strategies in response to

the current market situation.

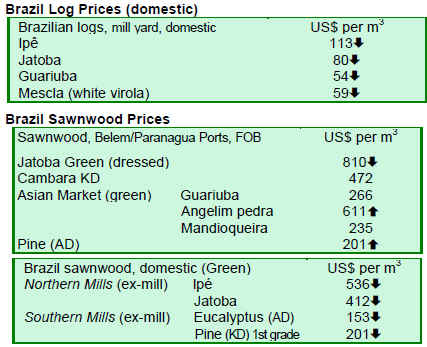

Exchange rate has little impact on Brazilian timber

companies

Gazeta do Povo reported that after almost two years of

low profits triggered by the rise of the Brazilian real

against the US dollar, recent reverses in the trend have

done little to assist profits in the timber sector. Producers

working in the international market have not made much

profit in Brazilian real since demand and prices for

Brazilian products have been falling. On the other hand,

producers depending on the domestic market may also

face the same problem and without attractive prices for

products, the timber sector may continue on a path of

stagnation.

In the state of Parana, until 2006, the US market accounted

for 60% of Brazilian exports, which reached about USD1

billion per year. When US housing construction began to

fall, timber shipments also dwindled. In response to this,

the first action taken was to diversify export destinations.

European countries, particularly England, Germany and

Spain had been increasing their exports imports over the

past few years, but are now asking for price reductions

given the current state of the economy. According to the

Brazilian Association of the Mechanically Processed

Timber Industry (ABIMCI), the fluctuation of the

Brazilian real against a number of currencies has badly

affected the timber industry. Exporters are facing

difficulties obtaining bank credits and prices for contracts

have been very low. The interest rate has jumped from 6-

8% per year to 14-18% per year due to the exchange rate

alone. Timber companies have also become more

dependent on the domestic market. Domestic plywood

consumption, fueled by civil construction, increased by

15% in 2008.

7.

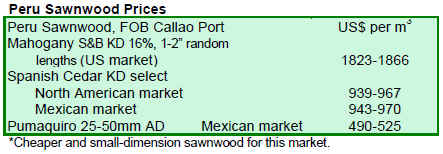

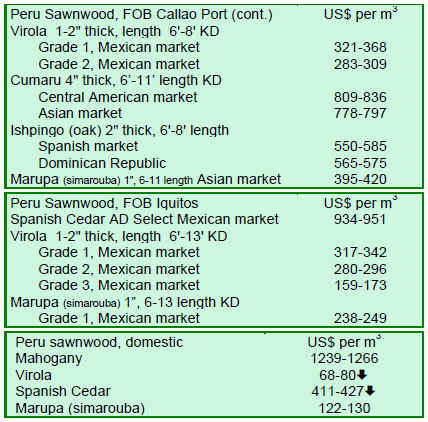

PERU

Peru to plant 2 million trees to combat climate change

Peru¡¯s National Soil and Water Conservation Program

(Pronamachcs) is undertaking an initiative to plant 40

million trees in Peru to combat the effects of climate

change, including through the capture of carbon dioxide.

In Junin, it is expected that over 2 million trees of different

species will be planted. The districts of Chupuro and San

Juan de Iscos will also begin planting trees, with the view

to planting over 32,000 seedlings as part of the national

initiative.

Germany provides EUR20 million to preserve Peru¡¯s

forests

Peru¡¯s Environmental Minister, Antonio Brack Egg,

announced Germany¡¯s contribution of EUR20 million to

Peru, which will be utilized over the next year and a half

to conserve primary forests. Brack was able to negotiate

the deal, along with other agreements on technical

capacity building and CO2 certification, during his recent

visit to Germany. In addition, Brack attended the recent

UN Framework Convention on Climate Change

Conference of the Parties in Poznan, where he stressed

that Peru could achieve emissions reductions over the next

10 years at a cost of USD5 million per year. Brack noted

that Peru would need international assistance to achieve

the ambitious goal, but that half of the required finances

had recently been provided by Germany. To obtain further

assistance, he indicated that Peru was undertaking

negotiations with The Netherlands, the UK and Finland.

INRENA Chief calls for more certified wood products

The Chief of the National Institute of Natural Resources

(INRENA), Mr. Jos¡§¦ Luis Camino, recently called on the

government to increase the amount of Peru¡¯s certified

wood products. He noted that certification would help

educate the industry and strengthen forest management by

concessionaires. He stressed the importance of Peru¡¯s

forest products, saying that the total value of Peru¡¯s forest

products grew from USD13 million in 1990 to USD322

million in 2007.

Camino said Peru¡¯s forests had been reduced to 18.7

million hectares for a variety of reasons, including

deforestation, drug cultivation and trade and a growing

population around forest areas. He also cautioned that a

high percentage of wood products were used for fuel. In

2007 alone, more than 87% of wood products were used

for the production of fuel. Over 7 million types of wood

products extracted from the Peruvian Amazon have been

turned into mostly wood and coal.

8. PERU 8. PERU

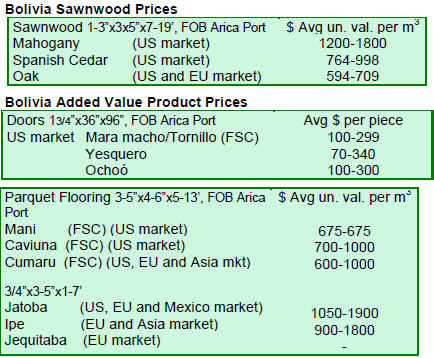

8. BOLIVIA

9.

Guyana

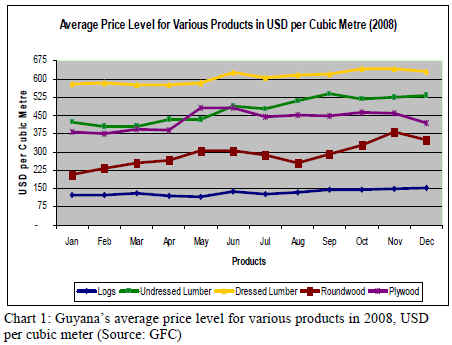

Guyana¡¯s 2008 market trends show mixed results

In 2008, domestic prices for Guyana¡¯s forest products

were mixed compared with 2007 levels. The greatest price

increase was recorded for splitwood, rising 61% over 2007

prices, and was closely followed by similar hikes in

plywood, which moved on average from USD366 in 2007

to USD538 in 2008. Prices for fuelwood rose 29% on

average. Price declines were greatest for roundwood.

The average price level for exported products showed a

more positive trend per cubic meter for logs, lumber and

plywood. Though there were small improvements

recorded for some products, others such as logs and

undressed lumber showed significant improvements in

prices. Robust gains in prices for roundwood per m³ were

recorded during the same period.

Log prices increased approximately 25% over the twelve

month period, moving from USD123/ m³ in January 2008

to USD154/ m³ in December 2008. Other trends over the

twelve month period included: undressed lumber prices,

increasing 26%, from USD422 to USD531; dressed

lumber and plywood prices, each rising approximately 9%,

from USD581 to USD631 and USD384 to USD419,

respectively; and roundwood, jumping 70% from USD206

to USD352.

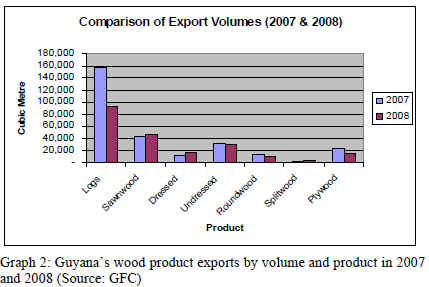

Log export volumes in 2008 were 41% less than the

accumulated total for 2007, the largest fall for any forest

product. Sawnwood export volumes also declined by more

than 8.2% over 2007 figures, although this was less

significant than the decrease in log exports because of the

larger volume of dressed lumber exported. Plywood

volumes were 35% lower than 2007 levels.

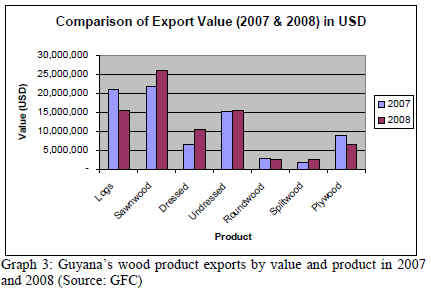

The total export value earned for Guyana¡¯s forest products

was supported by higher average prices per cubic meter

throughout the year. Values for plywood and logs fell by

26% and 25%, respectively. Other products that recorded

gains in the same period were dressed lumber (62%) and

sawnwood (19%).

By region, the Asia/Pacific region was the most important

export market for Guyana¡¯s wood products by value,

although revenue from this region in 2008 was 11% lower

than in 2007. The Latin American/Caribbean region

continued to import a significant share of Guyana¡¯s

products, with the value of exports to this region

increasing 3% over 2007 levels. The value of exports to

the North American market fell by 5%, while revenue

from the European market was up 27%. However, the

smaller contributors to Guyana¡¯s export revenues

increased their market share in 2008. Countries in South

America and Africa contributed a larger amount to

revenues in 2008 than in 2007, with revenue from these

regions increasing 26% and 83%, respectively.

Guyana

|