Japan

Wood Products Prices

Dollar Exchange Rates of 10th

March

2026

Japan Yen 158.05

Reports From Japan

Record-breaking 2026 buget

The adoption of a record-breaking 122.3 trillion yen

(US$785 billion) budget for fiscal 2026 in Japan is widely

considered risky, though it is viewed by the government as

a necessary measure for economic security and

stability. The budget aims to boost defense spending and

stimulate the economy but it has triggered concerns

regarding fiscal sustainability. Japan has the highest debt

burden among developed economies, at over twice the size

of its economy.

Critics fear that the budget that includes a massive

stimulus package, could fuel inflation which is already

hovering around 3% and undermining household finances.

Despite the risks, many analysts believe a crisis is not

imminent because a large portion of the debt is held by the

Bank of Japan and local institutions, reducing the risk of

capital flight.

See: https://www.nippon.com/en/news/yjj2026031300179/

Conflict in Middle East could affect annual wage

negotiations

The Middle East conflict is likely to affect Japan's spring

wage negotiations ("shunto") by increasing uncertainty,

complicating the Bank of Japan's (BoJ) policy direction.

While major firms are expected to grant significant pay

raises, high energy prices from the conflict could pressure

real wages and dampen economic growth, likely forcing

the BoJ to delay interest rate increaese.

The Middle East conflict has raised the chances of the BoJ

skipping a rate increase in March as they assess risks to

economic stability, potentially waiting until April, May, or

even June to act. The sharp rise in oil prices will increase

Japan's import costs, pushing up the inflation rate. This

scenario could impact the annual wage negotiations.

January wages growth outpaced inflation

In January real wages in Japan climbed for the first time in

13 months as inflation cooled, with base salaries growing

at their fastest pace in 33 years, government data showed.

The positive turn strengthens the case for the BoJ to keep

raising interest rates to normalise monetary policy.

Average nominal wages, or total cash earnings, increased

3% year-on-year to 301,314 yen ($1,911) marking the

fastest pace since July last year.

The growth in pay was enough to outpace the consumer

inflation rate the ministry uses to calculate real wages.

That was 1.7% in January, the slowest gain since March

2022, thanks to fuel subsidies and fewer food price hikes.

See: https://www.asahi.com/ajw/articles/16407483

Release of some oil reserves

The government will release a total of 45 days' worth of

oil, comprising 15 days of private-sector reserves and one

month of government-held reserves. With most of its oil

sourced from the Middle East, Japan is acting due to

concerns that conflict, specifically around the Strait of

Hormuz, will significantly disrupt oil imports.

The government aims to keep the average retail price of

gasoline around 170 yen (US$1.07) per litre, using

subsidies for oil wholesalers but this is still a major

increase that will eventually translate to higher costs in

many sectors.

Japan depends on the region for more than 90% of its oi,

and Iran’s effective blockage of the Strait of Hormuz,

preventing tankers from passing through, has led to

mounting supply concerns. Prime Minister Takaichi Sanae

responded on March 11, 2026, by announcing plans to

release 45 days’ worth of oil, amounting to almost 20% of

the nation’s reserves, from March 16 onward.

To prevent a shortfall in supply from causing upheaval in

Japan, whether due to political unrest or major disaster

overseas, private-sector actors have held oil reserves from

fiscal 1972 onward and the national government has

maintained reserves since fiscal 1978.

As of December 31, 2025, Japan’s state reserves held oil

equivalent to 146 days’ consumption, while private-sector

reserves held 101 days’ worth, and joint reserves with oil-

producing countries had 7 days’ worth. This adds up to

254 days’ worth of oil overall, or 470 million barrels.

See: https://www.nippon.com/en/japan-data/h02732/

Middle East conflict clouds decisions on interest rates

The consensus amongst analysts is that the BoJ will keep

its key interest rate at 0.75% but likely raise it to 1.00% by

end-June. The Middle East conflict has reignited global

inflation fears due to escalating oil prices and this

complicates central bank policy decisions as they grapple

with supply shocks and weaker economic growth.

See: https://www.reuters.com/world/asia-pacific/boj-raise-

interest-rates-next-quarter-with-expectations-unchanged-by-

middle-east-2026-03-11/

Consumers adopt cautious approach to purchasing

In the third quarter of 2026 Japanese consumers were

beginning to reduced spending on durable goods as

inflation persists. While wages are rising they have often

struggled to keep pace with the rising costs of daily

necessities, prompting consumers to adopt a more cautious

and selective approach to purchasing non-essential, long-

lasting items. Spending on durable items such as furniture

dropped almost 11% in January

Many households are adopting a defensive stance,

prioritising savings and holding off on large purchases

despite some signs of recovery in real wages.

The spending data is a key indicator of private

consumption, which accounts for more than half of Japan's

gross domestic product.

See:

https://mainichi.jp/english/articles/20260310/p2g/00m/0bu/0100

00c

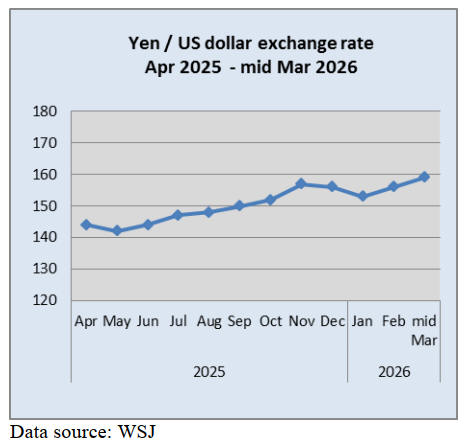

Yen weakens, safe haven status in doubt

The yen is weakening as the conflict in the Middle East

worsens with the currency's safe-haven image tarnished by

concerns that higher crude oil prices will widen Japan's

trade deficit and the recently adopted national budget is

unsustainable.

The Japanese yen traded at levels not seen in about 20

months in a dramatic drop on 13 March and looked likely

to drop further which could trigger intervention by

Japanese authorities. Some are suggesting the yen could

fall below the 161 level seen around 40 years ago.

See:

https://www.japantimes.co.jp/business/2026/03/13/markets/yen-

weakens-us-dollar/

Exchange rate movements an increasingly important

driver of inflation outlook

Bank of Japan Governor Kazuo Ueda has warned that

exchange rate movements are becoming an increasingly

important driver of Japan’s inflation outlook, highlighting

the growing influence of the weaker yen as rising energy

prices threaten to reignite cost-push inflation.

“Foreign exchange is one important factor affecting the

economy and prices,” Ueda said, adding that policymakers

must remain mindful that currency swings can influence

inflation expectations. The yen depreciation amplifies the

inflationary impact of higher commodity prices by

increasing the cost of imports.

See: https://investinglive.com/centralbank/bojs-ueda-warns-

weak-yen-could-amplify-inflation-as-oil-prices-rise-20260312/

Strong housing growth in Urban areas

Japan's housing demand is experiencing strong, localised

growth in urban centers, particularly Tokyo, driven by

foreign investment and redevelopment, while rural areas

face decline. Major cities (Tokyo, Osaka, Fukuoka) show

rising prices and increasing rents for new properties,

though national demand is weakening overall due to

demographic contraction.

Increasing construction costs and mandatory energy-

saving standards are driving up prices for new homes.

Potential interest rate adjustments could significantly

affect mortgage affordability and total residential demand.

See:https://www.landhousing.co.jp/for-foreigner/column/50

and

https://www.cbre.co.jp/en/insights/reports/japan-market-outlook-

2026

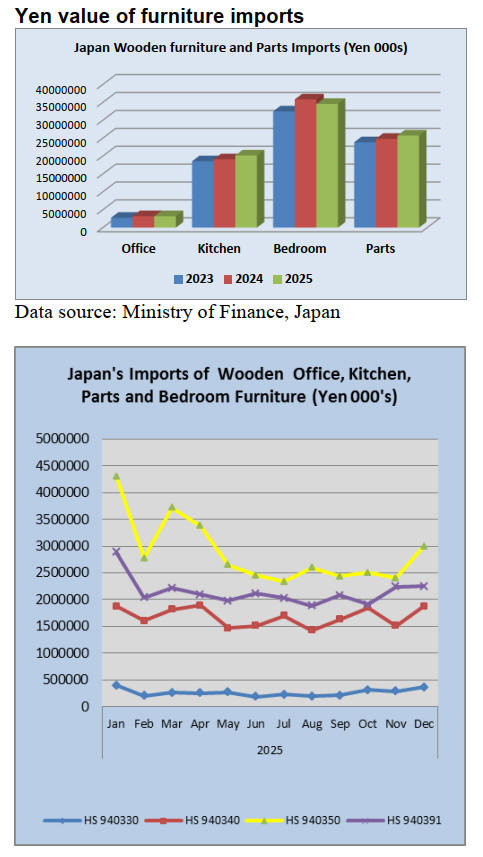

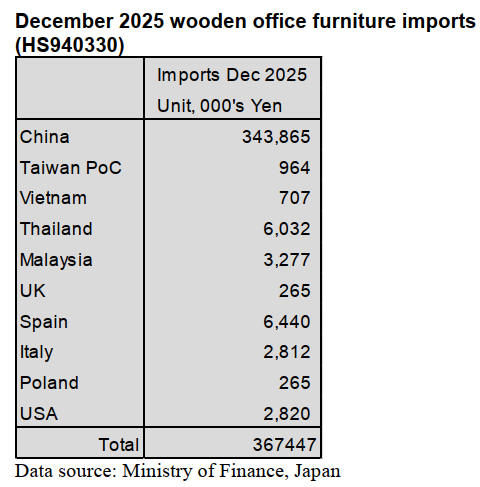

December 2025 wooden office furniture imports

(HS940330)

December saw a rise in the proportion of wooden office

furniture imports from China which jumped to 94% of all

HS940330 imports (85% in November). The other main

suppliers in December were Spain and Thailand. There

were no imports of wooden office furniture from Thailand

in November.

The top three shippers accounted for 97% of Japan’s

December 2025 imports of wooden office furniture.

The total value of HS940330 imports in December was

12% higher than in November. Year on year December

2025 imports were almost 30% higher.

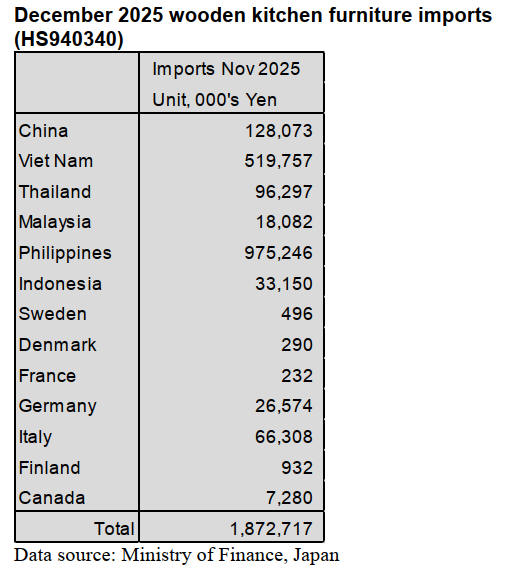

December 2025 wooden kitchen furniture imports

(HS940340)

In December 2025, the top three shippers of wooden

kitchen furniture (HS940340) accounted to just over 92%

of all HS940340 imports. The value of shipments from the

Philippines accounted for most (52%, 49% in November).

Shippers in Viet Nam contributed a further 28% to

December imports followed by China (7%) and Thailand.

December import values for HS940340 from the

Philippines rose sharply (31%) from a month earlier.

December arrivals from Viet Nam were up 16% month on

month while the value of December shipments from China

wer little changed from a month earlier.

Year on year the value of December wooden kitchen

furniture imports was up 7%.

November 2025 wooden bedroom furniture imports

(HS940350)

In a correction to the long period from mid-2025 when the

value of wooden bedroom furniture hardly changed there

was an over 30% jump in the value of December imports

but despite this increase the value of second half 2025

imports was far below that in the first half of the year.

As was the case throughout 2025 imports of wooden

bedroom furniture were dominated by shippers in China

and Viet Nam. Over 90% of the value of HS940350 in

December was shipments from China (60%) and Viet

Nam (30%). The third and forth largest value of shipments

were from Malaysia and Italy.

Year on year there was a 4% decline in the value of

December imports.

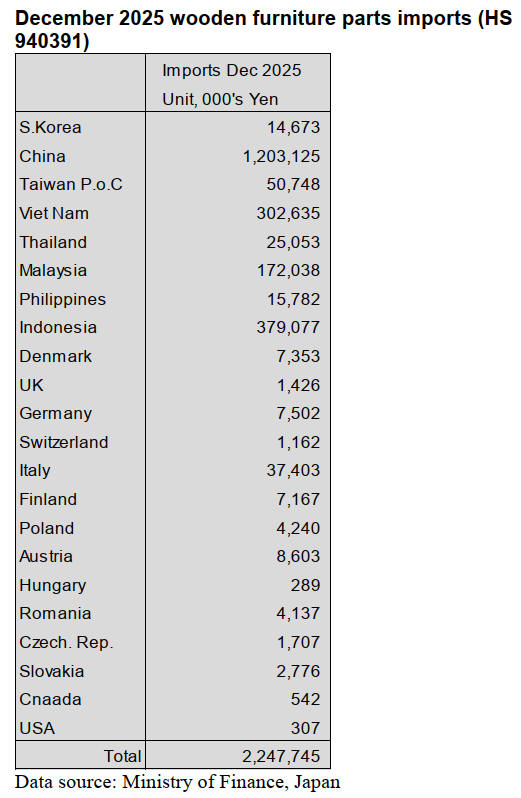

December 2025 wooden furniture parts imports

(HS940391)

Shippers in China and three SE Asian countries,

Indonesia, Viet Nam and Malaysia accounted for over

90% of Japan’s December imports of wooden furniture

parts (HS940391). These countries were the main source

of parts throughout 2025.

Shipments from China accounted for 53% of the total

value of December imports. The second largest shipper

was Indonesia at 17%, down from 20% in November

followed by Viet Nam at 14% and Malaysia 4%.

December arrivals from China and Viet Nam were at

around the same levels as in November. Arrivals from

Indonesia were down 14% with only Malaysia, among the

top shippers, seeing an increase of 24%. Year on year, the

value of December imports of HS940391 rose 6%.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR. For the JLR report

please see: https://jfpj.jp/japan_lumber_reports/

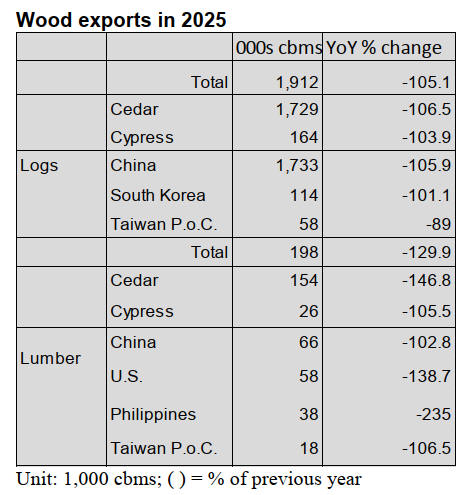

Wood export in 2025

In 2025, Japan’s wood exports totaled 1,912,494 cbms of

logs, a 5.1% increase from the previous year, and 198,690

cbms of lumber, a 29.9% increase. Log exports reached a

record high for the third consecutive year. Lumber exports

increased for the second consecutive year, reaching the

second-highest level on record after 2021.

Against the backdrop of sluggish domestic demand

and

improved cost competitiveness due to the weak yen,

domestic businesses became more eager to export. The

value of wood exports reached 59.5215 billion yen, up

10.9% from the previous year, marking a record high for

the second consecutive year.

China-bound log exports totaled 1,733,267 cbms, up

5.9%

from the previous year. Exports to South Korea reached

114,308 cbms, a 1.1% increase, while exports to Taiwan

PoC were 58,571 cbms, an 11.0% decrease. As a result,

shipments to China have grown for three consecutive

years and those to South Korea for two consecutive years,

whereas exports to Taiwan PoC PoC have declined for

three years in a row.

Exports to Viet Nam totaled 4,531 cbms, a 13.3% increase

from the previous year, marking the first rise in five years.

In addition, exports to Cambodia reached 1,065 cbms, up

from 54 cbms the previous year, and exports to Thailand

were 625 cbms, compared with zero the year before. These

figures indicate emerging efforts to develop new markets.

Regarding exports to China, the key issue was the outlook

for U.S. tariffs on Chinese goods under the Trump

administration. However, driven by a rush in demand

ahead of the tariff implementation, shipments in the first

half of the year exceeded 940,000 cbms, a substantial

25.1% increase from the same period of the previous year,

marking a notably high level. However, once the U.S.–

China tariff war began, purchasing dropped sharply. Due

in part to declining sales prices, volumes in August fell

sharply to 85,227 cbms, a 34.2% decrease from the same

month of the previous year.

From September onward, export volumes recovered,

reaching 169,644 cbms in October, a 25.8% increase from

the same month of the previous year.

Sawn timber exports were as follows: shipments to China

reached 66,019 cbms, up 2.8% from the previous year;

exports to the United States totaled 58,246 cbms, a 38.7%

increase; those to the Philippines amounted to 38,436

cbms, a sharp rise of 135.0%; exports to Taiwan PoC were

18,668 cbms, up 6.5%; and shipments to South Korea

came to 9,590 cbms, a 15.5% increase.

The increases were seen for China, the United States, and

South Korea for the second consecutive year, for Taiwan

PoC for the sixth straight year, and for the Philippines for

the first time in four years.

Exports of sawn timber to Viet Nam reached 5,166 cbms,

up from 876 cbms in the previous year, marking a record

high.

Plywood supply in 2025

The supply of plywood in 2025 reached 4,637,000 cbms, a

slight increase of 0.4% from the previous year, marking

the second consecutive year of growth. Domestic plywood

production increased slightly, rising 2.5% from the

previous year, while imports of plywood declined 1.9%

year-on-year, showing weak growth.

Production of domestic softwood structural plywood

increased 2.8% year-on-year in 2025, marking the second

consecutive year of growth. Shipments increased 3.3%

year-on-year, slightly exceeding production.

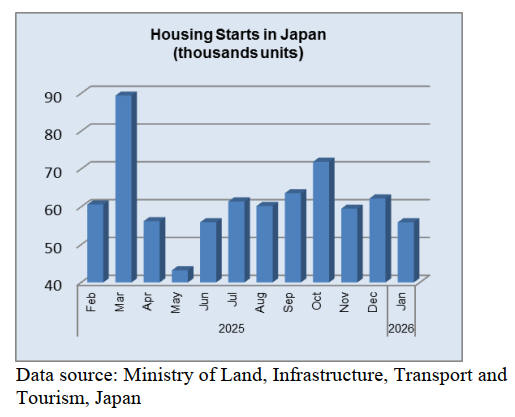

The months in 2025 when shipments exceeded 200,000

cbms were January, April, and October. Japan’s housing

starts totaled 740,000 units in 2025, down 6.5% from the

previous year, underscoring the continued lack of

underlying demand.

Among the major supplying regions, shipments from

Malaysia and China have declined. Plywood from

Malaysia fell below 40,000 cbms in both November and

December, marking a low level, and total arrivals for 2025

ended 2.3% lower than the previous year.

Plywood from Indonesia was essentially flat, edging up

just 0.1% from the previous year. In contrast, imports from

Viet Nam rose 6.2% from the previous year, marking a

second consecutive annual increase.

Plywood price hikes

Nisshin Group and Shimane Plywood will raise the price

of 12 mm, 3×6 structural softwood plywood starting with

March shipments.

As plywood prices continue to soften in the Tokyo

metropolitan area and other regions, the companies are

raising prices to address rising costs such as higher log

prices and wage increases, as well as to secure a stable

supply of logs and finished products. They will first move

to raise the delivered price to wholesalers to 1,100 yen per

sheet.

Plywood price increases

Key-Tec Co., Ltd. raised the price of domestically

produced structural softwood plywood for orders received

from February 21. The company cited persistently high

costs for electricity, adhesives and other inputs,

concluding that a price revision was unavoidable to ensure

the sustainability of its operations.

Compared with pre–wood shock levels, log prices for

plywood production are roughly 30 % higher, and the

current log supply–demand balance is tightening as

harvesting volumes decline

Price hike of plywood

Seihoku Corporation will raise the price of its softwood

structural plywood in March to at least 1,110 yen per

sheet, seeking to offset falling market prices and rising

labor, transport, and log costs

South Sea logs and products

Prices for tropical hardwood and China-made products are

showing signs of rising, particularly for Indonesian items.

Supplies of natural hardwood logs are tightening as

prolonged production cuts at local plywood mills have

reduced log intake, prompting forest operators to scale

back harvesting.

This has pushed up log prices for sawn wood destined for

local markets. As a result, domestic prices for keruing

lumber and decking materials such as selangan batu are

expected to increase, driven by higher source-country

prices and the weaker yen.

Prices for plantation species such as merkus pine are also

moving higher. Heavy rains last November damaged

forest roads in some logging areas, reducing log output,

and local producers report that these supply constraints are

pushing log prices up. In response, manufacturers have

announced product price increases. Indonesian merkus-

pine laminated boards have likewise risen to USD 830–

850 per cbm (C&F), up USD 30– 50 from the previous

month.

Supply and demand for tropical-hardwood logs is

essentially balanced. Necessary volumes arrived between

late last year and early this year, allowing both sawmills

and plywood manufacturers to secure adequate

inventories.

Imported tropical hardwood logs and lumber in 2025

The volume of tropical-hardwood log imports in 2025 fell

16.4% from the previous year but still held at around

30,000 cbms, a level regarded in recent years as broadly

appropriate for stable supply.

Sawn timber and laminated free boards both declined by

roughly 3–5% from the previous year. Indonesia supplied

44,168 cbms of tropical-hardwood lumber, down 4.3%

from the previous year while Malaysia shipped 27,194

cbms, a sharper 14.6% decline.

|