|

Report from

the UK

Slowdown in UK tropical wood product imports

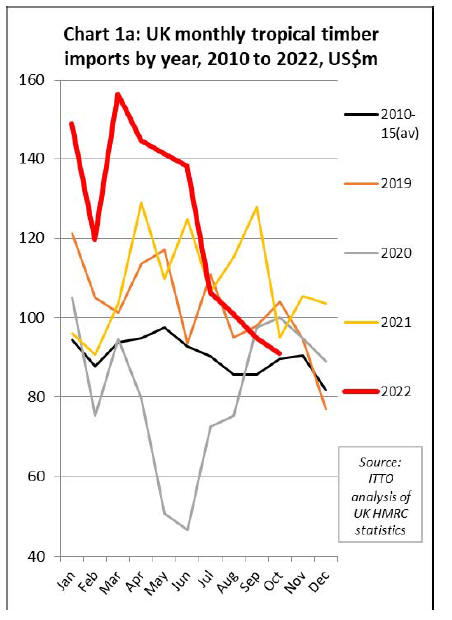

The import value of tropical wood and wood furniture into

the UK in the first ten months of last year was USD1.24B,

13% more than the same period last year. Following the

strongest start to the year in terms of UK import value

since before the 2008 financial crises, imports fell sharply

between July and October (Chart 1).

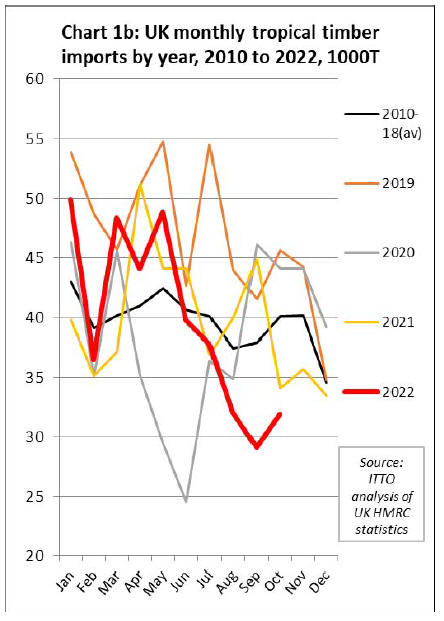

The trend looks different in quantity terms (Chart 1b).

Import quantity of tropical wood and wood furniture into

the UK in the first ten months of 2022 was 398,000

tonnes, 2% less than the same period last year.

In quantity terms, imports were at around the pre-covid

level in the first half of 2022 but fell to well below that

level between July and October. This suggests that price

inflation was the major factor behind relatively high UK

import value last year, driven both by historically high

material and freight prices and extreme weakness of

sterling against the US dollar.

UK economy expected to be worst performing

amongst G7 next year

According to UK government figures published on 22

December, the economy contracted by more than first

estimated in the third quarter of last year. GDP fell by a

revised 0.3% against the 0.2% decline initially estimated

from July to September, the Office for National Statistics

(ONS) said. The manufacturing and construction sectors

performed worse than expected. Manufacturing activity

contracted 2.8%, worse than the 2.3% contraction

previously announced, while construction activity actually

shrank 0.2% compared to earlier estimated growth of

0.6%.

According to ONS, household incomes continued to fall

during the third quarter of 2022, though the rate of decline

slowed compared to the first two quarters of the year, and

household spending fell for the first time since the final

spring lockdown of 2021. The level of households'

disposable income fell by 0.5% in the quarter, the fourth

consecutive drop.

Household spending fell by a revised 1.1% in the quarter

as declines in tourism, transport, household goods and

services, and food and drink spending were seen.

A slowing in real consumption expenditure in the UK was

seen during 2022 including in restaurants and hotels, and

recreation and culture as a result of that reduced

disposable income and a cost of living crisis, fuelled by

high inflation. The UK government blamed the

disappointing figures on high inflation caused by the

invasion of Ukraine.

More positively, ONS recorded GDP growth of 0.5% in

October, a stronger performance than expected by

economists.

However this was explained by the number of working

days returning to normal rather than any real surge in

output.

The UK economy is still expected to be confirmed as

having entered a recession at the end of 2022 as the fourth

quarter as a whole is forecast to have experienced negative

growth.

The Confederation of British Industry (CBI) has also

forecast that the economy will contract 0.4% next year.

The UK is expected to be the worst performing than any of

the other G7 countries that form the group of the world's

largest industrialised democracies, according to forecasts

from the Organisation for Economic Cooperation and

Development (OECD).

Construction activity slows sharply in December

Overall, the UK construction sector was performing quite

well in the year to November. According to comments by

Timber Development UK, the UK trade association, new

house construction performed well. Housing completions

in the third quarter of 2022 were at the highest level since

2007. However, there was mounting uncertainty towards

the end of last year about future prospects in the

residential construction sector because of rising interest

rates.

While new residential construction was still strong in

2022, activity in the renovation and refurbishment sector -

which is particularly important for the hardwood sector -

was slowing from the heights achieved during and

immediately following the pandemic when a lot of money

was invested in home improvement. This sector is

expected now to slow much further, possibly by as much

as 10% in 2023.

The latest data from the S&P Global/CIPS UK

Construction Purchasing Managers’ Index (PMI) – which

measures month-on-month changes in total industry

activity - mirrors these trends. Overall UK construction

activity was growing between September and October last

year - driven mainly by the new residential sector - but

then activity recorded the fastest rate of decline since May

2020 in December.

Also in that month, sentiment amongst construction firms

towards activity in the year ahead dipped into negative

territory for only the sixth time on record, reflecting fears

around the near-term economic outlook. Pessimistic

expectations were reflected in the first round of job

shedding in the UK construction sector since January

2021.

At 48.8 in December, down from 50.4 in November, the

headline Construction PMI registered below the 50.0 mark

to signal the first contraction in construction sector output

since last August. Commercial construction activity

continued to rise in the final month of the year, but only

marginally, and this growth was outweighed by

contractions across the residential and civil engineering

sectors.

December PMI data also highlighted a reduction in new

orders placed with UK constructors, following a modest

uplift in November. According to survey respondents, the

fall was driven by weak client demand, linked in turn to

higher prices. Construction firms pared back on their

purchasing in December for the first time in three month,

reportedly due to lower workloads. Notably, the rate of

reduction was the steepest for over two-and-a-half years.

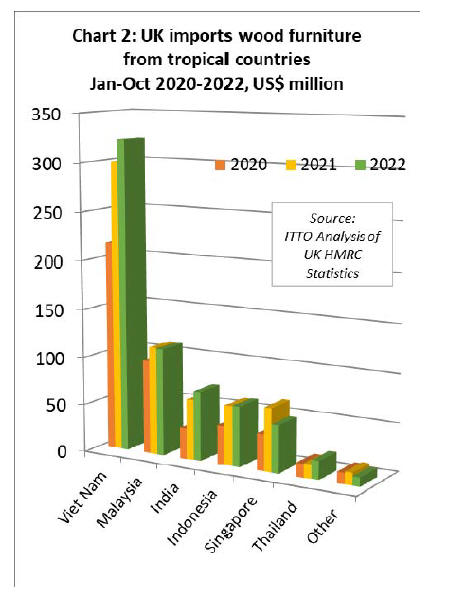

Imports of tropical wooden furniture much lower in third quarter

The UK imported US$647 million of tropical wood

furniture products in the first ten months of 2022, which is

3% more than the same period in 2021. In quantity terms,

wood furniture imports were 133,000 tonnes during the ten

month period, 9% less than the same period the previous

year. This indicates that the rise in value was driven more

by price inflation than strong demand. Imports between

June and October 2022 were much lower than the same

period in 2021.

In the first ten months of 2022 compared to the previous

year, UK import value of wood furniture increased 8%

from Vietnam to US$323 million, 15% from India to

US$72 million, 1% from Indonesia to US$63 million, and

30% from Thailand to US$19 million. Import value of

US$111 million from Malaysia was 1% less than the

previous year, while import value of US$49 million from

Singapore was 25% down compared to 2021. (Chart 2).

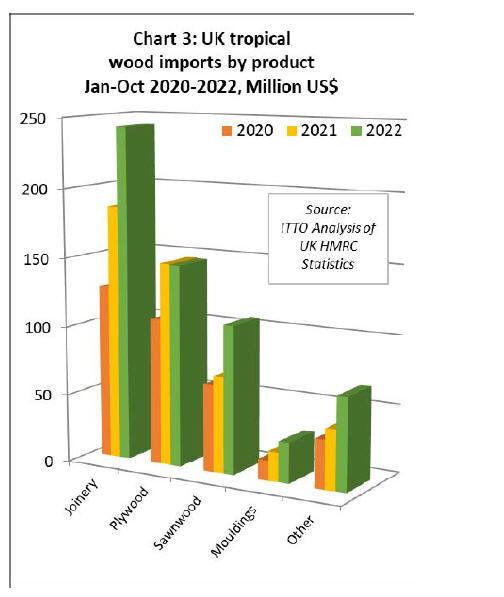

Import quanitity of tropical wood products flat overall in 2022

Total UK import value of all tropical wood products in

Chapter 44 of the Harmonised System (HS) of product

codes was US$595 million between January and October

last year, 27% more than the same period in 2021.

However in quantity terms imports increased just 1% to

265,000 tonnes during the period.

Compared to the first ten months of 2021, UK import

value of tropical joinery products increased 31% to

US$243 million, import value of tropical sawnwood

increased 53% to US$108 million, and import value of

tropical mouldings/decking increased 39% to US$29

million. Import value of tropical plywood was unchanged

at US$147 million (Chart 3).

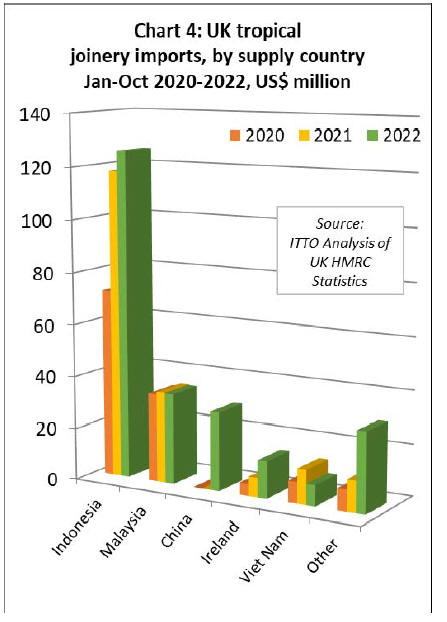

Slowing pace of imports of wood doors from Indonesia

The pace of increase in UK import value of tropical

joinery products slowed sharply between July and October

2022. Import value from Indonesia, by far the largest

supplier of tropical joinery products to the UK (in this case

mainly doors), was at US$126 million still up 7% year-onyear

in the first ten months of 2022 (Chart 4).

In quantity terms, UK joinery imports from Indonesia

were 40,650 tonnes in the first ten months of last year, 6%

less than the same period in 2021.

UK imports of joinery products from Malaysia and

Vietnam (mainly laminated products for kitchen and

window applications) were slow from the start of last year.

Import value from Malaysia was US$35 million between

January and October last year, 1% less than the same

period in 2021. In quantity terms, imports from Malaysia

were 8,900 tonnes, 28% less than the same period in 2021.

Joinery imports from Vietnam of 2200 tonnes valued at

USD8 million were respectively 40% and 39% less than

the same period in 2021.

UK imports of Chinese tropical joinery products, nearly all

comprising doors, were 11,900 tonnes with value of

USD30 million in the first ten months of 2022, up from

negligible levels in previous years. The recorded rise was

due to introduction from 1st January 2022 of new product

codes which identify wood doors and windows

manufactured using a wider range of tropical wood species

in UK and EU trade statistics.

This may also explain the apparent rise in UK imports of

tropical joinery products from Ireland which were 1,400

tonnes with value of US$14 million in the first ten months

of 2022, respectively 53% and 91% more than the same

period in 2021.

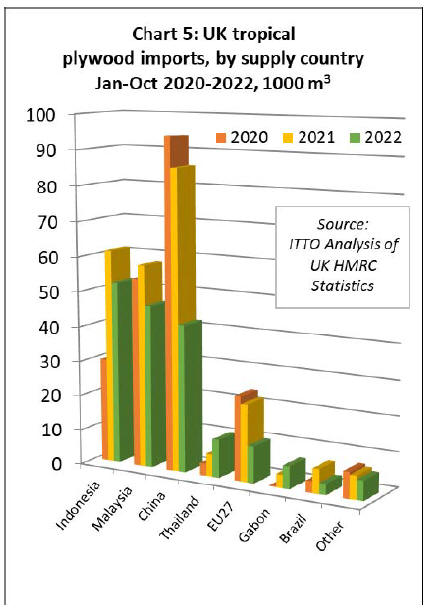

Tropical hardwood plywood imports decline from all leading sources

In the first ten months of 2022, the UK imported 177,600

cu.m of tropical hardwood plywood, 29% less than the

same period the previous year, with significant decline in

imports from all the main traditional supply sources

including Indonesia, Malaysia, and China (Chart 5).

After a strong start to 2022, UK tropical hardwood

plywood imports from Indonesia and Malaysia slowed

dramatically between June and October last year. After the

first ten months, imports from Indonesia were, at 52,400

cu.m, 15% less than the same period the previous year.

The UK imported 46,500 cu.m of plywood from Malaysia

in the first ten months of 2022, 20% less than the same

period the previous year.

The UK imported 42,100 cu.m of tropical hardwood

plywood from China in the first ten months of 2022, 51%

less than the same period in 2021. Probably the biggest

shift in the UK hardwood plywood trade in the last two

years has been a rapid decline in imports of Chinese

products faced with tropical hardwoods in favour of

Chinese products faced with temperate hardwoods.

Chinese temperate hardwood plywood has been the largest

beneficiary of UK sanctions against all trade in Russian

wood products since the start of the Ukraine conflict.

Meanwhile, the combined effects of Brexit, supply

shortages and rising energy and other material costs on the

European continent is impacting on UK imports of tropical

hardwood plywood from EU countries which were just

10,400 cu.m in the first ten months of 2022 compared to

over 20,000 cu.m during the same period in the previous

two years.

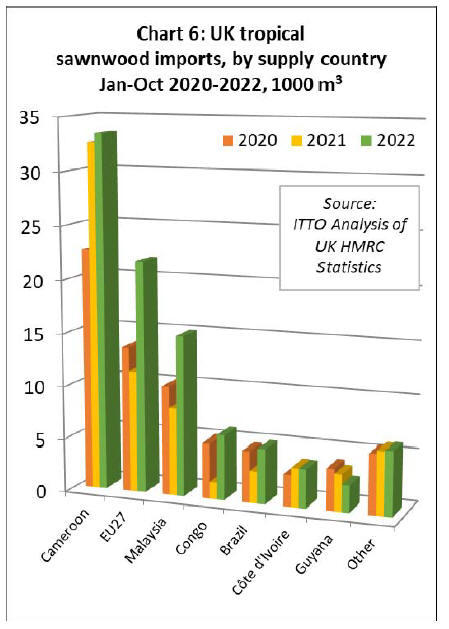

Bouyant UK imports of tropical sawnwood during 2022

Unlike tropical hardwood plywood, UK imports of

tropical sawnwood were buoyant last year. Total UK

imports of tropical sawnwood were 93,800 cu.m in the

first ten months of 2022, 34% more than the same period

in 2021. In addition to making gains overall, there were

some significant changes in the countries supplying

tropical sawnwood to the UK last year (Chart 6).

UK imports of tropical sawnwood from Cameroon were

33,400 cu.m in the first ten months of 2022, 3% more than

the relatively high level in the same period in 2021. UK

imports of tropical sawnwood from the Republic of Congo

recovered lost ground last year, with imports of 6,000

cu.m in the first ten months, a 274% gain compared to the

same period the previous year.

UK imports from Côte d'Ivoire were 3,700 cu.m in the

first ten months of last year, a 1% decline compared to the

same period in 2021.

UK imports of sawnwood from Malaysia, which had fallen

to little more than a trickle in previous years, were 15,000

cu.m in the first ten months of 2022, 83% more than in the

same period in 2021. UK imports of tropical sawnwood

from Brazil were 5,200 cu.m in the first ten months of last

year, 71% more than the same period in 2021.

Indirect UK imports of tropical sawnwood via the EU also

recovered ground last year despite the Brexit disruption,

increasing 91% to 22,000 cu.m in the first ten months of

2022.

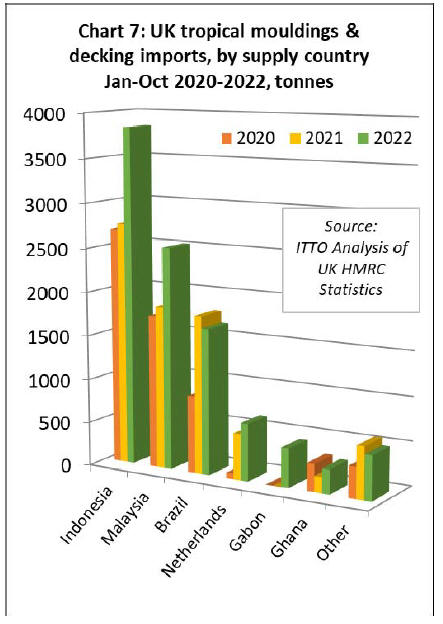

UK imports of tropical hardwood mouldings/decking were

high in the first ten months of 2022, at 9,900 tonnes, 28%

more than the same period in 2021. This commodity group

has benefited in the UK market from shortages of nontropical

products, particularly since the start of the war in

Ukraine and sanctions on Russian decking products that

directly compete with tropical decking. Imports of 3,800

tonnes from Indonesia were 40% more than the same

period in 2021.

Imports of 2,500 tonnes from Malaysia were 37% up on

the same period in 2021. However mouldings/decking

imports from Brazil of 1,650 tonnes were 8% less than the

same period in 2021. (Chart 7).

Tropical hardwood imports expected to remain low

over winter months

UK hardwood contacts suggest that imports from tropical

countries are likely to remain low over the winter months.

Conditions on the demand side are uncertain and, in the

case of sawnwood and decking products, importers are

now carrying a lot of expensive stock following the high

levels of import in the first half of the year.

The supply side situation is also challenging, particularly

as the UK is not such an attractive market as in the past

with buyers elsewhere in the world generally willing to

pay more and to be more flexible with regard to species

and grade.

For African wood, UK importers report very difficult

supply conditions, with many logistical challenges,

problems of cash flow, and high energy costs. Lack of kiln

drying capacity in the UK and a preference for certified

products makes it even more challenging for UK importers

to place contracts in Africa.

The UK market for tropical sawnwood is very focused on

sapele, for which demand was still reported to be quite

good in the final quarter last year. However, as one

importer noted, “there is lot of sapele about in the UK at

the moment”. Demand for sapele benefited in the early

months of last year from difficult supply conditions for

accoya and other modified temperate woods, but supply of

those alternatives is now improving again.

For Southeast Asian hardwoods, decline in global demand

and the rapid falloff in freight rates that occurred in the

second half of last year has helped ease the supply

situation, and there are more opportunities to buy product

at competitive prices, but UK buyers are wary given

current market uncertainty and existing high stock levels.

|