|

Report from

Europe

EU27 tropical wood imports come off the boil as

recession fears mount

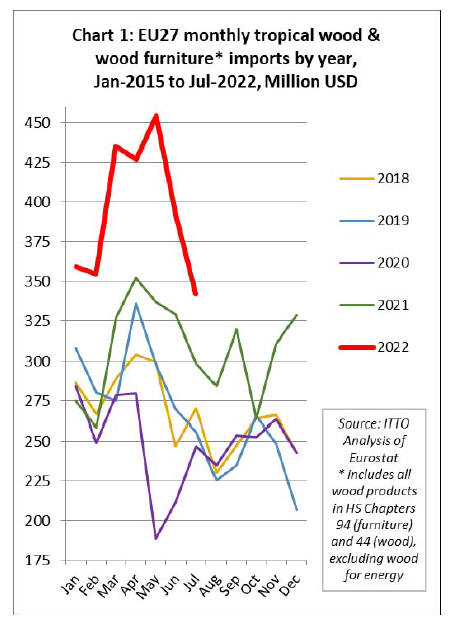

The most recent EU27 trade data to end July this year

shows that imports of tropical wood and wood furniture

products were still at historically high levels in the early

summer months this year. However, imports were slowing

from the peak reached in May.

Now, as Europe moves into the winter months there are

ominous signs of recession ahead, particularly as the war

in Ukraine is contributing to huge increases in energy

prices and business and consumer confidence is being hit

by expectations of higher interest rates to control inflation.

The level of imports in June and July, while still high

compared to previous years, were also sharply declining in

June and July from the heights reached between March

and May (Chart 1).

In the first seven months of this year, the EU27 imported

tropical wood and wood furniture with a total value of

USD2.76B, a gain of 27% compared to the same period

last year. Part of the gain in EU27 tropical wood product

import value was due to a rise in CIF prices. In quantity

terms, EU imports of tropical wood and wood furniture

products in the first seven months of this year were, at

1,190,200 tonnes, up 14% compared to the same period in

2021.

The high level of imports in the first seven months this

year was driven by the combination of a sharp fall in the

value of the euro against the dollar, continuing high freight

rates, and severe shortages of wood and other materials.

Since the start of this year, the value of the euro has

declined around 15% against the US dollar and is currently

at the lowest level for 20 years. In mid-July, the euro hit

parity with the US currency for the first time since 2002

and fell to a low of 0.95 against the dollar at the end of

September. The euro’s slide underlines the foreboding in

the 19 European countries using the currency as they

struggle with an energy crisis caused by Russia’s war in

Ukraine.

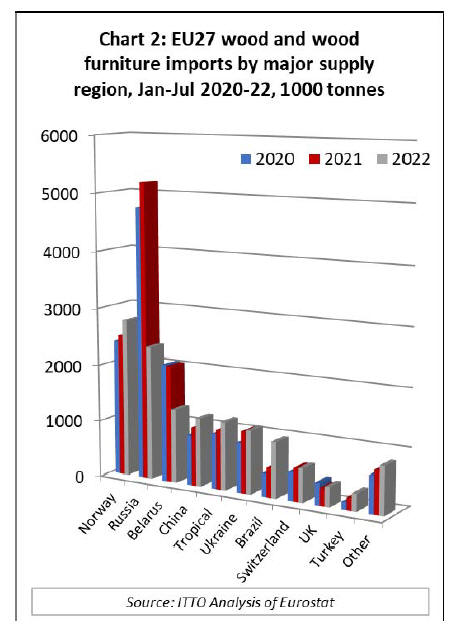

The curtailment of wood supplies from Russia and Belarus

due to the sanctions imposed by the EU following the

invasion of Ukraine in February has opened up new

opportunities in the EU market for some tropical wood

products, notably plywood and decking for which Russian

birch and larch products have been important substitutes.

In the first seven months of this year, tropical products

accounted for 9.2% of the quantity of all wood and wood

furniture products imported into the EU27, which

compares to 6.8% during the same period in both 2021 and

2020.

The gain in tropical wood share is due mainly to a large

reduction in imports from Russia (-55% to 2.34 million

tonnes) and Belarus (-37% to 1.30 million tonnes) during

this period.

After an initial fall in the early months of the war, EU27

imports from Ukraine recovered some ground in the

second quarter and by the end of the first seven months of

this year were, at 1.11 million tonnes, only 3% down on

the same period in 2021 (Chart 2).

While tropical wood has made gains in the EU market this

year, the largest beneficiaries of the opening supply gap

due to the fall in imports from Russia and Belarus have

been non-tropical wood products from Norway (+11% to

2.77 million tonnes), China (+17% to 1.20 million tonnes),

Brazil (+90% to 976,700 tonnes), Turkey (+38% to

304,200 tonnes), Chile (+67% to 66,900 tonnes), and New

Zealand (+24% to 34,800 tonnes).

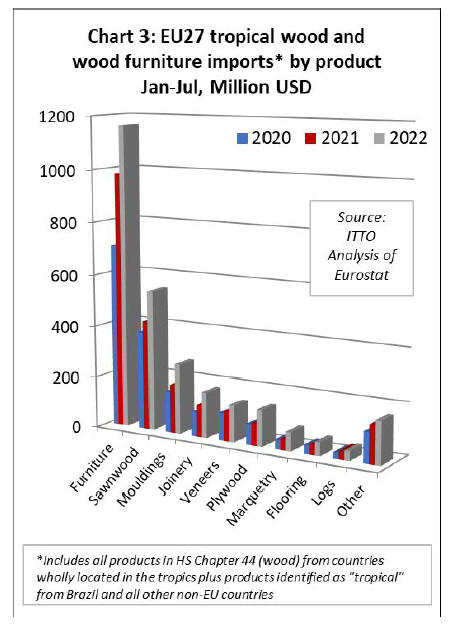

While not benefitting as much as other supply countries,

there were increases in EU27 imports of most wood

product groups from tropical countries in the first seven

months of this year (Chart 3). For wood furniture, import

value of USD1163M during the January to July period was

18% more than the same period last year, although import

quantity was down 5% at 235,200 tonnes.

For tropical sawnwood, import value of USD543M was

29% up on the same period last year while quantity

increased 25% to 447,600 tonnes. Import value of tropical

mouldings/decking was USD271M in the first seven

months of this year, a gain of 43% compared to the same

period in 2021, while quantity increased 3% to 117,000

tonnes.

There were also large gains in EU27 imports of tropical

joinery products (+43% to USD178M, +29% to 67,000

tonnes), tropical veneer (+24% to USD142M, +25% to

94,800 tonnes), plywood (+66% to USD141M, +30% to

82,200 tonnes), marquetry (+69% to USD73M, +49% to

12,400 tonnes), flooring (+33% to USD51M, +23% to

16,500 tonnes) and logs (+14% to USD37M, +12% to

61,600 tonnes) .

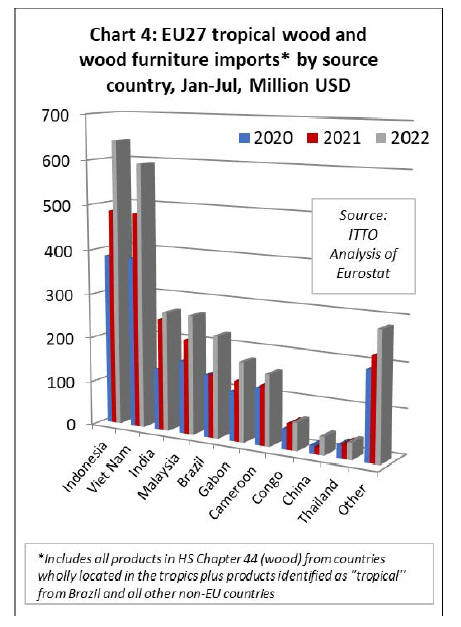

In terms of source countries, EU27 imports of wood and

wood furniture in the first seven months this year were up

significantly compared to the same period last year:

Indonesia (+33% to USD643M, +6% to 162,600 tonnes),

Vietnam (+23% to USD593M, +4% to 138,400 tonnes),

Gabon (+32% to USD179M, +29% to 160,400 tonnes),

Brazil (+60% to USD228M, +27% to 150,200 tonnes),

Cameroon (+19% to USD160M, +21% to 162,200

tonnes),

Republic of Congo (+6% to USD63M, +12% to 68,100

tonnes),

and

Cote d'Ivoire (+15% to USD37M, +7% to 28,700 tonnes).

While import value from Malaysia increased 24% to

USD267M, import quantity was flat at 101,000 tonnes.

Import value from India increased 7% to USD268M but

import volume fell 7% to 63,300 tonnes during the seven

month period (Chart 4).

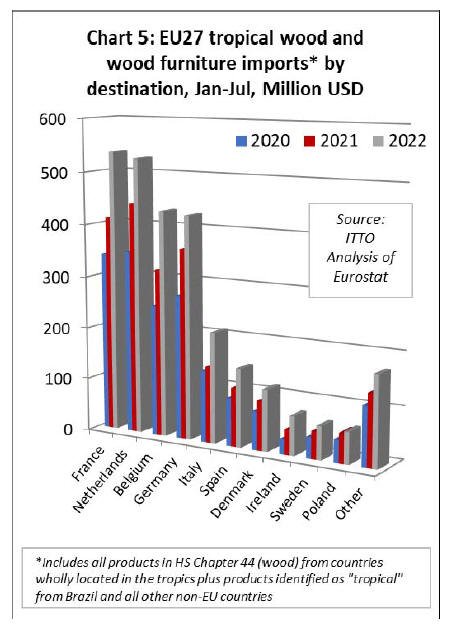

EU27 import value of tropical wood and wood furniture in

the first seven months this year increased into all the

leading EU destinations for these products, while import

quantity increased into all destinations except Germany.

Trends into the main import destinations were:

France (+30% to USD537M, +8% to 233,100 tonnes);

Netherlands (+19% to USD526M, +9% to 204,800

tonnes);

Belgium (+35% to USD431M, +18% to 287,800 tonnes);

Germany (+17% to USD426M, -1% to 120,100 tonnes);

Italy (+47% to USD211M, +44% to 112,400 tonnes);

Spain (+34% to USD148M, +35% to 62,700 tonnes); and

Denmark (+23% to USD116M, +11% to 28,600 tonnes)

Sharp deterioration in European economic indicators

The latest eurozone economic update by ING Group, the

Dutch multinational banking and financial services

corporation, reports that “after a deceleration in economic

growth over the summer months, eurozone indicators

strongly deteriorated in September, suggesting the start of

a recession. The challenges that the eurozone economy has

been facing over the last few months have not

disappeared. If anything, they have got worse”.

The ING Group particularly highlight the impact of the

war in Ukraine on energy prices in Europe and the effects

of this on the wider economy: “natural gas exports from

Russia to the European Union have been cut further and

the sabotage of the Nord Stream 1 and 2 pipelines has

created some fears regarding the safety of the gas pipelines

from Norway. Unfortunately, according to the latest

weather analyses, the risk of a cold winter has risen”.

With mounting concerns on the supply side, ING Group

“continue to expect very tight natural gas markets over the

winter months, keeping prices at uncomfortably high

levels. Moreover, because of the lack of natural gas

imports from Russia, prices are not likely to fall

significantly in 2023. This will hurt the supply side of the

economy, with a growing number of European companies

reducing production. And while governments have stepped

up their support for households and businesses, we still

believe that consumption will contract. At the same time,

increasingly tight financial conditions are another

headwind for growth”.

ING Group go on to suggest that “while the deceleration

of economic activity seemed to be limited during the

holiday season, the September data now clearly screams

recession”.

They point to the latest figures from the S&P Global

Eurozone Composite Purchasing Managers Index (PMI)

which stood at 48.2 in September, well below the 50

boom-or-bust-level.

According to ING Group “With inventories building on

the back of slowing sales, eurozone manufacturers reduced

their purchases of inputs for the third month in a row.

Consumer confidence fell in September to the lowest level

since the survey started, with households especially

worried about their financial situation over the next 12

months”.

ING Group note that the eurozone inflation rate rose to

10% in September. Energy prices were the main culprit,

but core inflation excluding energy also rose to 4.8%. The

European Central Bank is therefore expected to become

more aggressive in raising interest rates. ING Group are

forecasting a 75bp hike in October, followed by 50bp in

December and 25bp in February 2023, bringing the

deposit rate to 2.25%.

ING Group forecast a small negative GDP growth figure

for the eurozone in the third quarter of 2022 and a deeper

downturn over the winter months. For next year, ING

Group anticipate a 0.8% GDP contraction, after a 2.9%

expansion in 2022.

Being particularly sensitive to changes in mortgage

interest rates - and following a big short-term boost to

activity in the immediate aftermath of the COVID-19

pandemic - the downturn in the eurozone construction

sector is expected to be even larger than in the wider

economy. The S&P Global Eurozone Construction Total

Activity Index was well below the no-change mark of 50.0

for the fifth successive month in September, at 45.3. The

figure for Germany, at 41.8, was particularly low. The

figures for Italy (46.7) and France (49.1) were closer to

neutral territory.

Broken down by sector, the S&P Index showed that

housing activity in the Eurozone during September fell at

the fastest rate since May 2020. The fall in the Index was

less dramatic for civil engineering and commercial

activity, but still below the no-change mark.

New orders placed with eurozone construction companies

declined for the sixth successive month in September and

the rate of contraction quickened for the fifth month

running to the sharpest since May 2020. Data broken

down by country showed that a much a steeper reduction

in Germany drove the overall acceleration, offsetting

softer falls in both France and Italy.

September data revealed a worsening degree of pessimism

among eurozone construction companies regarding the

year-ahead outlook for business activity. Companies were

at their most downbeat since the first COVID-19

lockdown in April 2020, reflecting the growing risk of

recession in the wider economy.

German construction firms were at their most pessimistic

since March 2020, while their French counterparts were

less downbeat than in August and Italian firms were

modestly optimistic.

Commenting on the latest results, Trevor Balchin,

Economics Director at S&P Global Market Intelligence,

said: "September data rounded off a very weak third

quarter for the eurozone construction sector. Outside of the

pandemic, the rate of decline in activity in the third quarter

was the strongest since the fourth quarter of 2014. Activity

fell sharply again in September, with Germany posting a

notably steep rate of contraction. The overall pace of

decline eased due to slower falls in France and Italy,

although this masked a worsening outlook as both new

orders and firms' 12-month expectations sank deeper into

negative territory”.

European Parliament and Council start joint

negotiations on new deforestation law

On 13 September 2022, the European Parliament adopted

its position (the "Parliament Position”) regarding the

Proposal for a Regulation on Deforestation-Free Products

(the “Proposal”), published by the European Commission

on 11 November 2021. The Council of the EU had

adopted its general approach on the Proposal on 28 June

2022 (the “Council Approach”).

The first Trilogue for the regulation was held in the last

week of September. Trilogues are informal tripartite

meetings on legislative proposals between representatives

of the Parliament, the Council and the Commission. Their

purpose is to reach a provisional agreement on a text

acceptable to both the Council and the Parliament.

The EU hope to reach political agreement on the Proposal

before the COP15 on Biodiversity in December in

Montreal. Trilogues are an informal procedure with no

pre-set timeline, but the process typically averages 3 to 6

months.

Once political agreement between the Parliament and

Council has been reached, the agreed text would still need

to be formally endorsed by both legislative bodies, the

timing dependent on political urgency and other factors.

Once adopted, the main obligations imposed by the

Proposal would then apply 12 months (or 18 months as per

the Council Approach) from its entry into force, except for

microenterprises (and for SMEs as per the Parliament

Position) for which it would only apply 24 months after

the entry into force.

The three versions of the law on which the Trilogue

negotiations are based are available as follows:

Commission Proposal of 11 November 2021:

https://environment.ec.europa.eu/document/download/5f1b726e-d7c4-4c51-a75c-3f1ac41eb1f8_en?filename=COM_2021_706_1_EN_ACT_part1_v6.pdf

European Council Approach adopted 28 June 2022:

https://data.consilium.europa.eu/doc/document/ST-10284-2022-INIT/en/pdf

European Parliament Position adopted 13 September

2022:

https://www.europarl.europa.eu/doceo/document/TA-9-2022-0311_EN.pdf

Although the EU institutions are broadly aligned on

overall approach and objectives, the Parliament and the

Council have suggested a number of changes to the

Proposal. The Parliament, in particular, wants an enlarged

scope of application (which would include financial

institutions) and an extended range of penalties. A recent

independent comparison of the three positions by

Linklaters, an international law firm, is available at:

https://sustainablefutures.linklaters.com/post/102hydp/eudeforestation-proposal-next-steps

A new independent analysis of the implications of the law

for the tropical timber trade by Alain Karsenty Fondation

pour la Nature et l’Homme is available:

In French:

https://www.fnh.org/wpcontent/uploads/2022/09/TT-contribution-deforestation.pdf

In English:

https://www.atibt.org/files/upload/news/EU_REGULATION/The_draft_European_regulation_on_imported_deforestation.pdf

Recent timber trade and industry comments on the law

include:

Open Letter of 7 September 2022 from CEI-Bois, EOS,

ETTF and ATIBT:

https://www.ceibois.org/_files/ugd/5b1bdc_9f34319605d844ec8fe606682f90f14d.pdf

Considerations of the European forest-based industries on

the proposal for a regulation on deforestation and forest

degradation adopted by the European Parliament signed by

some of the leading European forest products industry

associations:

https://www.ceibois.org/_files/ugd/5b1bdc_bb2d941402734f90b3883eb1f12387ca.pdf

Independent press commentary on the legislation,

including free access to an on-line event at which

representatives from the commercial food and agriculture

sectors, academics and NGOs discuss some of the wider

implications of the legislation, is available at:

https://www.foodnavigator.com/Article/2022/10/07/do-duediligence-laws-actually-promote-climate-smart-food

https://www.foodnavigator.com/Article/2022/08/25/duediligence-obligations-a-golden-opportunity-for-transparentsupply-chains-or-a-costly-administrative-nightmare

European Parliament wants new FLEGT VPAs with

more partners

There is only passing reference in these various

commentaries on the future role of the existing FLEGT

VPA process and licenses in the prospective EU

deforestation-free regulatory framework. More insight is

gained from review of the three versions of the law now

being considered.

The European Parliament Position would suggest a larger

long-term role for the existing FLEGT VPA framework

than implied in the original legislative proposal or Council

Approach.

Both the original Commission Proposal and the Council

Approach note that the EU Fitness Check of the FLEGT

regulation and EUTR had determined that "while the

legislation has had a positive impact on forest governance,

the objectives of the two Regulations – namely to curb

illegal logging and related trade, and to reduce the

consumption of illegally harvested timber in the EU –

have not been met".

Both the original Proposal and the Council Approach also

state that “To respect bilateral commitments that the

European Union has entered into and to preserve the

progress achieved with partner countries that have an

operating system in place (FLEGT licensing stage), this

Regulation should include a provision declaring wood and

wood-based products covered by a valid FLEGT license as

fulfilling the legality requirement under this Regulation.”

There is no provision in either text for the FLEGT licenses

developed under the existing VPAs to fulfil either the

deforestation-free or forest degradation-free requirement

under the regulation. Instead there is a reference to a new

form of partnership with producer countries “to jointly

address deforestation and forest degradation”.

These new partnerships “will focus on the conservation,

restoration and sustainable use of forests, deforestation,

forest degradation and the transition to sustainable

commodity production, consumption processing and trade

methods”. They may include “structured dialogues,

support programmes and actions, administrative

arrangements and provisions in existing agreements or

agreements that enable producer countries to make the

transition to an agricultural production that facilitates the

compliance of relevant commodities and products with the

requirements of this regulation”.

Unlike the FLEGT VPAs, there is no expectation in the

original Proposal or the Council Approach that these

partnerships should lead to “licensing” of products

explicitly to ensure compliance with the EU’s

deforestation-free legislation. Instead, the agreements and

their effective implementation would be taken into account

when countries and sub-national jurisdictions are

benchmarked by the European Commission into three risk

categories; “High risk”, “Low risk”, and “Standard risk”.

For products from “low risk” countries or subnational

jurisdictions operators would apply a “simplified due

diligence”. Competent authorities would apply enhanced

scrutiny on relevant products from “high risk” countries or

subnational jurisdictions.

While the Parliament Position adopts much the same

approach, it is notable for containing a more nuanced

analysis of the value of the FLEGT process.

On the EUTR and FLEGT VPA legislation, the Parliament

Position is that "the performance and implementation of

the two Regulations underwent a fitness check which

found that, while both achieved some success, a number of

implementation challenges have held back progress

towards achieving fully their objectives.

The application and functioning of the due diligence

scheme under [the EUTR] on the one hand, and the limited

number of countries involved in the VPA process, with

only one having thus far an operating licensing system in

place (Indonesia), on the other, curtailed effectiveness in

meeting the objective of consumption of illegally

harvested timber in the EU”.

The Parliament Position also goes into more detail on the

purpose of the VPAs and envisages a continuing role for

FLEGT licensing. It notes that “VPAs are intended to

foster systemic changes in the forestry sector aimed at

sustainable management of forests, eradicating illegal

logging and supporting worldwide efforts to stop

deforestation. VPAs provide an important legal framework

for both the Union and its partner countries, made possible

with the good cooperation and engagement by the

countries concerned. New VPAs with additional partners

should be promoted”.

The Parliament Position also states that other partners

should be encouraged to work towards reaching the

FLEGT Licensing stage and that the “VPA partnerships

should be supported with adequate resources and specific

administrative and capacity building support”. The

Parliament Position is also more expansive on the content

of the new partnerships proposing that they “shall ensure

that indigenous peoples, local communities and civil

society, are involved in the development of joint

roadmaps” which “shall be based on milestones agreed

with local stakeholders”.

The Parliament Position is that the Commission should

“particularly engage with producing countries to remove

legal obstacles to their compliance, including national land

tenure governance and data protection law”, and that

partnerships should be “with countries and parts thereof

identified as high-risk, to support their continuous

improvement towards the standard risk category”.

The Parliament Position also emphasises that the new

partnerships should “pay particular attention to

smallholders in order to enable these smallholders to

transition to sustainable farming and forestry practices and

to comply with the requirements of this Regulation,

including through enabling sufficient and user friendly

information”. Specifically, that “adequate financial

resources shall be available to meet the needs of

smallholders”.

Clarity on the long-term role of the existing VPAs and of

FLEGT licensing and on the relationship between the

existing VPAs and new forest partnerships will only

emerge once the on-going Trilogue negotiations are

concluded and a final text of the new deforestation law is

agreed.

|