|

Report from

Europe

Rollercoaster ride for UK tropical wood imports

UK GDP increased 7.5% in 2021, the fastest annual

growth rate in the UK since the Second World War

and making the UK one of the world's fastest

growing economies last year. But this "rise" must be

considered in the light of the UK being amongst

countries worst affected by the COVID-19 pandemic

which led to a 9.4% fall in GDP in 2020 at a time

when there was already uncertainty due to the

countryˇŻs departure from the EU.

UK imports of tropical wood and wood furniture

products have mirrored the rollercoaster ride in the

wider economy. Total UK tropical wood and wood

furniture imports in 2021 were US$1.31 billion, 27%

more than the previous year. This followed a 21%

decline in 2020 when supply and demand were

severely affected in the early phase of the pandemic.

In practice, the value of UK imports of tropical

products last year was only a marginal gain compared

to US$1.30 billion in 2019 before the pandemic and

is no significant increase on the long-term average in

the last ten years (Chart 1).

While UK imports of tropical wood and wood

furniture increased last year, tropical products have

suffered a significant loss of market share during the

pandemic (Chart 2). The total value of UK imports of

wood and wood furniture products from all countries

increased from US$8.94 billion in 2020 to US$12.65

billion last year, a gain of 42% after a 5% fall the

previous year.

The share of tropical products in total imports was

only around 10% last year, well below the long term

average of between 13% and 14% share.

In contrast to tropical products the share of UK

import value of non-tropical products from China

remained level at 23.5% in 2021 as the value

increased by 43% to US$2.99 billion during the year.

The share of UK imports of non-tropical products

from other lower and middle income (LMI) countries

increased from 5% to 6% as the value increased by

57% to US$720 billion in 2021. This was largely due

to a near doubling in UK imports from Russia and

Turkey during the year.

However, in terms of absolute value, the largest gains

in UK imports during 2021 were made by EU27

countries.

The total value of UK imports of wood and wood

furniture from the EU27 increased 46% to US$6.73

billion in 2021. This followed only a 1% decline the

previous year despite the onset of the pandemic.

The share of EU countries in UK imports increased

progressively from 49.5% in 2019 to 52% in 2020

and 53% in 2021. Expectations that the UK's

departure from the EU might lead to a decrease in the

share of imports of wood and wood furniture from

the EU and a switch to other regions have yet to be

realised.

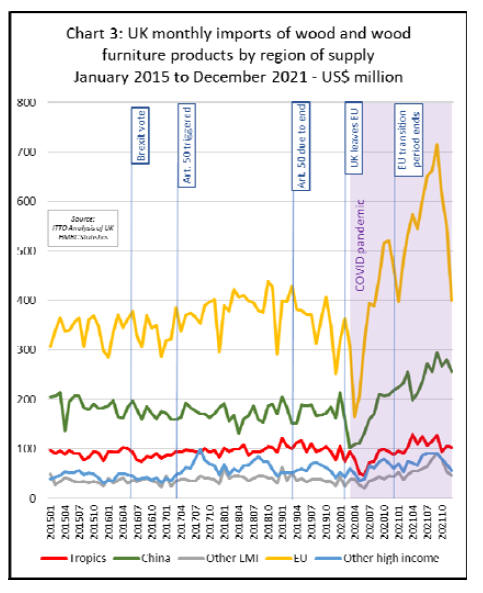

Recent trends in UK wood and wood furniture

imports were strongly influenced by the combined

effects of the pandemic and Brexit (Chart 3).

In the two and a half years following the UK's

decision to trigger Article 50 of the EU Treaty on 29

March 2017 which began the formal process for

withdrawal from the EU, a process eventually

completed January 2020, UK imports of wood and

wood furniture from the rest of EU were more

volatile than usual. However, there was no significant

change in share of overall UK imports sourced from

the EU and other regions of supply during this

period.

The pattern changed dramatically from February

2020 just after the UK's departure from the EU and

with the onset of the pandemic. This led to a sharp,

but very brief, downturn in UK imports of wood and

wood furniture from all regions, including the EU,

during the first period of lockdown in April and May

2020.

But UK demand for wood products increased rapidly

thereafter as consumers spent less money on

transport, holidays and eating out, and invested large

sums in home and garden improvement. Spending

was further boosted by low interest rates and a huge

injection of government support to tide the economy

over the pandemic.

The sharp recovery in demand in the UK in the

second half of 2020 and in 2021 coincided with a

severe shortage of container space and other

logistical problems in other parts of the world leading

to a big rise in UK wood products imports from the

EU.

At the same time, the full effects of the new customs

controls on imports from the EU following the UK's

departure from the EU were yet to be felt last year.

Unlike the EU, which immediately imposed full

inspections on imports from the UK in January 2021,

when the Brexit transition period came to an end, the

UK introduced a phased approach.

A grace period was granted to UK importers to give

them more time to adapt to the new rules and ways of

working.

The UKˇŻs originally intended that requirements for

phytosanitary certification of UK imports from the

EU would be introduced from April 2021 while

requirements for full customs declarations on

entering the UK market, rather than submitting forms

at a later date, would be introduced from July 2021.

However, these deadlines were progressively pushed

back during 2021. In the end, full customs

declarations and controls on UK imports from the EU

were only introduced on 1 January 2022, while

requirements for phytosanitary certification and

physical sanitary checks on controlled products are

now only due to be introduced on 1 July 2022.

It seems likely that the huge surge in UK imports of

wood products from the EU in the first three quarters

of 2021 was partly driven by the desire of UK

importers to build stock in advance of introduction of

full customs checks.

The pace of UK imports from the EU fell

dramatically in the last quarter of last year, with

importers carrying higher stocks into the (typically

slower) winter season and with some signs of

slowing construction sector activity.

Uncertain prospects in UK as economic and

logistics problems mount

Now there is a considerable uncertainty as to how

UK imports will develop during 2022, both in terms

of absolute numbers and in the balance between

imports from the EU and the rest of the world.

The headline figures look quite promising. The latest

OECD outlook indicated that the UK economy will

continue to recover in 2022 with overall growth

moderating to 4.7% during the year. Construction

activity in the UK has been robust and seems quite

resilient, despite material shortages and rising energy

costs.

The IHS Markit/CIPS UK Construction Purchasing

Managers index registered 56.3 in January, up from

54.3 in December, the strongest rate of output

expansion since July 2021.

At the same time, concerns about the effects of the

COVID omicron variant have waned in the UK as

cases and deaths have fallen sharply in recent weeks

and the UK government has indicated that all COVID

restrictions should be lifted before the end of

February.

On the downside, consumer price inflation in the UK

is currently around 5.4%, with energy prices rising

very rapidly. A recent article in the Financial Times

(FT) notes that UK growth rate has also been

artificially boosted by £25bn of corporate tax

incentives and that real business investment remains

weak.

In the third quarter of 2021, investment was still 4%

below pre-pandemic levels, lower than any other

economy in the G7. And UK exports have not joined

in the global boom. According to the FT, "all this

suggests that businesses are looking relatively

unfavourably on the UK, even before corporation tax

rates rise from 19 per cent to 25 per cent in 2023".

As to where the UK will turn to for wood products

during 2022, that will heavily depend on supply side

issues, including access to log supplies, availability

and prices for containers, shifting exchange rates,

level of demand in other markets, as well as policy

measures.

It seems unlikely that UK imports from the EU in

2022 will be anywhere close to the level of 2021 as

customs controls are finally introduced and

merchants are carrying heavier stocks than the same

time last year.

On the other hand, problems of shipping and

transport logistics have become particularly

prominent in the UK market in recent months and

these may yet tie importers even more closely to their

traditional European suppliers of wood products,

irrespective of Brexit.

A recent study conducted by global logistics platform

Container xChange and applied research organisation

Fraunhofer-CML revealed that the UK currently has

the worldˇŻs longest turnaround times for processing

shipping containers.

Due to the combined effects of Brexit and COVID, it

is taking an average of 51 days for cargo boxes

carrying goods from China and Southeast Asia to be

processed in UK ports due to port congestion,

shortage of warehousing space and lack of truckers

and other qualified staff. This compares to around 25

days in Germany (the next worst performing

European country) and as little six days in China.

The problems of shipping into the UK have led to

more calls for distributors and manufacturers to shift

away from their existing "just-in-time" business

model to a "just-in-case" model of bringing more

manufacturing closer to home and increasing

inventories once again.

In practice, this implies a continuing high level of

dependence on the large suppliers in continental

Europe for which turnaround times, while much

longer than before the UK left the EU single market,

still compare favourably to imports from other parts

of the world.

There are a few positive signs that global supply

chains may start to unclog before the end of this year.

For example, the FT was told by shipping giant AP

Moller-Maersk that it expects global supply chain

struggles to slowly get back toward normal in the

latter part of 2022. And while global container prices

have been very volatile around Chinese New Year,

they have eased a little from the heights reached in

the third quarter last year.

But overall, on-going supply side problems, which

are particularly pronounced for shipments into the

UK, suggest that there is unlikely to be a more

significant upturn in UK imports of wood and wood

furniture products from tropical countries during

2022.

|