Japan

Wood Products Prices

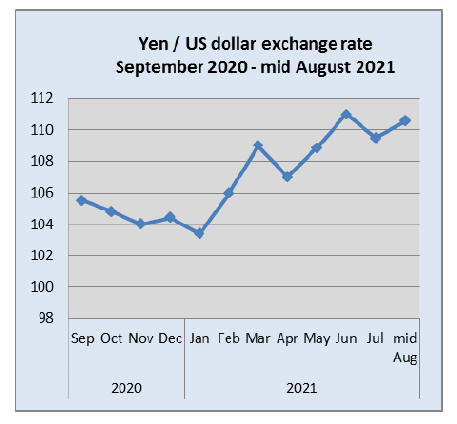

Dollar Exchange Rates of 10th

Aug

2021

Japan Yen 110.44

Reports From Japan

Corona update

Newly reported COVID-19 cases in Japan exceeded

15,000 for the first time on 5 August and Tokyo reported a

record high 5,042 new cases. Tokyo has been under a state

of emergency since 12 July. In an attempt to curb the

rising infections, Japan expanded emergency restrictions

to eight more prefectures, Fukushima, Ibaraki, Tochigi,

Gunma, Shizuoka, Aichi, Shiga and Kumamoto.

Olympic cost overun

The cost of the just-ended Tokyo Olympics greatly

overrun initial estimates. The Olympics were held without

spectators at almost all venues meaning most of the

US$800 million in estimated ticket revenues did not

materialise. The costs for the games had already ballooned

due the one-year postponement amid the global health

crisis and anti-virus measures and increased construction

expenditures for the venues pushed costs higher.

The total costs for the Tokyo Olympics and Paralympics

were estimated at ¥734 billion but this had grown to ¥1.64

trillion in December 2020.

July consumer confidence improves despite new state

of emergency

The Cabinet Office Consumer Confidence survey for July

reported a 17-month high, returning to pre-pandemic

levels despite a resurgence in infections that forced the

government to declare the fourth state of emergency.

Consumers surveyed were more optimistic about their

livelihood prospects, jobs and suggested government

spending and strong exports boosted confidence.

Japan's seasonally-adjusted consumer confidence index

stood at 37.5 in July, up from 37.4 in June to mark the

second straight month of increase. The Cabinet Office

survey said "While still in a severe state, consumer

confidence continues to recover". While the latest

lockdowns dashed policymakers' hopes for a strong

rebound in the third quarter the government still maintains

GDP will be back to pre-pandemic levels at the end of

2021 but this has not been borne out in a survey of the

private sector.

An NHK survey has found that more than 70 percent of

major companies in Japan expect the economy to recover

to pre-pandemic levels next year and beyond.

Asked when the economy would return to pre-pandemic

levels, 5 companies said in the latter half of this year, 30

said in the first half of 2022 while 24 companies said in

the latter half of 2022. 8 companies said in the first half of

2023 and another 8 said in the latter half of 2023. 3

companies said in the first half of 2024.

Agricultural and forestry exports rise

JapanˇŻs Minister of Agriculture, Forestry and Fisheries,

Kotaro Nogami, reported in an online press conference on

3 August that JapanˇŻs exports of agriculture, forestry and

fishery products increased by 31.6 percent in the first half

of 2021 from the same period last year, the highest ever

for the first half of a year.

Throughout 2020 there was a steady increase in the

exports of Japanese cedar logs to China and this continued

into the first half of 2021. China accounted for the largest

share followed by the Philippines, the United States, South

Korea and Taiwan P.o.C.

Rising raw material costs

Wholesale prices in Japan rose at their fastest annual pace

in July a sign that rising global commodity prices and a

weak yen has pushed up the cost of imported raw

materials. This has become a concern for Japanese

manufacturers as they slowly resume production.

In the second quarter of this year major manufacturers

reported strong export demand especially in the US and

China but optimism is tempered as rising raw material

costs will push up production costs.

The current state of domestic demand is not strong

so

companies hesitate to pass on higher raw material costs to

consumers by raising prices.

JapanˇŻs economy had been showing signs of recovery

with rising exports offsetting weak domestic consumption

but with another state of emergency announced there are

doubts that the pace of recovery can be maintained.

See:

https://www.japantimes.co.jp/news/2021/08/12/business/economy-business/wholesale-inflation-hits-13-year-high-japan-costsimports-rise/

New regulations on home energy saving being

considered

There are on-going discussions on making it mandatory

for new homes to meet energy-saving standards as the

household sector is estimated to account for roughly 15%

of carbon dioxide emissions in Japan and excessive

hosehold power consumption because of poor insulation is

one major factor.

To meet a target of reducing the average energy loss of all

newly built homes to zero by 2030 the government is

promoting ˇ°net-zero energy housesˇ±.

Some local governments have already adopted energysaving

targets for the household sector. In 2020 the

government of Tottori Prefecture introduced a programme

to certify the heat insulation of homes.

House builders are concerned about the impact of these

measures as they will result in increased house prices.

Import update

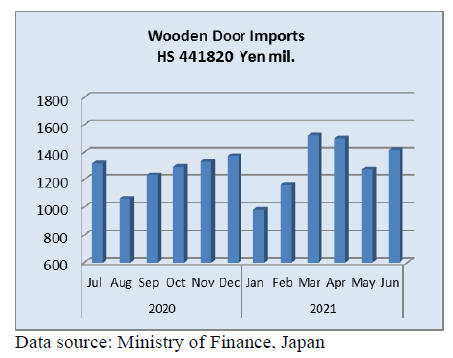

Wooden door Imports

JapanˇŻs imports of wooden doors (HS441820) in the first

half of 2021 were up 16% on the value of first half 2020

imports but still below levels reported in the first half of

2019. Year on year, the value of June 2021 imports of

wooden doors were 12.5% higher and compared to a

month earlier there was a 12% increase.

As in previous months shippers in China and the

Philippnes accounted for over 80% of June imports of

wooden doors with Malaysia accounting for around 3% of

June imports. The combined value of wooden door

shipments from suppliers in Europe amounted to 6% of the

value of June arrivals.

Wooden window imports

Looking at the 12 month trend in the value of wooden

window (HS441810) imports it would appear there has

been a substantial improvement however, in the first half

of 2021 the value of window imports was down on 2020

and down a massive 60% on the value of 2019 imports.

Compared to a month earlier, the value of June window

imports were little changed but year on year there was a

5% rise. There has been a steady rise in the value of

wooden window imports between January and May this

year but this upward trend stalled in June.

Shippers in China accounted for 41% of June arrivals

of

wooden windows followed by the US at 35%. June

shipments from the Philippines dipped to 14% of all June

arrivals marking a decline on the value of May shipments.

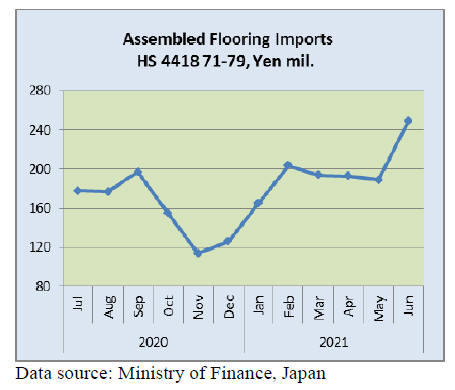

Assembled wooden flooring imports

In the first half of 2021 JapanˇŻs imports of assembled

wooden flooring (HS441871-75) were around the same

level as in 2020 but some 25% below the value of first half

of 2019 imports.

Year on year, the value of JapanˇŻs imports of assembled

wooden flooring (HS441871-79) in June jumped a

remarkable 84% and compared to the value of May

imports there was an over 30% increase.

As in previous months imports of HS441875 acounted for

most assembled flooring imports with most (43%) being

shipped from China. Shippers in Vietnam have been

successful in capturing market share and accounted for

28% of all shipments of HS441875 in June.

In June this year shippers in Malaysia and Indonesia

together accounted for an increased share of imports at

over 12%, a better performance compared to May when

their combined shipments accouted for around 5% of

shipments of HS441875.

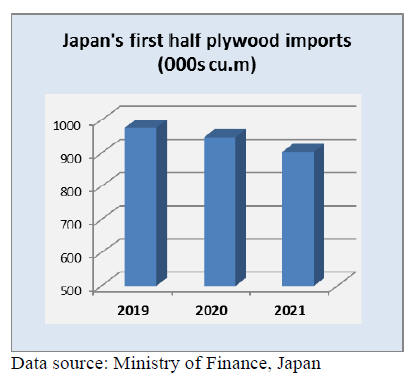

Plywood imports

Plywood imports to japan have been falling steadily for

several years. The volume of first half 2021 plywood

imports was down around 5% from that in 2020 and

around 7% lower than the volume of 2019 imports.

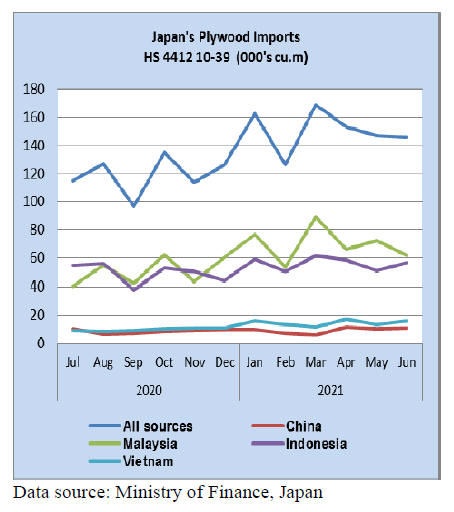

Year on year the volume of JapanˇŻs June imports of

plywood (HS441210-39) was up 8% but compared to May

the volume of imports was little changed.

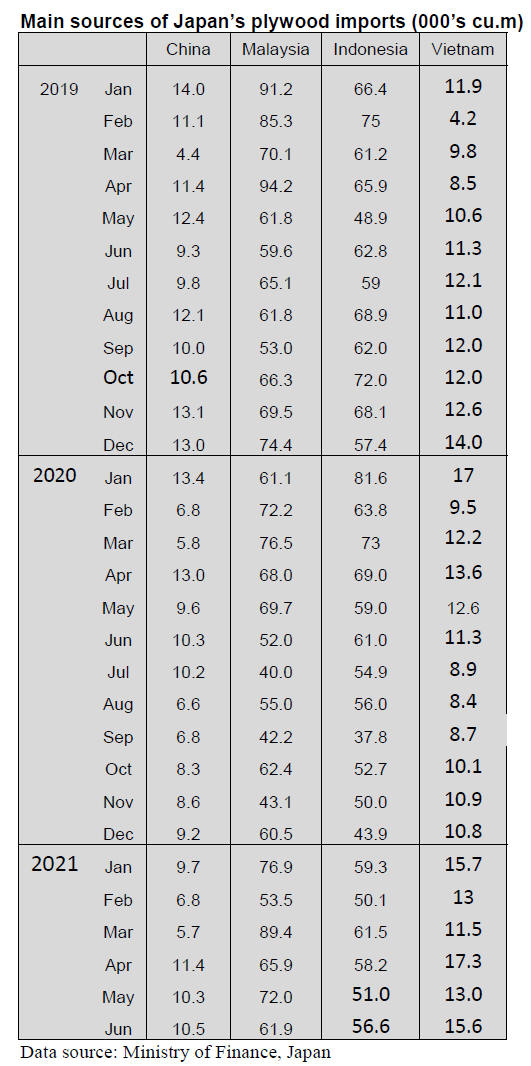

Of the four main shippers of plywood, Malaysia,

Indonesia China and Vietnam shipments from China were

flat compared to a month earlier, arrivals from Malaysia

were down but shipments from both Indonesia and

Vietnam improved on the May volumes. Shipments of

plywood from Vietnam to Japan are not large but June

shipments were considerably higher than in Juen 2020.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR.

For the JLR report please see:

https://jfpj.jp/japan_lumber_reports/

Front loading of national forest timber sales

With rapid increase of demand of domestic wood, four

regional offices of the national forest management decided

to move up timber sales. With sharp drop of demand,

overall supply reduction was done last year but now it is

reversing to increase the supply.

Log supply from the national forest is about 15% in total

log supply and it is functioning supply and demand. Log

supply shortage started in early this year in some areas and

three regional offices, Kyushu, Kinki/Chugoku and North

East moved up schedule of timber sales then Kanto office

decided to move up timber sales after July.

Log production depends on how soon timber buyers

harvest and produce logs for the market but more timber

sales are up for sale means log production should increase.

In Kyushu, normal bidding rate of timber sales is about

50% but in May, it is surprisingly high of 80% and the bid

prices also climbed. In the North East, snow removal on

logging road was made from beginning of the year to get

logs out, which is unusual event.

North American logs

It is reported that FAS prices of Douglas fir logs for Japan

market on July shipment are US$30 up per M

Scribner.Log market in local markets is rather quiet but

log production is dropping and higher prices are necessary

to secure enough volume.

Ocean freight tis also climbing so that CIF prices are more

than US$60 higher, which is about 1,500 yen per cbm

hike. The largest Douglas fir lumber manufacturer in

Japan announced to increase the sales prices by 15,000

yen per cbm on KD lumber and 10,000-12,000 yen on

green lumber since August 1 after considerable price

increase of competing European redwood laminated

beam for the third quarter.

Severe hot wave hit the West Coast is now gone but dry

condition continues without any rain fall so forest fires

could start up in any day now. Once restriction on logging

starts, log supply will decrease so log prices for August

and September are likely to stay high so domestic Douglas

fir lumber manufacturers would continue raising the sales

prices step by step.

FAS prices of Canadian Douglas fir logs for plywood

mills are about US$140 per cbm FAS, US$5 up from June.

CIF cost would be about US$210, US$10 up.Imported

cost would be about 24,800 yen per cbm CIF, 1,300 yen

up but plywood mills are anxious to procure as domestic

cedar log prices are soaring but like U.S.A., log production

is limited so there is not enough supply to satisfy the

Japanese demand.

Imports from Canada continue increasing month after

month. Total for the first five months is 329,324 cbms,

238.2% more than the same period of last year. The

increase is so conspicuous because last yearsˇŻ supply

dropped much by harvest stop of the largest supplier.

Douglas fir log supply increase by 29.9% from both

Canada and the U.S.A. This is only increased item when

all the other imported wood products decrease in wood

shock.

Radiata pine logs and lumber

Export industry is not active so that crating lumber

demand for export is dull but supply of crating lumber on

both domestic and import is limited so that the dealers are

trying to secure the volume.

Meantime, because of climbing prices of crating lumber,

some dealers are shifting to use other materials like

cardboard.

Chilean radiate pine lumberˇŻs number second ship arrived

in June. Compared to number one ship, the prices of

number two ship are US$25 per cbm C&F higher so the

dealers are increasing the sales prices.

DealersˇŻ prices on both thin board and square are 40,000-

43,000 yen per cbm. Number three ship will come in late

July, which prices are up by US$20-25 so the dealers need

to keep pushing the prices.

While the prices are climbing, dealersˇŻ inventory is getting

tight because shipsˇŻ interval stretched longer so the dealers

try to limit sales.

Distribution volume of domestic cedar crating lumber is

tight since sawmills concentrate manufacturing

construction lumber. The prices of cedar crating lumber

are also escalating and some prices are higher than Chilean

radiate pine lumber.

New Zealand radiata pine lumber manufacturing mills

announced to increase the sales prices of radiata pine

lumber by 10,000 yen per cbm to 60,000 yen after they

increased the prices in April by 5,000 yen. For crating

panel, Chinese poplar LVL prices are climbing.

Advancing cypress log prices

As reported in last edition, it is big surprise that regular

cypress log prices soared to record high price of 40,000

yen in June and the prices continue advancing. In July the

prices reached 46,000 yen in Shikoku then in Hyogo

prefecture, the auction price hit 48,000 yen. Domestic log

prices have started climbing since last March as a result of

shortage of imported wood products and extreme high

prices. Substituting demand increased in May.

Housing starts are almost the same as last year but

speculative demand pushed lumber prices higher, which

stimulates log demand. Lumber prices climb then log

prices follow to go up.

Plywood mills are also short of logs so that they buy logs

for lumber now. Normally A class logs are straight for

lumber manufacturing and B class logs for plywood. B

class logs are not as good as A class with some curve but

now there is no difference between A and B. Logs with

top diameter of 18-28 cm (nakame) are in high demand

now. Cypress nakame prices for plywood are 30,000 yen

and cedar logs for plywood are 15,000 yen.

There was some excess supply of lumber in March but

since last May, lumber supply became short and in July, it

is scramble to buy lumber. Cypress 4 meter sill square

wholesalersˇŻ prices are 135,000 yen per cbm and 3 meter

cedar post are 105,000 yen which was about 85,000 yen

about a month ago then shot up in short time.

In Kushu, prices of KD and green cypress sill lumber have

been fiercely soaring after cypress log prices reached

40,000 yen.

KD sill lumber prices are 140,000 yen from 80,000 yen a

month ago. Green sill lumber prices also jumped up to

90,000-100,000 yen from 60,000-70,000 yen a month ago.

Marketers comment that the prices would keep going up

toward fall demand.

In Northern Kyushu, KD cedar post prices are 110,000 yen

and cedar purlin prices are 90,000- 95,000 yen, 20,000 yen

up from June. KD cedar post prices are lower than

whitewood laminated post so the dealers are scrambling

but some are not able to procure so that some ordered

houses are short of post and are not able to start up. Some

predict that orders by precutting plants should slow down

so upward move of lumber should ease.

Changing North American lumber market

Average prices of 15 structural lumber dropped down to

US$689 per MBM in the second week of July, which is

continuous decline for seven straight weeks. Compared to

the last peak prices in the third week of May, it is drop of

US$ 825 (54.5%). Canadian SPF 2x4 #2 & better prices

are US$695 per MBM FOB mill, US$15 down from

previous week. Douglas fir KD 2x4 prices are US$850,

US$105 down and hemlock KD 2x4 prices are US$720,

US$165 down.

Compared to the peak prices, Douglas fir green lumber is

down by US$645 (45.8%), Douglas fir KD is down by

US$825 (49.3%) and KD hemlock is down by US$965

(57.3%). However, dropped prices of US$695 on average

15 structural lumber and US$695 on SPF are higher than

record high prices in 2018. Demand for housing has not

dropped that much so once the bottom is confirmed, the

prices are likely to rebound.

It is reported that abnormal high prices are caused by DIY

market where general consumers buy small volume at one

time for renovation of houses but now DIY market is

simmering down after vaccine shots prevailed and from

now on, the prices should settle at practical level.

Recent concern is forest fires on the west coast which

would affect logging activities and may cause log supply

shortage. There will not be any chance to see outrageous

high lumber prices but upward pressure would continue.

|