|

Report from

Europe

UK April tropical wood imports at highest since

2008-

09 financial crises

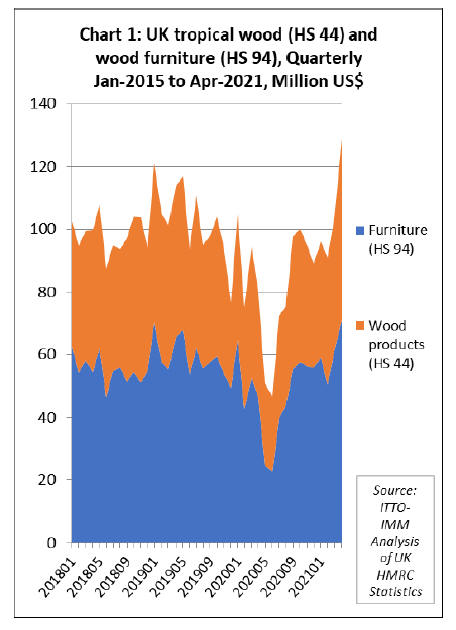

The UK imported tropical wood and wooden

furnitureproducts with a total value of USD419 million in

the first four months of 2021, an 18% increase compared

to the same period in 2020. There was a particularly sharp

increase in April when imports were USD129 million, the

highest monthly import value recorded since before the

financial crises of 2008-2009.

The strong performance in the first four months of this

year reflect both a robust rise in consumption in the UK,

supported by strong government stimulus measures, and

the late arrival of delayed shipments from the previous

year. The rise occurred despite severe logistical problems

that have emerged in shipment of tropical wood products

to the UK since the start of the pandemic.

BritainˇŻs economy surged in June as private-sector

businesses secured extra work and created thousands of

new jobs, but analysts warned the boom could be shortlived

if shortages of skilled staff and hold-ups to vital

supplies continue into the autumn.

The manufacturing and services industries, which account

for more than 80% of business activity, expanded at nearrecord

rates in June, according to a survey by IHS Markit,

building on the unprecedented burst in output growth in

May.

Firms were in a confident mood after the easing of Covid-

19 restrictions and a rush by consumers to shop and visit

bars and restaurants. Survey respondents were enjoying

higher domestic sales and higher demand from the US,

China and much of Europe for British goods and services.

The IHS Markit/CIPS flash UK output index measures the

difference between the proportion of employers who say

activity is above or below normal levels, where a figure of

50 separates contraction from expansion. The composite

index was 61.7 in June, while the manufacturing sector

posted a 64.2 figure, and the services industry stood at

61.7.

The UK construction sector, the leading driver of timber

demand in the country, has recovered even more strongly.

According to the IHS Markit/CIPS UK Construction

Purchasing Managers Index (PMI), UK construction

companies signalled an exceptionally strong increase in

output volumes in May, with continued recoveries seen in

civil engineering activity, commercial work and house

building.

The PMI posted 64.2 in May, up from 61.6 in April with

construction output growth reaching its strongest since

September 2014. New order volumes increased at the

fastest pace since the survey began just over 24 years ago.

Input cost inflation in the UK construction sector was also

at a survey-record high during May, reflecting a surge in

demand for construction materials and severe supply

shortages.

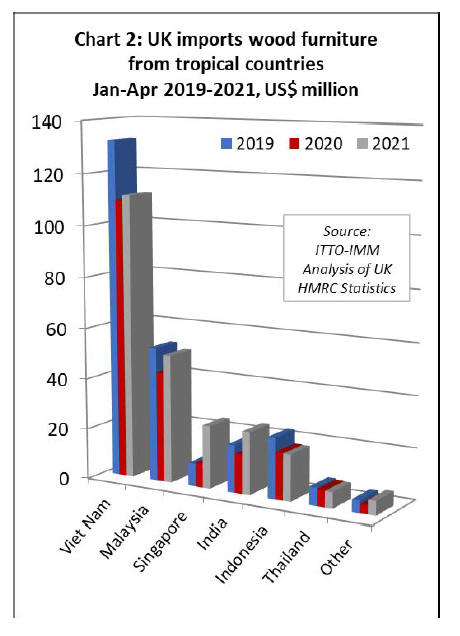

UK wooden furniture imports up 17% this year

Overall the UK imported USD241 million of tropical

wooden furniture products in the first four months of this

year, 17% more than the same period in 2020. In contrast

to 2020, when imports began to nose-dive in April with

the onset of the first COVID lockdown, UK imports of

wooden furniture in April this year, at USD71 million,

were at a higher level than in any other single month for

over a decade.

In April this year, imports of wooden furniture surged

from all the leading tropical countries supplying the UK

including Vietnam, Malaysia, India and Indonesia. Imports

from Singapore, which had been filling the supply gap due

to problems of shipment out of other South East Asian

countries earlier in the year, began to moderate during the

month.

Overall during the first four months of 2021, UK wooden

furniture imports were up from all four of the leading

tropical supply countries to this market; Vietnam (+2% to

USD112 million), Malaysia (+17% to USD50 million),

Singapore (+160% to USD25 million) and India (+59% to

USD25 million).

In contrast, imports from Indonesia, at USD18 million,

were still 1% behind the same period in 2020, while

imports from Thailand, at USD6 million, were 4% down

on last year (Chart 2).

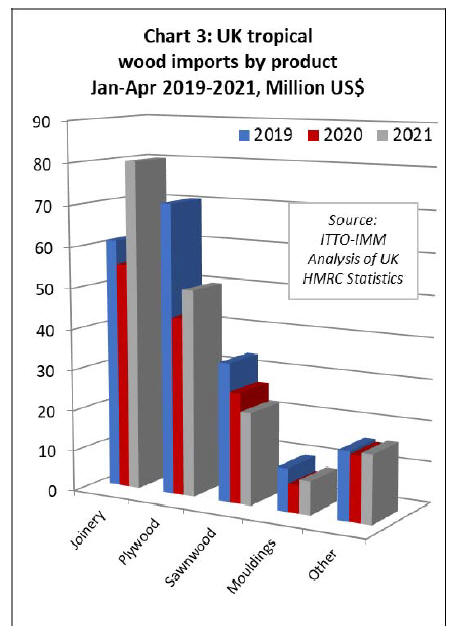

UK tropical wood imports rise 20%

UK imports of all tropical wood products in Chapter 44 of

the Harmonised System (HS) of product codes were

USD178 million in the first four months of 2021, 20%

more than the same period last year. With imports of

USD58 million in April 2021, this was the highest

monthly import value recorded since before the 2008-09

financial crises.

Comparing the first four months of 2021 with the same

period in 2020, UK imports of tropical joinery products

increased 45% to USD80 million while imports of tropical

plywood increased 16% to USD50 million and imports of

tropical mouldings/decking increased 20% to USD8

million. These gains offset a 16% decline in tropical

sawnwood imports to USD23 million (Chart 3 above).

After the sharp dip in UK imports of tropical joinery

products during the first lockdown period in Q2 2021,

imports gradually built momentum until March this year

and then surged in April. Imports from Indonesia, mainly

consisting of doors, were USD46 million in the first four

months of 2021, 46% more than the same period last year.

UK imports of joinery products from Malaysia and

Vietnam (mainly laminated products for kitchen and

window applications) also made strong gains in the first

four months of 2021.

Imports from Malaysia were USD20 million between

January and April this year, 34% more than the same

period in 2020. Imports of USD5.2 million from Vietnam

were 63% more than in the same period in 2020. UK

imports of joinery products consisting of tropical

hardwood from neighbouring Ireland also increased by

159% during this period, to USD3.8 million (Chart 4).

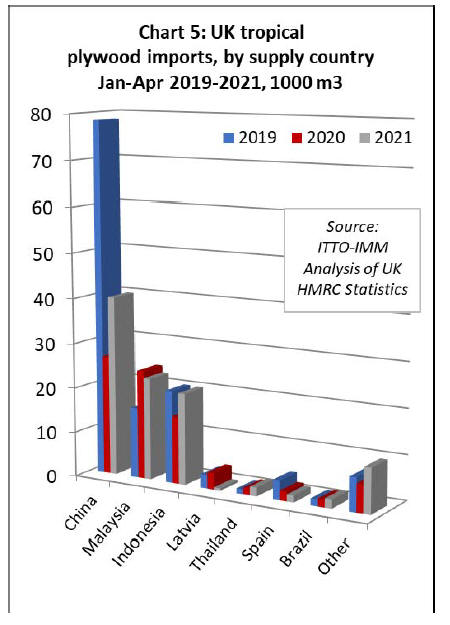

In the first four months of 2021, the UK imported 99,100

cu.m of tropical hardwood plywood, 22% more than the

same period in 2020. Imports from the UKˇŻs three largest

suppliers of tropical hardwood plywood ¨C China,

Indonesia and Malaysia ¨C have followed very different

trajectories this year (Chart 5).

The UK imported 40,000 cu.m of tropical hardwood faced

plywood from China in the first four months of this year,

51% more than the same period in 2020.

Imports from Indonesia also made gains during this

period, rising 36% to 20,400 cu.m. In contrast, imports of

22,700 cu.m from Malaysia in the first four months of

2021 were 6% down on the same period in 2020.

As with other hardwood product groups, UK demand for

tropical hardwood plywood has been strong this year,

driven by high levels of construction activity and

shortages of competing materials.

The main market challenges have been on the supply side,

notably the considerable escalation in freight rates on

Asian routes to the UK. In the past six months there was a

4-5 fold increase in container freights from South East

Asia. During December and January, this virtually halted

shipments of hardwood products from the region to the

UK.

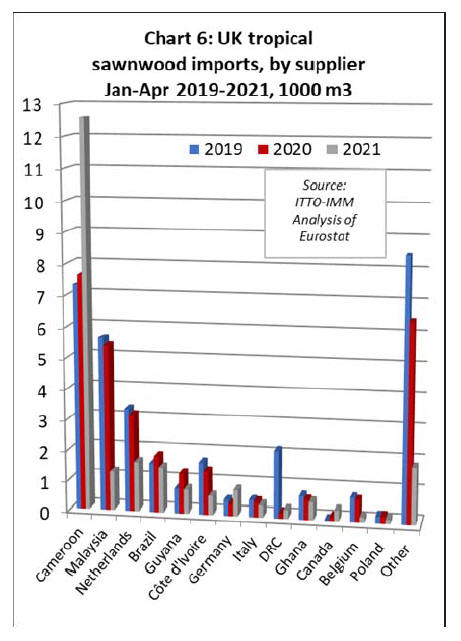

After falling sharply in May and June last year, UK

imports of tropical sawnwood strengthened between July

and December but the momentum has slowed this year.

UK imports were 23,000 cu.m in the first four months of

2021, 23% less than the same period in 2020. Although

imports from Cameroon, now by far the leading supplier

to the UK, increased by 64% during the four month

period, imports from all other leading tropical sawnwood

supply countries declined (Chart 6).

The large increase in imports of sawnwood from

Cameroon was due to the long lead time in shipment of

contracts placed back in 2020. UK importers now report

that supply for hardwoods from Cameroon and other

African supply countries is very limited.

Global demand for species such as sapele, sipo and iroko,

accompanied by production delays and logistical

difficulties, have been such that many African mills placed

a moratorium on taking new orders in late March and

throughout April this year.

The few mills with capacity to take orders which can be

produced and shipped relatively quickly are taking

advantage with high premiums being requested.

Even African hardwood species such as ayous and

okoume are limited in supply, in part due to the fact that

consumer markets are seeking new alternatives to their

customary products such as American tulipwood which is

hardly available at present.

UK imports of tropical sawnwood from Côte d'Ivoire were

no more than 630 cu.m in the first four months of this

year, 56% less than the same period in 2020.

The UK was previously a significant buyer of framire

from Côte d'Ivoire but UK importers report that this

species is proving increasingly difficult to source, both due

to a lack of raw material in the forest and the challenges of

obtaining assurances of legality that satisfy UK Timber

Regulation requirements.

UK imports of tropical sawnwood from Malaysia were

only 1,300 cu.m in the first four months of 2021, 77% less

than the same period last year.

Imports from Malaysia have been severely affected both

by production problems during pandemic and extreme

shortages of container space. The latter has led to the first

breakbulk shipments of Asian meranti and keruing lumber

into the UK for nearly 30 years, with the first arrivals in

May (and therefore not appearing in these statistics).

With shortages in supply from other sources, UK

importers were turning more to Brazil in the opening

quarter of the year, but imports from the country slowed

again in April. In the first four months of 2021, total UK

imports of tropical sawnwood from Brazil were 1,500

cu.m, 20% less than the same period last year.

Indirect UK imports of tropical sawnwood from other EU

countries also fell dramatically in the opening months of

this year. Total UK imports from EU countries were 3,800

cu.m in the first four months of 2021, 29% less than the

same period last year.

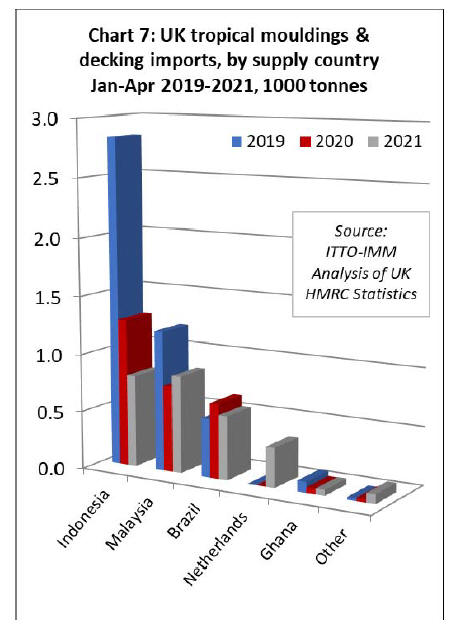

The UK imported 2,700 tonnes of tropical hardwood

mouldings/decking in the first four months of 2021, 7%

less than the same period in 2020. Imports declined 38%

from Indonesia to 800 cu.m and were down 15% from

Brazil to 500 cu.m. These losses were only partly offset

by a 13% rise in imports from Malaysia to 800 cu.m and

by imports from the Netherlands rising from close to zero

to 300 cu.m this year (Chart 7).

The TTF reports that the UK market is currently suffering

from severe lack of availability of bangkirai decking,

ˇ°initially due to the freight hikes at the beginning of the

year but, it seems, in the past 3 months or so, due to

suppliers selling UK bound stocks to other markets at a

time when the availability of (replacement) logs and

lumber suddenly dried upˇ±.

The number of Indonesian mills offering bangkirai for sale

to UK importers is now very restricted and the few offers

being made are ˇ°at prices about 50% higher than where

they were back in December which has led to significant

interest in cheaper Brazilian Decking speciesˇ±, according

to the TTF.

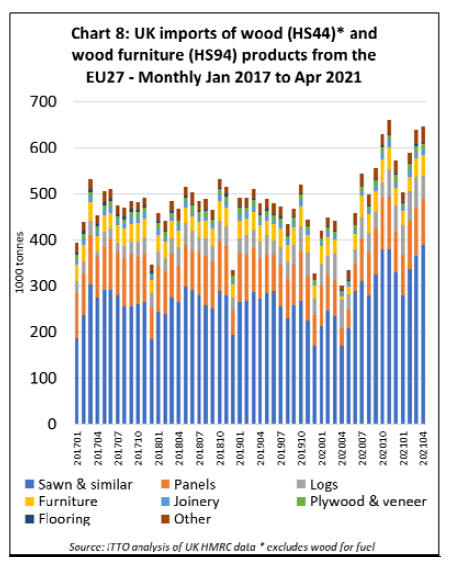

UK timber imports from the EU at record levels despite

Brexit

An impact of the UKˇŻs departure from the EU single

market and customs union on 1st January this year was

meant to be a decline in the quantity of UK timber imports

from the EU.

This forecast followed expectations of logistical problems

as new controls were introduced at the UK border,

increased scrutiny of the plant health and legal status of

EU wood products imported into the UK, and sluggish

economic activity in the UK due to post Brexit

uncertainty.

However, not only did UK imports from the EU fail to

decline in the opening months of 2021, but they were at

record levels for the time of year.

Chart 8 shows the quantity of UK imports of all wood and

wooden furniture products from the EU (excluding wood

for fuel) on a monthly basis since the start of 2017.

Following the dip in imports with the introduction of the

first lockdown in April and May last year, imports

recovered strongly through to November. They cooled a

bit in December and January, but less than usual for the

time of year, and then rebounded rapidly between

February and April.

In total, the UK imported 2.38 million tonnes of wood

products from the EU27 in the first four months of 2021,

47% more than the previous year, which of course was

COVID-affected, but also 21% more than in 2019, the last

ˇ°normalˇ± year. In fact, the quantity of UK imports of

wood and wooden furniture from the EU27 in the first four

months of 2021 was at the highest level since at least

2005.

Most of this growth was concentrated in softwood

sawnwood and logs and panel products, which dominate

UK imports from the EU27 (at least in tonnage terms).

However, imports of furniture and hardwood products

which compete more directly with imports from the

tropics also grew strongly from the EU in the opening

months of this year.

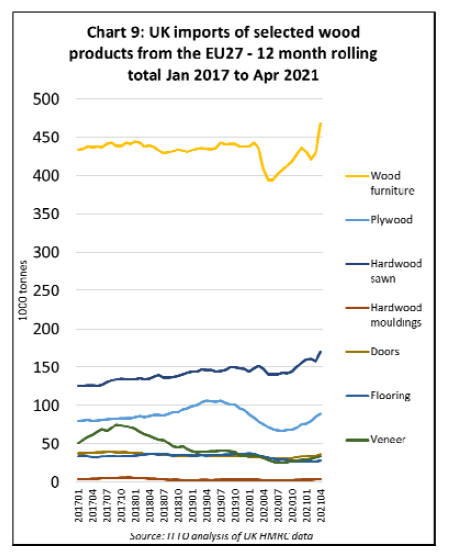

Chart 9 showing 12 month rolling total imports into the

UK from the EU27, highlights that following a sharp fall

in UK imports of wooden furniture from the continent

during the first lockdown in April/May last year, imports

gradually recovered in the second half of 2020. They then

weakened only slightly in January this year and surged in

March and April.

In contrast, a gradual long term rise in UK imports of

sawn hardwood from the EU seems to have been little

impacted by either the COVID lockdown or the UKˇŻs

departure from the single market.

UK imports of plywood from the EU27 fell sharply from

the middle of 2019, when the market was seriously

affected by over-stocking, and this downward trend

continued until the last quarter of 2020. However, UK

imports of plywood from the EU27 have been recovering

again this year.

Similarly, UK imports of flooring, doors and veneer were

all sliding throughout 2019 and 2020, but the downward

trend has haltered this year and there has been a slight

upturn.

Of course it is early days for the UK outside the EU single

market, and the UK timber market is currently

experiencing unprecedented conditions due to the COVID

pandemic. A massive government stimulus, including low

interest rates, a stamp duty holiday, and an additional £2bn

spending on infrastructure, has combined with a huge

surge in home and garden renovation activity as people

have either moved house or improved their existing

homes. Cash usually spent on vacations and other

recreational activities has instead poured into construction.

Meanwhile supplies of wood products from sources

further afield, in China, South East Asia, North and South

America, and Africa, have been severely disrupted. All

this has fed a huge upturn in UK demand for timber

imports from the EU and in prices which, for now, have

encouraged importers and distributors to overcome the

new logistical and bureaucratic challenges of sourcing

from the EU.

The only questions now are: for how long will this extraordinary

market situation in the UK continue; and, if and

when there is a return to ˇ°normalityˇ±, will the longexpected

UK pivot away from the EU to other supply

sources then take place or will the UKˇŻs renewed

dependence on EU suppliers be maintained for the longterm?

|