|

Report from

Europe

Sharp fall in UK tropical wood imports in 2020 likely

to

be short-lived

Total UK tropical wood and wood furniture imports in

2020 were USD981 million, 23% less than the previous

year (Chart 1a). The UK being amongst the worldˇŻs worst

affected countries by the COVID-19 pandemic last year, at

a time when there was already uncertainty due to the

countryˇŻs departure from the EU, it is no surprise that

imports fell so precipitously.

The decline in UK imports of tropical wood and wood

furniture in 2020 was concentrated in May and June when

imports fell to around 50% of the normal level. After

recovering sharply between July and October, imports fell

5% to USD100 million in November and by a further 7%

to USD89 million in December (Chart 1b).

The slowdowns in 2020 coincided with the initial COVID-

19 lockdown in Q2 2020 and a second lockdown in Q4

2020 as another more severe wave of the virus hit in the

winter months.

A concern for tropical suppliers is that timber product

imports from tropical countries suffered a

disproportionately large share of the decline. There are,

however, reasons to believe that the downturn in the UK

market last year may be only temporary and that new

opportunities for tropical suppliers will open up in the

emerging post-Brexit trading environment.

The scale of the in 2020 downturn was strongly influenced

by supply side issues. UK demand for all wood products

has proved to be more resilient than expected during the

pandemic and importers are widely reporting that the main

obstacle to trade at present is lack of availability.

The problems of shipment and rising costs of freight have

been particularly intense from South East Asia, a factor

which should ease gradually as trade flows begin to

normalise this year.

While Brexit is likely to act as a significant drag on

economic recovery in the UK, at least in the short to

medium term, there are signs that the relatively thin trade

agreement reached between the UK and the EU in the

closing days of 2020 may help level the playing field for

non-EU wood suppliers in the UK market relative to EU

competitors.

This has particular significance for hardwood products

since the UK, unlike the rest of EU, has only a very

limited domestic hardwood resource, while the broader

wood processing and furniture manufacturing industries

are also relatively small in international terms.

The country has always been very heavily dependent on

imports for wood supply and now has a strong incentive to

build stronger trade links with countries outside the EU.

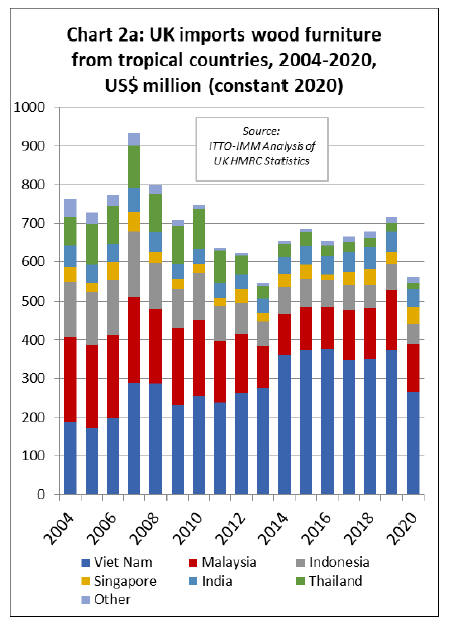

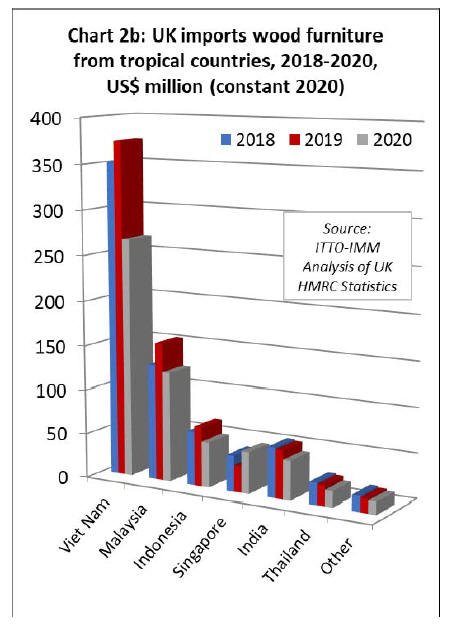

UK tropical wood furniture imports down 22% in 2020

Overall UK imports of wood furniture (HS 94) from

tropical countries in 2020 were USD562 million, 22% less

than in 2019. This was the lowest level since 2013 and

followed four years of consistent growth (Chart 2a).

UK imports from tropical countries fell much more than

imports from other countries in 2020. Total UK imports of

wood furniture fell 8% to USD 3.52 billion in 2020, with

imports from China down 7% to USD1.32 billion, down

5% from the EU to USD1.12 billion, and up 6% from

other non-tropical countries to USD458 million.

UK imports of wood furniture declined sharply from all

the leading tropical supply countries in 2020 (Chart 2b).

Imports from Vietnam were down 29% to USD267

million, imports from Malaysia fell 21% to USD123

million, imports from Indonesia declined 24% to USD51

million, imports from India fell 19% to USD44 million

and imports from Thailand were down 21% to USD18

million. In contrast, there was a 59% rise in imports from

Singapore to USD46 million.

The rise from Singapore is mainly due to logistics as large

container carriers left off the coast of Singapore during the

most stringent coronavirus measures in the second quarter

of 2020 re-entered the shipping market to help ship

containers to Europe.

Container space from other South Eastern countries was

very limited and was likely an important factor explaining

loss of share in the UK and wider European market for

wood furniture in 2020.

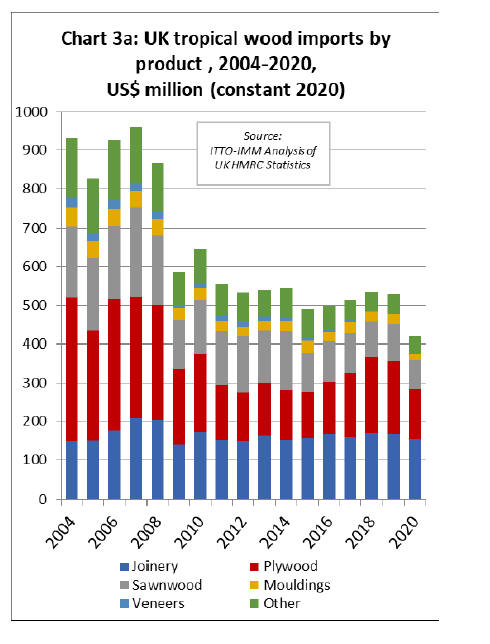

UK imports of tropical HS 44 wood products at

historically low level in 2020

UK imports of all tropical wood products in Chapter 44 of

the Harmonised System of product codes (excluding wood

for energy) declined 21% to USD417 million in 2020.

This is by far the lowest level since 2004, and probably for

many years prior to that (Chart 3a).

The downturn in imports of HS 44 wood products was

much greater from the tropics than other regions.

Total UK imports of HS 44 wood products from all

countries fell only 2% to USD5.02 billion in 2020. UK

imports from the EU actually increased 1.5% to USD3.35

billion in 2020, the gain partly explained by stock building

prior to the UKˇŻs exit from the single market on 31st

December 2020. Imports from China fell 6% to USD726

million while imports from other non-tropical countries

declined 4% to USD544 million.

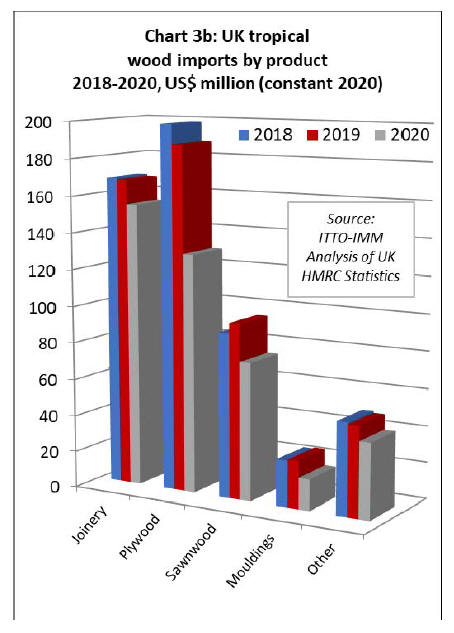

In 2020, UK import value of all the main HS 44 tropical

wood product groups declined sharply, including tropical

joinery (-8% to USD155 million), tropical plywood (-31%

to USD130 million), tropical sawnwood (-22% to USD75

million), and tropical mouldings/decking (-35% to USD17

million) (Chart 3b).

UK hardwood market conditions unprecedented

According to the latest hardwood market report in the UK

Timber Trades Journal (http://www.ttjonline.com/), the

combined effect of COVID and Brexit has been to produce

unprecedented market conditions: ˇ°Demand is reported as

good to exceptional, but the supply situation, particularly,

but not exclusively in North America, is proving

exceptionally challenging.

Prices are rising accordingly. While the sector reports

sales slumping to just 30-40% of normal levels at the

outset of the pandemic, since then, they have grown

exponentially. Some companies reported a seasonal dip in

December, others said they continued to climb and that

they hit the ground running in Januaryˇ±.

The TTJ highlights that that the surge in home

improvement is a key factor driving consumption, with

importers reporting high demand for anything to do with

construction, refurbishment and the garden and that

joinery customers are also flat out.

TTJ also notes that the hardwood supply situation is now

extremely tight as hardwood mills worldwide have

struggled to gear up production as markets emerge from

lockdown due to lack of raw material, social distancing

measures and a large proportion of personnel being in

isolation. Many mills have also been overly cautious about

increasing output, failing to forecast the huge surge in

global demand as China experienced a very rapid recovery

and the US and EU benefited from the home improvement

boom.

On tropical hardwoods, TTJ reports that while African

supply have been affected later and less than elsewhere by

the pandemic, implementation of Covid-safe work

practices has added to existing logistical problems and

very extended lead times. UK importers are saying that on

orders for kiln-dried African hardwood placed this

February, delivery is not expected before January 2022

delivery.

This highlights the extent to which UK importers are

having to rely on existing stockholdings and implies that

prices, which are already up 5% this year for sapele, the

most popular tropical hardwood species in the UK, will

continue to rise. Based on reports of very tight availability

from their suppliers in Cameroon, the Republic of the

Congo and Ghana, UK importers expect price pressure on

forward orders to increase.

One company told the TTJ that their Asian supply was

currently on hold due to ˇ®off-the-chartˇŻ freight rate

increases resulting from the disruption to shipping and

particularly container distribution caused by the pandemic.

While a container from South East Asia cost US$1500 to

US$2000 a year ago, companies now report being quoted

US$12,000-$16,000.

According to TTJ, UK importers are still generally

reluctant to try alternative hardwoods despite the huge

supply and price pressure on preferred species like white

oak and sapele.

However, a few importers report that tiama is being used

as a sapele alternative, while there is steadily increasing,

but still very restricted, demand for angelim-vermelho,

angelim-amargoso, tatajuba, jutai and araracanga from

South America and eveus (Klainedoxa gabonensis) from

Africa. Amongst temperate species, American red oak has

made some gains as the price of white oak is now 40%

higher than it was a year ago.

UK GDP unlikely to recover to pre-pandemic level until

mid-2022

The UK governmentˇŻs official estimate is that GDP

contracted 9.9% in 2020, the biggest fall of any G7

country. The latest monthly data shows that the rebound in

UK GDP stalled in the last quarter of 2020 and continued

to decline in January 2021. The latest downturn coincides

with a return to lockdown to counter a second, more

severe, wave of the virus during the winter months.

As a result GDP in January 2021 was still over 9%

percentage points down compared to a year earlier The

UK governmentˇŻs latest forecast is for the economy to

rebound 4% this year and 7.3% in 2020. This means the

economy is unlikely to return to pre-pandemic levels

before the middle of 2022.

UK construction sector and buildersˇŻ merchants report

strong growth

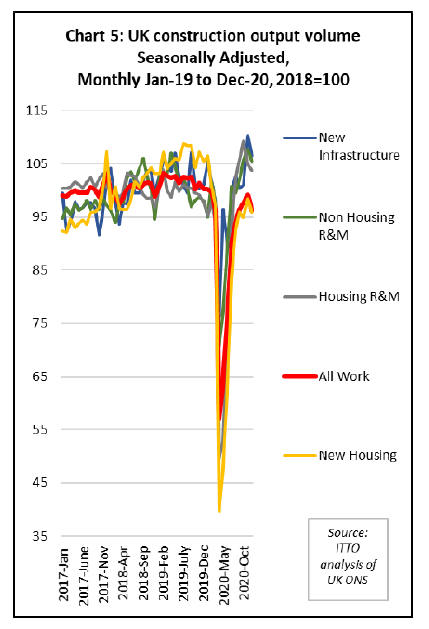

A positive factor for the UK timber trade in 2020 was that

the initial downturn in construction sector activity, which

is a key driver of timber demand, during the first ˇ°great

lockdownˇ± was short and followed by a stronger rebound

than other areas of the economy.

Although the rebound in UK construction lost momentum

in the last quarter of 2020, by the end of the year

construction activity in new infra-structure and repair and

maintenance, both for housing and non-housing, was

slightly higher than before the pandemic.

Activity in the new housing sector was only marginally

down on the pre-pandemic level (Chart 5). In January

2021, construction was the only main sector of the UK

economy to register growth, rising 0.9% compared to the

previous month.

Sales figures of UK buildersˇŻ merchants follow the general

trend in construction. The BMFˇŻs Builders Merchants

Building Index (BMBI) reported a strong performance in

the third quarter of 2020 with sales returning to near

normal levels after the first Covid lockdown greatly

reduced sales in the second quarter.

This positive overall trend continued into the fourth

quarter, with total buildersˇŻ merchantsˇŻ sales 5.4% ahead

of the same period the previous year.

For the tropical hardwood sector, it is notable that the

fourth quarter year-on-year increase in merchantˇŻs sales

was driven by strong performances in Landscaping

(+22.9%) and Timber & Joinery (+12.7%). Concerted

efforts to build timber stocks at a time when supply was

low and prices high was a key factor behind the rise in the

value of trade during the period.

Taking 2020 as a whole, UK Builders MerchantˇŻs sales

were down by -10.7% compared to 2019. Given the

publicˇŻs focus on their gardens during the first lockdown,

it is no surprise that Landscaping was the only category to

show an annual increase in sales value (+5.4%). In

contrast, sales for interior improvement were amongst the

worst performers including Kitchens & Bathrooms (-

18.1%) and Decorating (-16.5%).

BMF chief executive John Newcomb said: ˇ°Given

widespread site closures both at the start of the pandemic

and for extended Christmas shut down periods, the

continued year-on year growth seen in the final quarter of

2020 provides a positive indicator of the building

industryˇŻs recovery. No doubt the Covid effect, including

its impact on product availability, will be felt for some

time to come.

But the adaptability to enforced changes demonstrated by

merchants and their trade customers over the past 12

months gives me a cautious degree of optimism for the

coming year.ˇ±

The extent to which material supply shortages are

impacting on the UK construction sector, due both to

COVID and the UKˇŻs departure from the EU single

market on 31st December, is highlighted in recent

comments on Brexit by Rico Wojtulewicz, the head of

housing and planning policy at the National Federation of

Builder: ˇ®all materials from Europe are taking a while to

get into the UK, most with cost increases. Members are

having major issues with timber, such as MDF, veneers

and solid wood. There are very long wait times of two to

six months.ˇŻ

He added: ˇ®Another issue having a major impact is the

availability and cost of shipping containers. In some cases,

the price per container has increased six-fold, in others

there just arenˇŻt any containers available.ˇŻ

Immediate trade impact as UK leaves the EU single

market

UK trade with the EU is now governed by the EU-UK

Trade and Cooperation Agreement concluded on 24th

December 2020 just a few days before the UK was due to

leave the single market at the end of the year. The

Agreement allows for zero tariff trade between the two

partners but does not exempt UK companies from the red

tape associated with a customs border, including the need

to handle customs declarations for imports and exports.

The UK tax office has estimated that British businesses

will spend £7.5 billion a year handling customs

declarations for trade with the EU ˇŞ as much as they

would have done under a no-deal Brexit ¨C and has stated

that the number of customs forms needed to trade with the

EU under the Brexit deal ˇ°is not materially different from

a no-deal situationˇ±.

The effects on UK exports to the EU have been

immediate. A Road Haulage Association (RHA) member

survey found the volume of exports going through British

ports to the EU fell by 68% in January compared to the

same month last year, mostly as a result of problems

caused by Brexit.

While there has been a huge fall in UK exports to the EU

with the immediate introduction of EU customs controls to

UK products on 1st January, the situation in relation to UK

imports from the EU has been different.

UK imports from the EU have been affected by port

congestion and a shortage of freight capacity. However,

unlike the EU, the UK government chose a phased

approach to introduction of customs controls, postponing

the introduction of certain import procedures for EU

products.

These grace periods are designed to give businesses more

time to adapt to the new rules and ways of working.

The UKˇŻs initial intent was that requirements for

phytosanitary certification of UK imports from the EU

should be introduced from April while requirements for

full customs declarations on entering the UK market,

rather than submitting forms at a later date, should be

introduced from July.

However, on 11 March, the UK announced that these

grace periods would be extended for an extra six months

in a bid to give businesses and customs officials more time

to prepare for the additional red tape and to avoid the

threat of food shortages in the summer.

The move means the first checks on imports from the EU

into the UK will not start until October, with full border

controls not being carried out until 1 January 2022 ¨C a full

year after the UK left the EU.

These changes have significant implications for the UK

timber importing trade. In a typical year, the UK imports

around 9 million cubic metres of timber from Europe,

mostly softwoods and panel products, but including some

hardwood products, most notably oak sawnwood and birch

plywood.

Timber imported from the EU accounts for well over half

of all timber and panels consumed in the UK. In addition,

the UK imports wood furniture with a total value of

USD1.2 billion from the EU, around one third of all

imports and 15% of all consumption of wood furniture in

the UK.

Insights on the immediate effects of the UKˇŻs departure

from the EU single market on the UK timber importing

trade are provided in a TTF member survey published on

1st March. The survey draws on the views of thirty-six

respondents representing timber importers, merchants,

agents, and manufacturers.

In introducing the survey, the TTF note that, ˇ°Q1 2021 has

already brought multiple reports of haulage and freight

companies rejecting jobs and hiking prices to travel to

Britain amid long waiting times at British portsˇ±.

The survey suggests that the effects of Brexit on the UK

timber trade have been muted so far, particularly in the

hardwood sector. However, since border controls have yet

to be fully implemented, this may not be indicative of the

long term impact. The survey report finds that ˇ°Brexit red

tape has caused a mild impact on their business as customs

and due diligence mapping combined with logistical

challenges from increased border checks has slowed down

trading, but not demandˇ±.

Somewhat contradicting this conclusion, the survey report

also finds that ˇ°Members have stated they are

experiencing a dramatic slowdown in deliveries,

particularly from haulage across the English Channel from

European countriesˇ±.

Where impacts are reported, they are a very much focused

on softwoods. While 66% of respondents stated they have

had ˇ°logistics issues importing and exporting softwood

due to haulage companies charging increased rates,

rejecting their request for delivery in and out of the UK,

and a lack of truck ability due to the trade barriers

introduced by Brexitˇ±, only 33% and 0% of respondents

stated these same issues had impacted on the hardwood

trade.

Similarly, new requirements for phytosanitary certificates

on UK imports from the EU had impacted on 33% of

hardwood traders compared to 66% of softwood traders.

A significant issue for many TTF members to date has

been growing obstacles to their trade with Northern

Ireland (NI). Although NI is a part of the UK, the region

also remains in the EU single market to prevent the

creation of a hard border between NI and the Irish

Republic and thereby protect the NI peace process.

The TTF survey report notes that ˇ°while ˇ®unfettered

accessˇŻ from Great Britain to Northern Ireland had been

promised, in reality trading has become more difficult,

with a number of our members reporting they are looking

to cease trading with Northern Ireland until the trade

barriers are removedˇ±.

The TTF also notes that new requirements for UKCA

marking are starting to concern members. ˇ°While this year

members can continue placing CE-marked goods onto the

UK market, from January 2022 the UKCA mark will

become the sole UK conformance mark. This would raise

considerable trade barriers and challenges next year with

concerns businesses will not have enough time to prepare

for the implementation of the new mark.

The TTF has announced that it ˇ°will work with the

Construction Products Association (CPA) and the

Confederations of Business Industries (CBI) to advocate

for a deferment of the implementation of the mark or to

achieve equivalence with the CE Markˇ±.

EU exporters struggle to respond to UK due diligence

requests

One measure already enforced in the UK is the UK

Timber Regulation which imposes legality due diligence

requirements on all timber products placed on the UK

market, including from the EU, and which replaces the

EUTR. The TTF survey suggests that this is a "mild

barrier" to TTF members trade with the EU and Northern

Ireland.

According to the TTF, importing timber from the EU has

been made more difficult as ˇ°European companies

unwilling or unable to share details of supply chains to

help members complete the necessary due diligence has

become a growing problem.ˇ±

Furthermore, ˇ°each shipment must go through double due

diligence. Stock going into the EU undergoes due

diligence and then when it has been purchased by a UK

trader, due diligence on the same product has to be

undertaken againˇ±.

One respondent to the TTF survey stated ˇ°Due diligence

works for bulk supplies from regular customers outside the

EU. But when topping up from the EU, there could be

several supply chains involved in one shipment. Every

chain has to be risk assessed despite already being risk

assessed to enter the EU.

Suppliers do not want to risk revealing their supply chains

for smaller (but essential) occasional orders.ˇ±

Some respondents to the survey highlighted that European

suppliers do not understand why they have to prove due

diligence when the product is certified or when from a

low-risk region of the EU. TTF note that ˇ°it is hoped that

over time our membersˇŻ European suppliers will accept

the new due diligence requirements and share their supply

chain information to lessen the blocking of tradeˇ±.

In response to Brexit, Vandecasteele Houtimport, the large

Belgian hardwood importer, has created a UK registered

company to minimise post-Brexit administration and

streamline service for customers. Vandecasteele Timber

Ltd acts as operator under the UK Timber Regulation,

handling all due diligence and other customs clearance

procedures.

ˇ°We have set up the company basically to continue to

service the UK market as before,ˇ± said export manager

Genevi¨¨ve Standaert. ˇ°It ensures for UK customers that

nothing changes; all paperwork is from UK to UK, so

there are no headaches for customs clearance,

phytosanitary certificates, VAT prepayment and so on.

Due diligence, in particular, can be a lot of work and a

challenge for companies which may not have done it

before. We take that work on on the UK customerˇŻs

behalf.ˇ±

VandecasteeleˇŻs sales to the UK dropped sharply in the

first two months of the pandemic but recovered rapidly

from May. ˇ°Business has continued to grow since and

today is really good,ˇ± said Ms Standaert.

|