|

Report from

Europe

Half UK tropical timber trade value

lost in May

As expected, following the UK lockdown in response to

COVID-19 introduced on 24 March and allowing for the

long lead time in the tropical trade, there was a very sharp

decline in UK imports of tropical timber products in May.

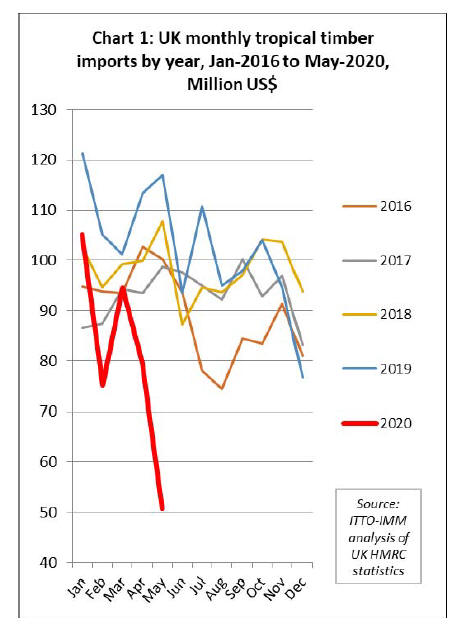

The total value of UK imports of all tropical wood (HS 44)

and wood furniture (HS 94) products during the month

was just over US$50 million, only half the value typical in

what is usually one the busiest months of the year for the

UK trade (Chart 1).

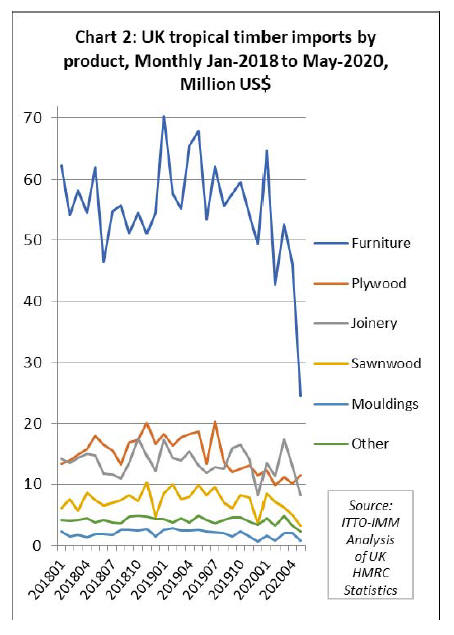

There was a large downturn in UK imports of all tropical

timber products in May. Imports of tropical wood furniture

were US$24.5 million during the month, compared to an

average of US$61.6 million for the same month in the

previous 5 years.

The same comparison for tropical plywood is US$11.5

million in May this year against the 5-year average of

US$14.3 million, for tropical joinery US$8.2 million in

May this year against the 5-year average of US$13.0

million, for tropical sawnwood US$3.3 million in May this

year against the 5-year average of US$8.3 million, and for

tropical mouldings/decking US$0.9 million in May this

year against the 5-year average of US$2.2 million (Chart

2).

The sharp downturn in May, a direct result of the

COVID-19 lockdown measures, follows a period of more

gradual decline in UK imports of tropical timber products.

UK wood furniture imports from tropical countries have

been weakening since the start of 2019 and were

particularly slow in February this year. Imports of tropical

plywood and sawnwood have also been sliding since the

middle of 2019.

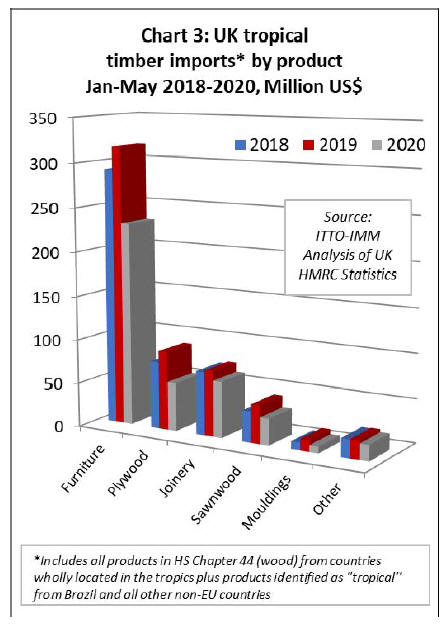

Comparing the first five months of 2020 with the same

period in 2019, total UK import value of tropical timber

products fell 27% to US$405 million.

Import value of wood furniture from tropical countries fell

27% to US$230.6 million, while imports of tropical

plywood were down 39% at US$54.9 million, tropical

joinery products were down 14% at US$63.4 million,

tropical sawnwood fell 31% to US$30.3 million, and

mouldings/decking declined 41% to US$7.7 million (Chart

3).

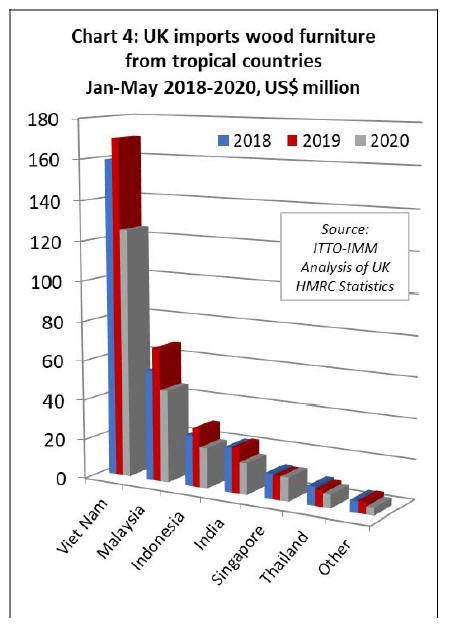

UK imports of wood furniture declined sharply from all

the leading tropical supply countries in the first five

months of this year (Chart 4). Imports from Vietnam were

down 26% at US$125.1 million, imports from Malaysia

fell 31% to US$46.5 million, imports from Indonesia

declined 31% to US$20.5 million, and imports from India

fell 31% to US$15.9 million.

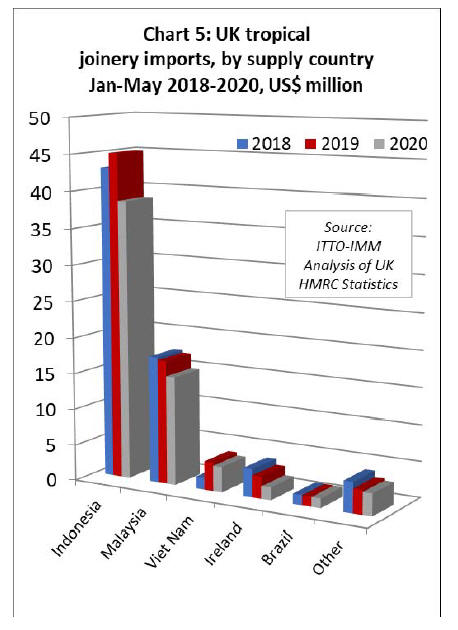

Indonesia loses ground in UK joinery market

After making gains in 2019, UK imports of tropical

joinery products from Indonesia, mainly consisting of

doors, fell 14% to US$38.6 million in the first five months

of this year. After a strong start to the year, UK imports of

joinery products from Malaysia and Vietnam (mainly

laminated products for kitchen and window applications)

stalled almost completely in May.

Total joinery imports in the first five months were down

12% to US$15.1 from Malaysia and down 11% to US$3.5

million from Vietnam. UK trade in joinery products

manufactured from tropical hardwoods in neighbouring

Ireland have also fallen dramatically this year, down 42%

to US$1.8 million in the first five months. (Chart 5).

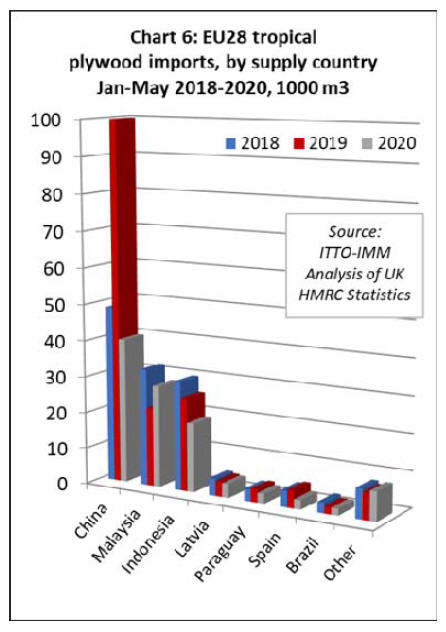

UK imports of tropical hardwood plywood from China

fall 60%

The UK imported 40,000 cu.m of tropical hardwood faced

plywood from China in the first five months of this year,

60% less than the same period last year. UK imports of

this commodity from China were at unusually high levels

in the first half of 2019 after a period of slow buying in

2018 due to Brexit uncertainty.

However, the market suffered from over-stocking in the

second half of last year as consumption slowed. This year,

UK imports have been further dampened by COVID

related supply problems in China.

Likely due to supply problems elsewhere, UK imports of

plywood from Malaysia, which have been in long term

decline, were recovering ground in the opening months of

2020. Despite significant slowing in May, imports from

Malaysia were still up 30% at 28,100 cu.m for the first

five months of the year.

However, imports from Indonesia were down 26% to

19,000 cu.m during this period, while imports from

Paraguay were 24% less at 2,700 cu.m. In recent years, the

UK has been importing small volumes of tropical

hardwood faced plywood from Latvia and Spain. In the

first five months of 2020, imports declined 8% to 3,800

cu.m from Latvia and 47% to 2,600 cu.m from Spain

(Chart 6)

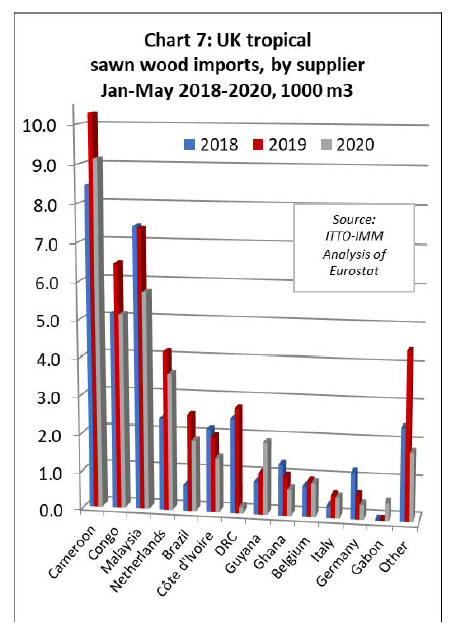

UK tropical sawn hardwood imports down 24% in year

to May

The UK is now a relatively minor market for tropical sawn

hardwood, importing less than 100,000 cu.m in each of the

last two years, making it only the fifth largest European

importer for this commodity (after Belgium, Netherlands,

France and Italy).

With the UK trade stagnating in May this year, imports

were well down from nearly all the major supply countries

by the end of the first five months. Total imports of 34,000

cu.m during this period were 24% less than the same

period in 2019.

UK tropical sawn imports are sourced from a large range

of countries, both directly in the tropics and indirectly

from other European countries (Chart 7). UK imports from

Cameroon, the leading supplier, fell 11% to 9,100 cu.m in

the five-month period, while imports from the Republic of

Congo declined 21% to 5,100 cu.m.

Of other African suppliers, imports were down 28% to

1,400 cu.m from Côte d'Ivoire, 94% to only 166 cu.m

from DRC and 33% to 704 cu.m from Ghana.

UK imports from Malaysia were 5,700 cu.m in the first

five months of 2020, 22% less than the same period in

2019.

Indirect imports into the UK via the Netherlands were

down 14%, at 3,600 cu.m, after significant growth last

year. Imports from Brazil fell 26% to 1,900 cu.m.

Of all countries supplying tropical sawnwood to the UK,

only Guyana recorded any growth in this market in the

first five months of 2020, rising 75% to 1,900 cu.m.

ˇ®Four yearsˇŻ to recover from record recession in the

UK

The key question now for the UK trade in tropical wood

products is what ˇ°shapeˇ± will the recovery take following

the sharp fall in May (likely maintained in June given the

lead times involved): will it be a ˇ°V-shaped reboundˇ±; or a

ˇ°tick markˇ± with the sharp fall followed by a longer tail of

recovery; or, worst case, an ˇ°L-shapeˇ± where trade barely

recovers and bounces along at the lower level for many

months?

This is difficult to forecast with any confidence given

continuing uncertainty over prospects for a second wave

of the virus in the UK and the long-term effects of the

lockdown and of the governmentˇŻs policy response on

jobs, consumer confidence, and business investment. That

is before factoring in other key sources of uncertainty,

such as on-going negotiations towards a post-Brexit trade

agreement with the EU, and the profound effects of the

virus on wood production in tropical countries and

competing supply regions.

The latest forecasts of growth in the UK economy are not

optimistic and imply that hopes of a V-shaped recovery

are fading. On the other hand, there are some more

positive signals from the construction sector, a more direct

driver of timber demand, and new government support

measures have potential to boost consumption.

In their latest report, the EY Item Club, a leading UK

economic forecasting body, warns that the economy may

not get back to pre-pandemic levels before 2024. The

organisation expects a record recession as the UK

economy contracts by 11.5% this year followed by a slow

rebound.

Unemployment will more than double, it says, from 3.9%

to 9%, leaving roughly three million people out of work as

the furlough scheme ends. Job losses and poor real wage

growth will lead to a collapse in consumer confidence and

hold growth back.

According to the EY Item Club report, ˇ°even though

lockdown restrictions are easing, consumer caution has

been much more pronounced than expected. Consumer

confidence is one of three key factors likely to weigh on

the UK economy over the rest of the year, alongside the

impact of rising unemployment and low levels of business

investment.ˇ±

Recent economic data in the UK has been inconsistent.

Retail sales jumped in June by 13.9%, more than expected

by most forecasters. The flash purchasing managersˇŻ index

for business activity in the UK also registered solid growth

for July.

However, these improvements come from a very low base.

DeloitteˇŻs consumer confidence tracker for the UK found

that households were emerging from the second quarter in

a slightly improved but still highly cautious mood.

Recovery in the UK manufacturing sector is also proving

to be elusive. According to the Confederation of British

Industry industrial trends survey, the manufacturing sector

remained in a deep downturn in June. Output volumes fell

at a record pace in the three months to June, exceeding the

previous record in May.

More positive, particularly for having a more direct

bearing on timber demand, is that June data pointed to a

sharp turnaround in the performance of the UK

construction sector.

The phased restart of building work on site in the UK

helped to lift output volumes and boost business

confidence in this sector. At the same time, new orders

stabilised after three months of sharp declines and

purchasing activity expanded at the fastest rate since

December 2015.

The headline seasonally adjusted IHS Markit/CIPS UK

Construction Total Activity Index jumped to 55.3 in June,

from 28.9 in May, to signal a strong increase in total

construction output. Moreover, the latest reading signalled

the steepest pace of expansion since July 2018.

Residential building was the best-performing area of UK

construction activity in June. Around 46% of respondents

to the IHS Markit/CIPS survey noted an increase in

housing activity, while only 27% experienced a reduction.

Commercial work and civil engineering activity also

returned to growth in June, although the rates of expansion

were softer than seen for house building.

The index measuring business expectations in the

construction sector for the year ahead remained

historically subdued but climbed to its highest since

February amid a boost from the reopening of work on site.

46% of the survey panel anticipate a rise in business

activity, while 31% forecast a reduction. The latter mostly

commented on concerns about the wider UK economic

outlook.

To help improve that outlook, on 8th July, the UK

government announced GBP30 billion in additional

spending measures to boost demand, retain jobs, and get

young people into employment. This was the second major

fiscal response to the COVID-19 crisis and represents a

new phase of response from the Government.

From the perspective of wood demand, probably the most

significant measure is a temporary holiday on stamp duty

for all property transactions up to a threshold of

GBP500,000. The last time such a holiday was introduced

was 2009, following the Global Financial Crisis, it did turn

out to be an effective measure for boosting transactions in

the housing market. The benefit of transactions in this

market is that they tend to be paired with other forms of

activity, including in sectors, like furniture, particularly

relevant to wood product suppliers in tropical countries.

According to UK government figures, there were 48,450

UK residential property transactions in May 2020, which,

while 16.0% higher than April 2020, was still 49.6% lower

than May 2019, and 6.2% lower than at the lowest point in

the financial crisis, which was January 2009. It is hoped

the stamp duty holiday will lead to a more significant

increase in transactions in August and September.

Also included in the governmentˇŻs announcement was

GBP1 billion in funding to improve public buildings and

GBP2 billion of Green Home Grants, with grants of up to

GBP10,000 for each household towards retrofitting

properties to be energy efficient. This should help boost

demand and activity in the UK joinery sector.

The UK and EU ˇ°still some way off reaching

agreementˇ± on Brexit deal

Following negotiations in London in the week ending 24

July, the UK and EU have said they still remain some way

off reaching a post-Brexit trade agreement. This was the

second official negotiation round to be held in person

since the coronavirus crisis, after both sides agreed to

"intensify" talks in June.

EU chief negotiator Michel Barnier said a deal looked "at

this point unlikely" given the UK position on fishing rights

and post-Brexit competition rules. The EU is demanding

that the UK tie itself closely to the blocˇŻs state aid, labour

and environmental standards to ensure it does not undercut

the EUˇŻs single market with poor-quality goods.

Mr. Barnier said there was a risk of no deal being reached

unless the UK changed course on these topics, which were

"at the heart" of the EU's trade interests. He added that an

agreement would be needed by October "at the latest" so it

could be ratified before the current post-Brexit transition

period ends in December.

His UK counterpart David Frost said "considerable gaps"

remained in these areas, but a deal was still possible. The

UK has ruled out extending the December deadline to

reach a deal. The two sides' chief negotiators are meeting

again informally in London in the last week of July, with

another round of official talks scheduled for mid-August

in Brussels.

In his regular weekly blog on 27 July, under the heading

ˇ°Any deal is better than no dealˇ±, the CEO of the UK

Timber Trade Federation David Hopkins called on

members to put more pressure on the Government to

ensure a deal with the EU is secured.

Mr. Hopkins highlighted the ˇ°increased bureaucracy,

increased costs, and increased time to move goods across

bordersˇ± seen in the UK governmentˇŻs new publication for

the Border Operating Model.

https://www.gov.uk/government/publications/the-borderoperating-model).

He was also critical of the new UK Global Tariff regime.

ˇ°On the face of it, this is a positive document for trading

with the rest of the world, with the stated intention to

lower the tariffs currently in existence and simplify the

frameworkˇ±.

ˇ°Howeverˇ±, says Mr. Hopkins, ˇ°in the event of a no deal

exit it will have exactly the opposite effect on imports from

Europe, our main trading partner, imposing duty on many

products that have been duty free within the single

marketˇ±.

Mr Hopkins identified the following ˇ°obvious problems

for the wood sectorˇ± created by the new tariff regime:

ˇ°First, the UK Global Tariff introduces tariffs on imports

of European plywood and laminated timber products of

between 6 and 10%. This will reduce the competitiveness

of these products in the market ¨C possibly pushing buyers

towards competing non-timber alternatives or products

from outside Europe with lower transparency and worse

track record on performance.

ˇ°Secondly, it seems to provide a disincentive to

manufacturing certain products and adding value within

UK borders. For example, manufacturing of certain

joinery items such as door sets, windows or I-beams, can

use laminated sections as components or feedstock. These

components could now face tariffs of up to 10% adding

costs to the manufacturing process.

ˇ°However, paradoxically, importing fully manufactured

items of joinery or I-beams will attract considerably lower

tariffs of zero to two per cent. Under this scenario, what

would be the point of maintaining manufacturing in the

UK ¨C with the associated costs of machinery, trained

skilled staff and so on ¨C when one could simply import the

products from abroad?ˇ±.

Mr. Hopkins concludes, ˇ°Of course, it may not come to

this. The scenario described above could easily be solved

by negotiating and agreeing a comprehensive free trade

deal with the EU, thus eliminating the need for tariffsˇ±.

|