|

Report from

Europe

EU wood manufacturing struggles with slow

growth

and substitutes

The EU wood joinery sector continued to grow only very

slowly in 2018, well below the pace of increase in the

wider construction sector. While joinery production and

consumption gained momentum in Germany, Austria,

Spain, the Netherlands and Belgium last year, it remained

subdued in Italy, the UK, France and Scandinavia.

Growth in the EU wood door sector slowed in 2018, while

the wood window sector was close to a new record low.

There was some evidence of wood making up some lost

ground against plastics in these sectors, but wood

continues to face stiff opposition from other materials.

Where wood is being used, it is increasingly combined

with metals, or used in engineered form, to ensure greater

strength and durability.

These are the main conclusions to be drawn from analysis

of newly released Eurostat PRODCOM data which

provides a snapshot of the production and consumption

value of wood joinery products in the EU in 2018.

EU joinery production not keeping pace with

construction sector growth

The independent research agency Euroconstruct estimates

that the value of construction activity in the EU increased

3.1% in 2018, building on 3.1% growth the previous year.

However, analysis of newly released Eurostat data

indicates that activity in the European wood joinery sector

has been relatively unresponsive to this wider expansion in

the building sector.

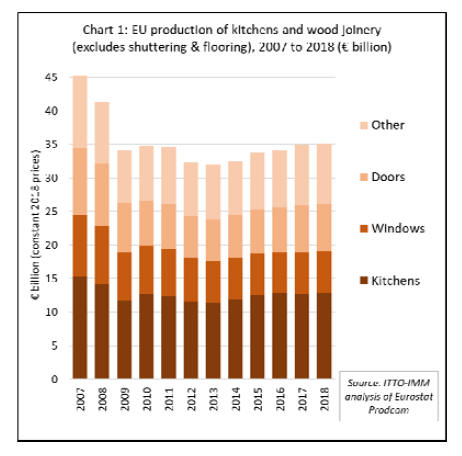

Eurostat PRODCOM data shows that the production value

of wood joinery and related products in the EU increased

only 0.3% to €35.1 billion in 2018 following growth of

2.4% in 2017. Although 2018 marked a high point for EU

joinery sector activity in the last 10 years, activity was still

down more than 20% compared to the period before the

global financial crises (Chart 1 left).

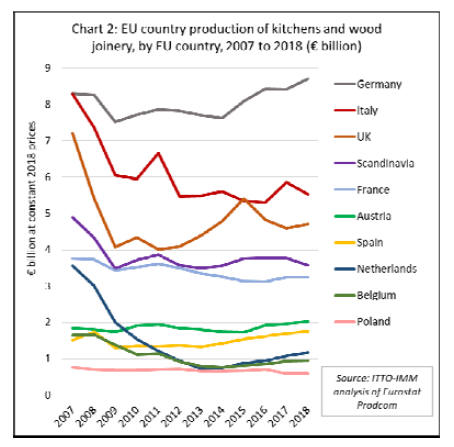

The trend in wood joinery activity has varied widely

between EU countries in recent years (Chart 2). After

levelling off in 2017, growth in joinery activity in

Germany resumed last year, rising at 3.3% to €8.70. After

a brief bounce in 2017, joinery production in Italy fell

back 6% to €5.52 billion in 2018, only just above the

historically very low levels recorded in 2015 and 2016.

In the UK, joinery production increased 2.6% to €4.71

million after slowing over 5% the previous year. Joinery

production declined in Scandinavia, by 5.6% to €3.57

billion in 2018. Joinery production in France increased

only 0.3% in 2018, to €3.25 billion, after rising 3.7% the

previous year.

However, there has been more consistent growth in joinery

production in several other EU markets including Austria

rising 3.3% to €2.03 billion in 2018 (+2.2% in 2017),

Spain rising 3.6% in 2018 to €1.75 billion (+4.6% in

2017), the Netherlands rising 8.5% in 2018 to €1.17

billion (+11.7% in 2017), and Belgium rising 1.5% in

2018 to €0.95 billion (+8.8% in 2017).

Part of the explanation for the slow increase in wood

joinery activity in the EU compared to growth in the wider

construction sector and economy is increased substitution

by alternative materials. However, there is some evidence

to suggest that the pace of substitution slowed in 2017 and

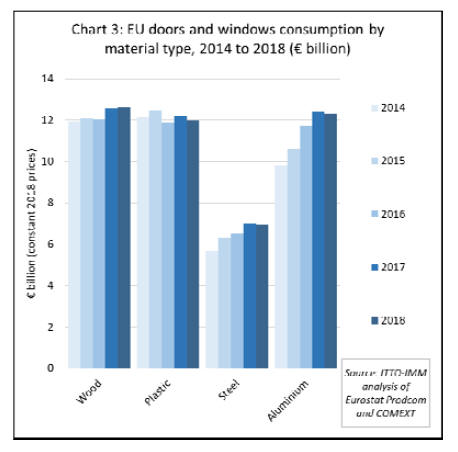

2018. This is revealed by comparing the total EU apparent

consumption value of doors and windows in various

materials (Chart 3).

Between 2014 and 2017 total EU consumption value for

doors and windows increased 26% in aluminium and 28%

in steel. The consumption value for wood increased only

4% during this period, while consumption of plastic

stagnated.

Overall the share of wood in the total value of EU door

and window consumption fell from 30% to 28% between

2014 and 2017, while the share of aluminium increased

from 25% to 28%, steel increased from 14% to 16%, and

plastic decreased from 31% to 27%.

During this period, the growth in aluminium consumption

in the EU windows and doors sector was particularly

dramatic. Aluminium has always remained the default

windows product in the commercial market but has

enjoyed considerable resurgence within the residential

window and door market.

An important driver behind this has been aluminium bifold

and sliding doors as consumers demand greater space

and light within living areas. Another factor is the demand

for lower maintenance and greater strength in light weight

frames for high energy efficiency double and triple glazed

units.

However, in 2018, the growth in consumption of steel and

aluminium appears to have stalled. Wood even regained a

little share, rising from 28% to 29%, at the expense of

plastic for which share fell from 28% to 27%.

The Eurostat data has limitations and the suggestion that

wood may be regaining some market share is contradicted,

at least in the window sector, by other more detailed

studies (see report below on the Interconnection study).

A specific constraint of the PRODCOM data is that it does

not distinguish products made wholly in wood or metals

from those that are composites of both materials. The

development of wood-aluminium composite window

frames has been a key growth area in the EU in recent

years. These products combine the strength and efficiency

of aluminium with the thermal insulation and aesthetic

properties of wood.

Stasis in EU market for wooden doors

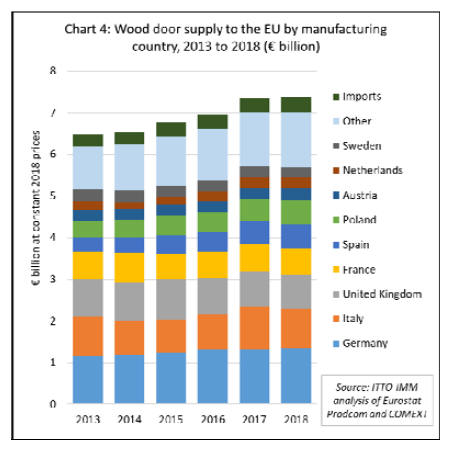

Eurostat PRODCOM data shows that the total value of

wood doors supplied to the EU increased just 0.1% to

€7.36 billion in 2018. Most new wood door installations in

the EU comprise domestically manufactured products. The

EUˇŻs domestic production was static at €7.0 billion in

2018 (Chart 4).

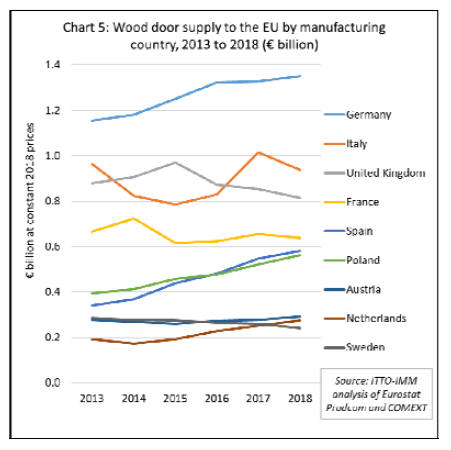

There was significant variation in the performance of the

wood door sector in EU countries in 2018. Production in

Germany, the largest wood door manufacturing country,

increased 1.9% to €1.35 billion during the year.

Production in the UK fell back a further 4.5% to €810

million in 2018 after declining 2% the previous year, the

volatility being partly due to Brexit and partly to changes

in the EUR-GBP exchange rate.

Door production in Italy has also been volatile, declining

7.5% to €940 million in 2018 after a 22% increase the

previous year. Production in France fell 2.5% to €640

million after a 5% rise in 2017. Production in Sweden fell

nearly 8% to €240 million.

Elsewhere there were solid gains during 2018, with door

production rising 6% to €580 million in Spain, 7.4% to

€560 million in Poland, 5% to €290 million in Austria and

9% to €280 million in the Netherlands (Chart 5 above).

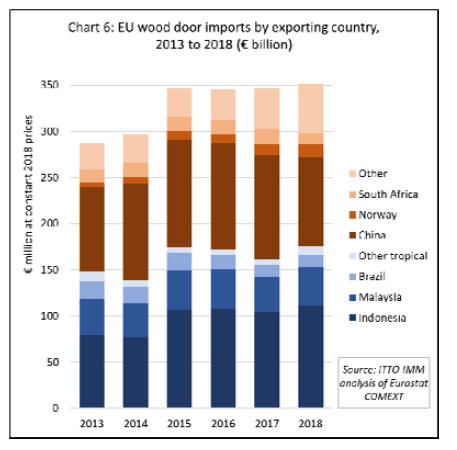

Wood door imports into the EU increased by 1.5% to €352

million in 2018 (Chart 6). Imports accounted for 4.8% of

the total euro value of wood door supply to the EU in

2018, the same proportion as the previous year.

Tropical countries took a larger share of the EU market for

wooden doors in 2018, largely at the expense of China.

Total EU imports from the tropics were €175 million in

2018, 8.6% up on the previous year and enough to offset a

6% decline in 2017.

In 2018, wooden door imports from Indonesia increased

7.8% to €112 million, while imports from Malaysia were

up 7.1% to €41 million. Imports from Brazil increased

1.7% to €13 million. EU imports of wooden doors from

China, still the largest single external supplier, fell 2% to

€111 million in 2017.

The European wood door industry is now dominated by

products manufactured using engineered timber driven by

requirements to comply with higher energy efficiency

standards and efforts to provide customers with more

stable products and long-life time guarantees.

Another key trend is towards composite doors with a steelreinforced

uPVC outer frame with an inner frame

combining hardwood and other insulation material. These

new products are designed to combine strength, security,

durability, high energy efficiency, with a strong aesthetic.

There may be a place for tropical hardwoods in the design

of these products with manufacturers looking to combine

high quality, consistent performance, regular availability,

and good environmental credentials with a competitive

price.

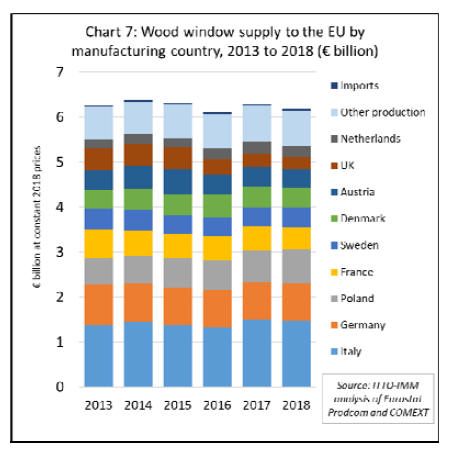

EU market for wood windows fell 1.6% in 2018

The total value of wood windows supplied to the EU fell

1.6% to €6.18 billion in 2018 following a 2.8% increase

the previous year (Chart 6). EU consumption of wood

windows in 2018 was €6.14 billion, the second lowest

level recorded in the last twenty years (when adjusted for

inflation), only just exceeding the record low of €6.07 in

2016.

Supply of wood windows to the EU is overwhelmingly

dominated by domestic production which fell 1.7% to

€6.14 billion in 2018. Imports from outside the EU

accounted for only 0.6% of total EU wood window supply

in 2018, a slight gain compared to 0.6% in 2017.

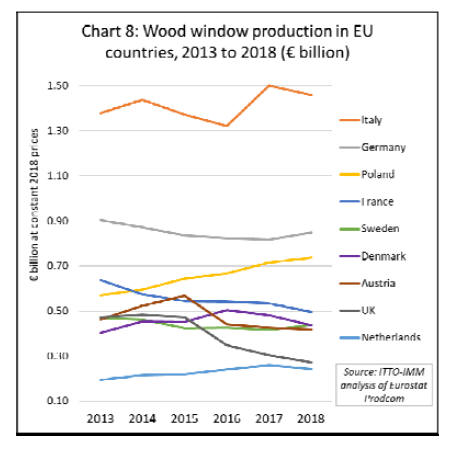

Italy has maintained its position as the largest wood

window manufacturer in the EU, although production fell

2.7% to €1.46 billion in 2018. Production in Germany

increased 4% in 2018, to €850 billion, rebounding after a

0.9% decline the previous year. Production in Sweden also

rebounded in 2018, up 5.4% to €440 million, after

declining 2.4% the previous year. Production in Poland

continued to rise in 2018, by 2.9% to €740 billion.

However, wood window production declined in most other

leading EU producer countries in 2018 including France (-

7.2% to €500 million), Denmark (-9.2% to €440 million),

Austria (-2.2% to €420 million), UK (-10.8% to €270

million), and the Netherlands (-5.9% to €240 million)

(Chart 7).

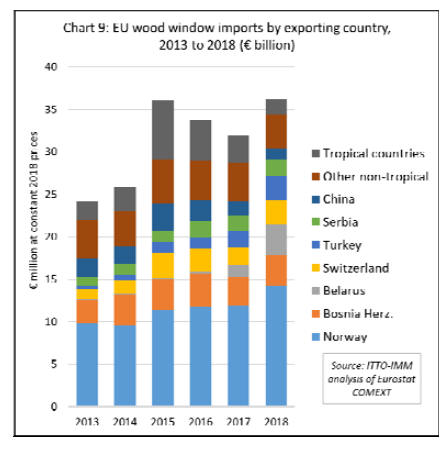

EU imports of wood windows from outside the EU

increased by 13.1% in 2018 to €36 million, recovering

ground lost in the previous two years (Chart 9). Imports

increased 19% to €14 million from Norway, 8% to €4

million from Bosnia Herzegovina, and 154% from

Belarus, to €4 million.

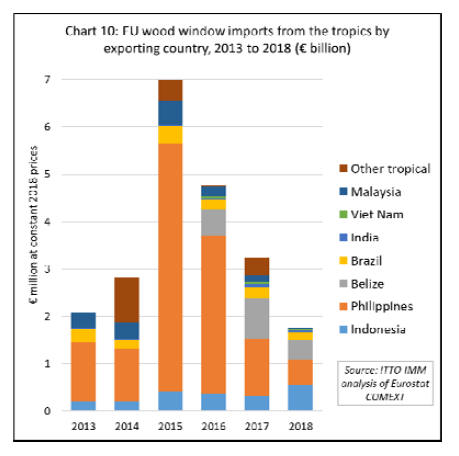

Only a very limited, and currently declining, quantity of

wood windows is imported into the EU from tropical

countries. After a spike in imports of €7 million in 2015,

mainly from the Philippines, imports from tropical

countries fell continuously to only at €1.8 million in 2018

(Chart 10). Most EU wood window imports from tropical

countries are destined for France and Belgium.

Tropical wood in the European wood window market

While tropical countries are not significantly engaged in

the EU market for finished windows, this sector is of

interest as a source of demand for tropical wood material.

From this perspective, a notable trend in the EU window

sector ¨C as in the door sector - is towards use of

engineered wood in place of solid timber.

This is particularly true of larger manufacturers producing

fully-factory finished units that buy engineered timber by

the container load.

Increased use of engineered wood is closely associated

with efforts by window manufacturers to meet rising

technical and environmental standards, provide customers

with long lifetime performance guarantees and recover

market share from other materials.

Increased focus on energy efficiency means that tripleglazed

insulating window units with very low U-factors

are now more common than double-glazed units in

Europe. These units demand thicker, more stable and

durable profiles that in practice can only be delivered at

scale using engineered wood products or by combining

wood with aluminium and steel in composite products.

The quality and engineering of wood windows has

undergone a revolution in the EU in recent years so that

manufacturers are now able to deliver products with many

of the benefits previously reserved only for the best quality

tropical hardwood frames using softwoods and temperate

hardwoods.

Factory-finished timber windows are given a specialist

spray-coated paint finish for even and durable coverage

which might only need redoing once a decade. The

lifespan of factory-finished engineered softwood frames is

now claimed to be about 60 years, while thermally or

chemically modified temperate woods can achieve around

80 years.

Nevertheless, smaller independent joiners producing

bespoke products in low volumes still tend to rely on solid

timber purchased from importers and merchants to

manufacture window frames. Tropical woods such as

meranti, sapele and iroko continue to supply a high-end

niche in this market sector, competing directly and often

successfully with oak, Siberian larch, and western red

cedar.

Total window sales increase 2% in Western Europe

2018

Sales in the window market in Western Europe increased

by 2.0% in terms of value last year. Sales in the industry

increased by 1.5% in terms of quantity. A similar

development is expected for 2019, as shown by

Interconnection Consulting in a study presented at the

First Vienna Window Congress in June 2019.

The great uncertainty surrounding Brexit caused a 2.1%

sales decrease in the window industry in the UK and

Ireland area. By contrast, the window market in southern

Europe (Italy, Spain, Portugal) will continue to recover

and will be EuropeˇŻs main growth area with sales expected

to increase 6.8% in 2019.

The largest markets, France and Benelux and the Germanspeaking

DACH region, however, will continue to achieve

moderate growth rates of 1.6% and 1.9% in 2019,

respectively. In these countries, the main factor curbing

growth is restrained housing construction.

The Scandinavian countries are also suffering from the

poor development of residential construction and the

window market is this region is expected to decline 1.5%

in 2019 with a particularly large slowdown in Sweden.

Overall, Interconnection estimate that sales of windows in

western Europe will increase from €18.4 billion in 2018 to

€19.9 billion by 2022, with Italy, Spain and Portugal

making a major contribution to growth both in the new

construction sector and in the renovation segment.

Wood-metal composite windows gain ground in

western Europe

According to Interconnection, western European sales of

windows with wood content should hit €5.38 billion in

2019, including €2.62 billion of wood-only products and

€2.86 billion of wood-metal composite products. Window

market share of wood-only products currently stands at

14.0% while the share of wood-metal composites stands at

15.3%.

Sales of wood-only windows in western Europe are

forecast to decline 1.2% per year between 2018 and 2022.

However, this decline is expected to be offset by 2.6%

annual growth in sales of wood-metal composite windows.

In 2019, metal windows have the largest share of the

western European window market, with 36.8%. Sales of

metal windows in this market are forecast to reach €6.8

billion this year and annual growth of 3.2% is expected

until 2022.

Consistently high growth rates for this material are

expected due to relatively low costs of maintenance and

the optical appeal of aluminium.

PVC currently accounts for €5.40 billion (29.4%) of

window sales in the western European market. PVC

window sales are expected to grow by 1.7% per annum

until 2022, mainly driven by rising demand in southern

Europe.

An additional €680 million (3.7%) of window sales

comprise PVC-aluminium composite product. Sales of this

product are expected to increase 3.7% annually until 2022.

Environmental requirements drive window demand for

renovation

Interconnection report that the residential construction

sector is the most important market for windows in

western Europe, accounting for 66.3% of sales. Total sales

in this sector are expected to grow 1.4% per year until

2022 with most of the increase driven by renovation which

continues to perform well due to increased environmental

requirements.

The European window industry is undergoing a major

structural change due to increased internationalization.

Companies from Eastern Europe, particularly in Poland,

Slovakia and Romania, are gradually increasing share of

western European markets. Nearly 30% of windows

installed in Germany each year are manufactured outside

the country. Exports account for 56% of sales by Polish

windows manufacturers.

PVC dominant window type in Eastern Europe

According to Interconnection Consulting, PVC is the

leading material used for window frames in Eastern

Europe, with annual sales of €2.48 billion expected to

grow at 3% per year until 2022. Metal windows are the

second most popular window type with annual sales of

€1.03 billion euros growing annually at a rate of 5.2%.

Metals are particularly dominant in the non-residential

construction sector. There is also expected to be rapid

growth in sales of wood-aluminium windows in Eastern

Europe, at an annual rate of 7.6% until 2022.

|