|

Report from

Europe

EU tropical wood trade strong in the first

quarter of

2019

The EUˇŻs trade in tropical wood products was more

buoyant in the first quarter this year compared to the same

period in 2018.

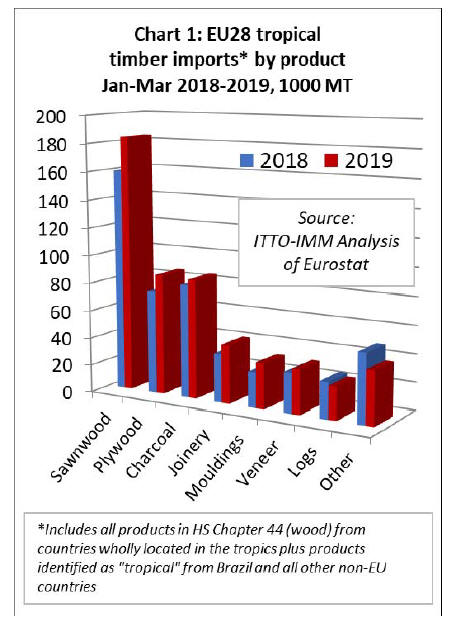

Total imports of all wood products (classified in HS

Chapter 44) from tropical countries in the first quarter of

2019 were 525,000 MT, 9% more than the same period in

2018. Import value increased 17% to €561 million.

This is surprising given that the wider economic situation

in the EU is not particularly promising this year, the

European Commission having recently downgraded GDP

growth projections to only 1.4% for the whole of the EU

in 2019 in response to signs of deteriorating economic

conditions.

To some extent the rise in EU tropical wood imports so far

in 2019 is only a reflection of just how poor the market

was last year when imports for several commodities barely

exceeded the record lows of the 2008-2009 financial

crises. Nevertheless, it is encouraging that the rise in EU

imports so far this year has been consistent across nearly

all tropical wood product groups (Chart 1).

The latest upturn in imports is also quite well distributed

across the EU with imports of tropical wood products

higher during the first quarter in all the leading EU

markets except Germany.

In the first quarter of 2019 compared to the same period in

2018, total imports of tropical wood products increased in

Belgium (+5% to 102,500 MT), the UK (+23% to 91,000

MT), Netherlands (+16% to 72,000 MT), France (+4% to

60,000 MT), Italy (+13% to 44000 MT), Spain (+36% to

26,600 MT), Portugal (+70% to 19,400 MT) and Greece

(+23% to 18,700 MT).

In contrast, total imports of tropical wood products in

Germany declined 9% to 42,400 MT in the first quarter of

2019. This decline is partly driven by increasing reliance

on indirect imports of tropical wood products from other

EU countries by German distributors.

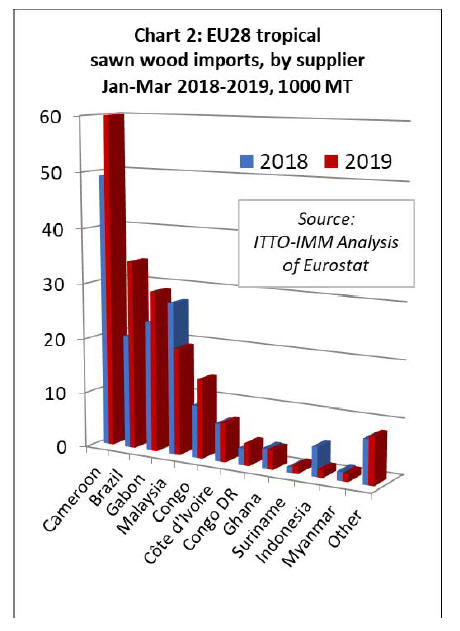

15% rise in EU imports of tropical sawn wood

EU imports of tropical sawn wood increased 15% to

184,000 MT in the first quarter of 2019 compared to the

same period in 2018. Import value increased 12% to €181

million.

Imports from Cameroon, particularly slow in the first

quarter of last year, increased 22% to 60,000 MT in the

same period this year. Imports also increased sharply from

several other countries including Brazil (up 66% to 34,000

MT), Gabon (up 23% to 29,000 MT), Congo (up 52% to

14,200 MT), and DRC (up 32% to 4,000 MT).

Imports increased slightly, by 4%, to 7100 MT from Cote

dˇŻIvoire. These gains offset a 30% decline in imports from

Malaysia, to 19,400 MT. (Chart 2).

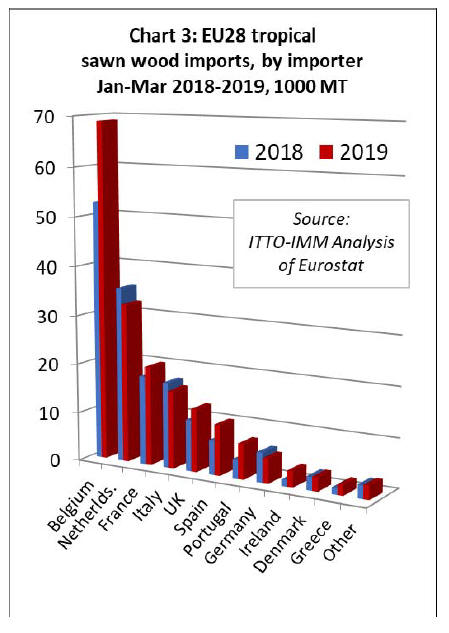

The trend towards increased concentration of tropical

sawn wood imports into the EU by way of Belgium has

continued this year. In the first quarter of 2019 compared

to the same period in 2018, imports into Belgium

increased 31% to 69,000 MT.

Imports also increased in France (up 12% to 20,100 MT),

the UK (up 23% to 12,900 MT), Spain (up 47% to 10,370

MT) and Portugal (+85% to 7,200 MT). However, imports

fell 9% to 32,500 MT in Netherlands and were down 8%

to 15,900 MT in Italy. (Chart 3).

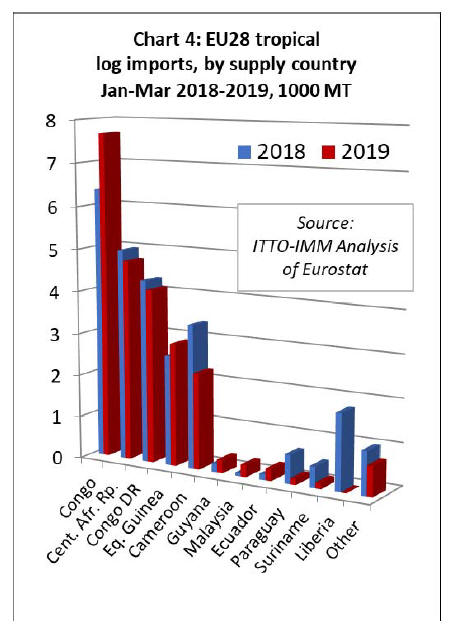

Slowdown in EU imports of tropical logs

After recovering a little ground in 2018, EU imports of

tropical logs slowed again in the first quarter of 2019.

Imports of 23,500 MT during the first quarter of the year

were 10% less than the same period in 2018. Import value

fell 16% to €11.2 million during the period.

While EU imports of tropical logs increased by 20% to

7,680 MT from Congo, the leading supplier, this was

offset by falling imports from the Central African

Republic (-5% to 4,730 MT), DRC (-5% to 4,100 MT) and

Cameroon (-33% to 2,260 MT).

There were also zero EU imports of tropical logs from

Liberia during the first quarter of 2019 compared to 1790

MT in the same period last year. (Chart 4 above).

All three of the leading EU markets for tropical logs

declined in the first quarter of 2019 compared to the same

period last year; imports fell 7% to 11,200 MT in France,

26% to 4,360 MT in Belgium, and 10% to 3,450 MT in

Portugal.

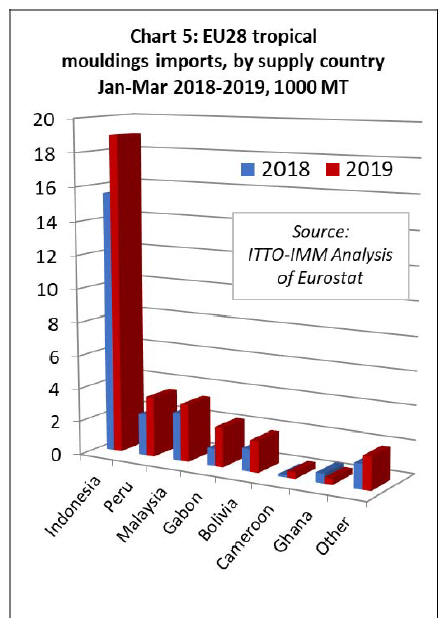

Sharp rise in EU tropical moulding imports

EU imports of tropical mouldings (which includes both

interior mouldings and exterior decking products)

increased sharply, by 30%, to 32,900 MT in the first

quarter of 2019. Import value increased 46% to €54

million.

EU imports of tropical mouldings increased from all the

leading suppliers of this commodity in the first quarter of

2019 including Indonesia (+22% to 19,000 MT), Peru

(+45% to 3,600 MT), Malaysia (+21% to 3,400 MT),

Gabon (+124% to 2,300 MT) and Bolivia (+40% to 1,900

MT) (Chart 5).

In the first quarter of 2019, imports of tropical mouldings

increased in all the leading EU markets including

Germany (+33% to 9,500 MT), Netherlands (+30% to

7,400 MT), France (+58% to 5,100 MT), Belgium (+11%

to 4,600 MT), and the UK (+49% to 3,500 MT).

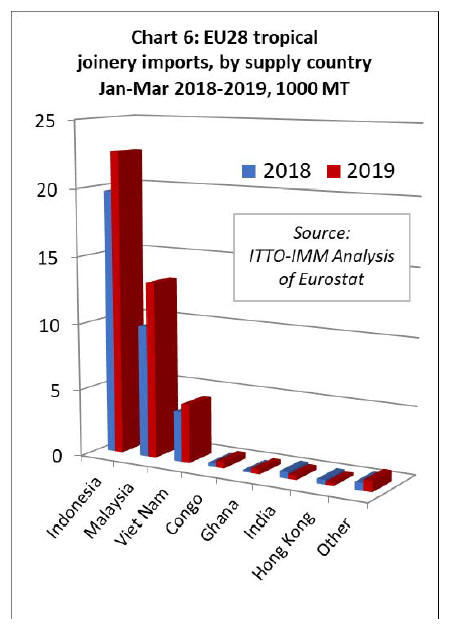

Tropical Asian suppliers make gains in EU joinery

market

EU imports of tropical joinery products, mainly doors

(from Indonesia), and laminated window scantlings and

kitchen tops (from all leading tropical suppliers), increased

21% to 42,300 MT in the first quarter of 2019. Import

value increased 26% to €87.2 million.

EU imports of tropical mouldings increased in the first

quarter of 2019 from all three of the countries that

dominate international trade in tropical joinery products

including Indonesia (+15% to 22,600 MT), Malaysia

(+33% to 13,100 MT), and Viet Nam (+17% to 4,300 MT)

(Chart 6).

In the first quarter of 2019, imports of tropical joinery

products increased by 13% to 17,400 in the UK and by

115% to 12,300 MT in the Netherlands. These gains offset

a 10% fall in imports in Belgium to 4,200 MT, a 33% fall

in France to 2,500 MT, and a 14% fall in Germany to 2250

MT.

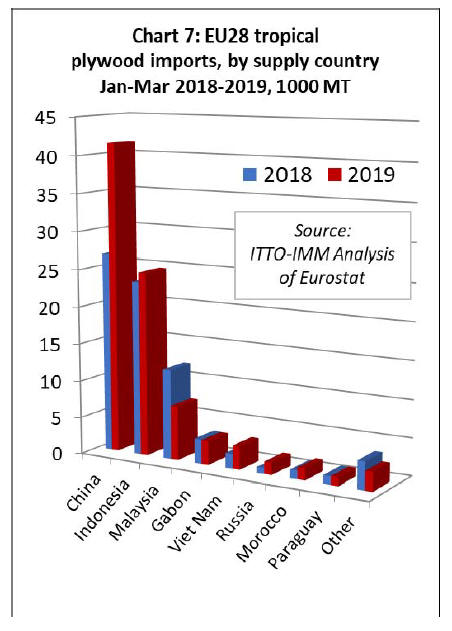

EU imports of tropical plywood made in China

continue to increase

EU imports of tropical plywood products increased 17% to

86,600 MT in the first quarter of 2019 compared to the

same period last year. Import value increased 24% to

€76.6 million.

A large and growing proportion of the plywood faced with

tropical hardwood imported into the EU is manufactured

in China. The EU imported 41,400 MT of this product

from China in the first quarter of 2019, 55% more than

during the same period in 2018.

Imports also increased from Indonesia, by 6% to 24,700

MT, and from Viet Nam, by 60% to 3,100 MT. These

gains offset a 40% fall in imports from Malaysia, to 7,300

MT (Chart 7).

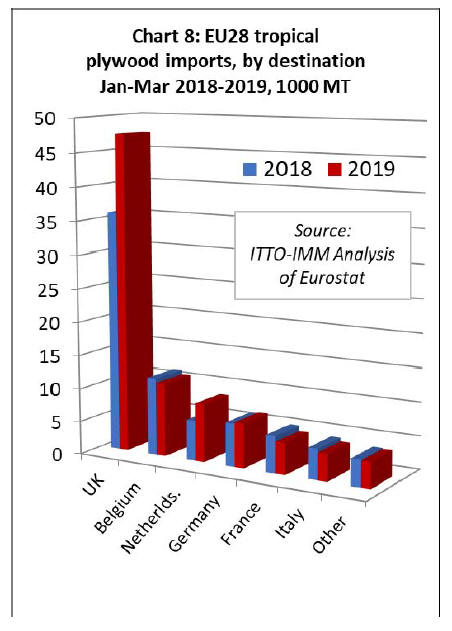

In the first quarter of 2019, imports of tropical plywood

products increased 32% to 47,500 in the UK, by 45% to

8,700 MT in the Netherlands, and by 3% to 6,700 MT in

Germany. These gains offset a 5% fall in imports in

Belgium to 11,000 MT, a 14% fall in France to 4,750 MT,

and a 12% fall in Italy to 4,050 MT. (Chart 8).

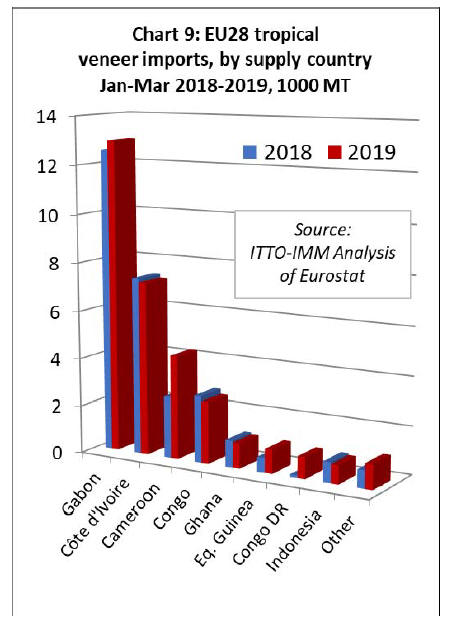

EU imports of tropical veneer up 11%

EU imports of tropical veneer increased 11% to 31,800

MT in the first quarter of 2019 compared to the same

period last year. Import value increased 13% to €42.6

million.

The EU imported 12,970 MT of veneer from Gabon in the

first quarter of 2019, 3% more than during the same period

in 2018. Imports from Cameroon rose sharply, by 68% to

4,300 MT, after a poor year in 2018.

There was also a significant increase in imports from two

smaller African suppliers of this commodity, Equatorial

Guinea (+61% to 1000 MT) and DRC (+700% to 900

MT). Meanwhile imports from several long-term veneer

suppliers to the EU lost ground, including Cote dˇŻIvoire (-

2% to 7,200 MT), Congo (-8% to 2,560 MT), and Ghana

(-6% to 1,050 MT). (Chart 9).

In the first quarter of 2019, tropical veneer imports

increased by 10% in France, to 11,600 MT, by 22% in

Italy, to 8,100 MT, and by 120% in Greece to 2,500 MT.

However, imports fell slightly, by 4%, to 4,550 MT in

Spain.

Benefits to UK merchants of stocking wide range of

hardwoods

The first edition of the UK Timber Trade FederationˇŻs

Merchant News (https://ttf.co.uk/latest/merchant-news/)

includes an article focusing on the challenges and

opportunities in the UK hardwood trade.

The article seeks to answer the question ˇ°Are merchants

missing out on business by not making available a

selection of sustainably-grown hardwoods from around the

worldˇ±?

The article highlights how the market for hardwoods in the

UK is constrained by the costs to merchants of holding a

diverse range of expensive stock as well as by lack of

knowledge of end-users of the wide range of species

available.

The article quotes John Dowd, Specialised Product

Category Director at International Timber,one of the UKˇŻs

largest hardwood importers: ˇ°For many merchants the

main difficulty is not having sufficient space to carry the

ideal inventory: boards may not be the right width or

length for bespoke joinery work, for example.

The main hardwood species we find demand for are

American white oak, sapele, meranti, European oak,

beech, and, for decking, bangkirai. One or two merchants

succeed by keeping a small stock of hardwoods on the

ground in-branch, but sawn hardwood lumber can be

expensive to stockˇ°.

Commenting on the main hardwood species available to

UK buyers and their respective uses, Chris Bowen-Davies,

Key Accounts Manager at Brooks Bros Timber, notes that:

ˇ°In terms of African hardwoods, sapele is our largest

seller. ItˇŻs a good all-rounder for external and internal use,

with reasonable density and good machining capabilities.

ItˇŻs good for paint application too. Utile is still favoured

as it tends to be more stable than many external

hardwoods.

ˇ°Iroko is classed as Very Durable and lasts well in outdoor

situations. It can be used for example as cill sections or

for other outdoor joinery. It can also be used in boatbuilding

and garden furniture, as well as for marine work,ˇ±

BrooksˇŻ Chris Bowen-Davies says. ˇ°idigbo is another

durable material, but it needs a primer coat before any top

paint coat is applied. Its availability from legal and

sustainable sources can be somewhat erratic.

Travelling further round the globe, meranti, which comes

from Se Asia, is a very popular joinery hardwood used in

window and door manufacturing. It paints satisfactorily

but its density can vary considerably.ˇ±

The article notes that UK merchants are seeing a sales

benefit from stocking the more familiar types of

hardwood, in defined ranges to suit particular market

segments, as Business Development Director at buildersˇŻ

merchants MGM Timber, relates: ˇ°We stock a range of

hardwood mouldings in our branches.

European oak mouldings match the current fashion for

Oak flooring, joinery and kitchens. We also stock meranti

mouldings for the replacement market, including skirtings,

architraves and window cill sections.

ˇ°The market for hardwood mouldings is very wideranging,

from the enthusiastic DIYer to builders and

joiners involved in RMI, window fitters and even

housebuilders.

Local housebuilders want to increase the value of the

homes they build by providing a high quality finish, which

is where hardwood mouldings come in,ˇ± Grant Wilson

says.

Grant Wilson also notes that ˇ°ensuring sustainable

sourcing is of primary importance on hardwoodsˇ±, and this

is a theme also highlighted by TTF Managing Director

David Hopkins. Hopkins particularly emphasises the role

of the FLEGT VPA process which is seen as having strong

market development potential in the UK.

According to Hopkins, ˇ°FLEGT licensing is a mechanism

for ensuring the legality of harvesting and supply at

country-level, whereas the two main certification schemes

license at individual forest and producer level.

Merchants should watch the FLEGT space as a number of

African countries are going through the licensing process,

which will eventually make more species available for

purchase under EUTR rules.ˇ±

|