|

Report from

Europe

Sharp slowdown in EU wood furniture trade at

the end

of 2018

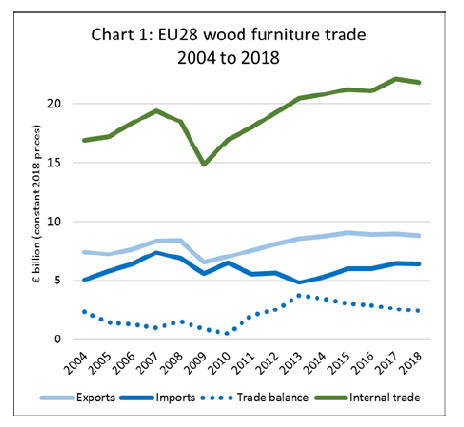

After a strong start to the year, the trade in wood furniture

slowed sharply in the last quarter of 2018. EU imports of

wood furniture from outside the region, which were up 6%

in the first nine months of 2018, finished the year down

around half a percentage point compared to 2017 at €6.36

billion. This is a reversal of the slow recovery in EU

imports that began in 2013. (Chart 1).

The decline in wood furniture imports closely mirrors

changes in the wider European economy.

According to the EU Winter 2019 Economic Forecast

published in February, economic activity in the EU cooled

in the second half of 2018 as political tensions and

uncertainty over fiscal policy and Brexit sapped business

and consumer confidence and output in some Member

States.

GDP growth in both the euro area and the EU slipped to

1.9% in 2018, down from 2.4% in 2017. Slowing

economic growth fed through into a fall in the value of the

euro and the British pound, both of which weakened

against the U.S. dollar by around 8% during 2018.

These changing economic conditions are also indicated by

a slowdown in internal EU wood furniture trade which,

after hitting a peak of €22.1 billion in 2017, fell back

nearly 7% in 2018 to €21.8 billion. The Brexit situation

led to a slowing in UK imports both from within and

outside the EU in the second half of 2018, while broader

concerns about the EU economy contributed to a slowdown

in trade elsewhere in the region.

The decline last year interrupts a long-term sharply rising

trend in internal EU trade on-going since the financial

crises in 2008-2009.

This long-term trend has been driven by increased market

integration within the EU, the shift in manufacturing from

higher cost countries in the western EU to lower cost

eastern locations, particularly Poland, and the growing

presence and influence of large-scale retailing chains

operating at cross country level, most notably IKEA. More

wood furniture imports into the EU from outside the

region are also now being funneled via the Netherlands.

The drive towards greater integration of the EU furniture

market and access to relatively lower cost manufacturing

locations in the eastern EU partly explains the continuing

dominance of EU-based manufacturers in the region.

ITTOˇŻs own estimates based on analysis of Eurostat data

indicate that EU-based manufacturers account for around

85% of all wood furniture sold in the region.

In recent years, European manufacturers have boosted

productivity and competitiveness through investment in

more advanced computer-controlled and automated

manufacturing, cutting overheads and reducing the relative

labour cost advantages of overseas producers.

ThereˇŻs been a particularly large investment by Western

European furniture manufacturers in Eastern European

countries, notably since their accession into the EU from

2004, and this is now maturing. From being principally

production satellites for large western European brands,

Eastern European manufacturers are now developing their

own identity and market momentum.

Furniture manufacturers in the EU area are also making a

virtue of their shorter supply chains which not only reduce

transport costs but also allow products to be delivered

more rapidly.

External suppliers face other more direct challenges to

expanding sales in the EU. Despite some recent

consolidation, there is still a relatively high degree of

fragmentation in the retailing sector in many European

countries which complicates market access. Many

overseas suppliers remain reliant on agents and lack direct

access to information on fashions and other market trends.

The progressive migration of European furniture sales

online is also tending to favour local manufacturers better

placed to meet the short lead times demanded by internet

retailers and consumers.

EU furniture manufacturers losing export market share

European furniture manufacturers are also strongly

motivated to maintain and increase share in their home

markets as they are now struggling to expand sales outside

the EU. Last year there was a 1.7% fall in the value of EU

wood furniture exports to €8.78 billion.

This continues a trend of flat-lining, or slowly declining

exports to countries outside the EU after reaching an alltime

high of just over €9 billion in 2015. Since then the

competitive benefits of the relative weakness of the euro

against the dollar and other cost saving efforts of EU wood

furniture manufacturers have waned.

Competition for EU-based manufacturers has intensified

from newly emerging producers in Eastern European

countries outside the EU, such as Bosnia, Ukraine and

Turkey, and from Vietnam which in the last 5 years has

rapidly overtaken all other tropical countries in the global

league table of wood furniture producing nations.

EU wood furniture manufacturers have suffered in higherend

export markets in Asia, the CIS and Middle East from

a range of factors including cooling of the Chinese

economy, a sharp fall in global equity markets towards the

end of 2018, extreme weakness of the Russian rouble,

relatively low oil prices and political instability.

Given domestic market problems in the EU and the

European Central BankˇŻs policy to keep interest rates at

record-lows to boost demand, the euro is expected to

depreciate against the dollar in 2019, which may boost EU

exports a little this year.

However, while the risk of outright global recession in

2019 still seems low, a general global deceleration is

widely forecast with growth falling below potential in

most regions. Overall therefore, EU wood furniture

exports are unlikely to rise significantly this year.

Challenging market for external suppliers to the EU

Prospects for non-EU wood furniture suppliers selling into

the EU are mixed. All suppliers face an uphill struggle to

compete with EU domestic manufacturers.

Added to this challenge this year is the economic

uncertainty inside the EU and the prospects for further

weakening of European currencies against the US dollar.

Gains are being made by some external suppliers, but

nearly all are in countries neighbouring the EU. Only one

tropical wood furniture supplier, India, is currently making

ground in the EU market.

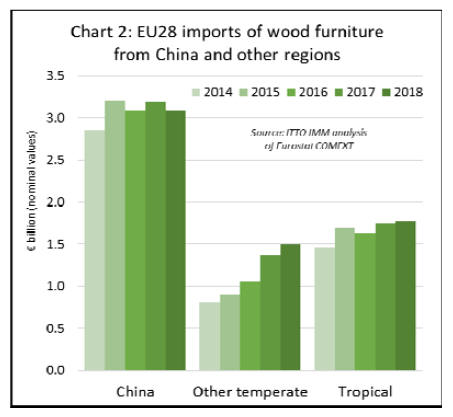

After a brief upturn in 2017, EU wood furniture imports

from China, by far the largest external supplier, fell 3% to

€3.09 billion in 2018. ChinaˇŻs competitiveness in the EU

wood furniture market has been impeded as prices have

risen on the back of growing domestic demand and new

laws for pollution control pollution in China.

In 2018, EU imports of wood furniture continued to rise

from other temperate countries, mainly bordering the EU.

EU imports from these countries increased 9% to €1.49

billion in 2018, building on a 28% gain recorded the

previous year. The biggest gains in 2018 were made by

Ukraine, Belarus, Russia, USA, Bosnia, and Turkey.

After a slow start to the year, EU imports of wood

furniture from tropical countries picked up pace a little in

the second half, and were €1.78 billion overall for 2018,

up 2% compared to the previous year (Chart 2).

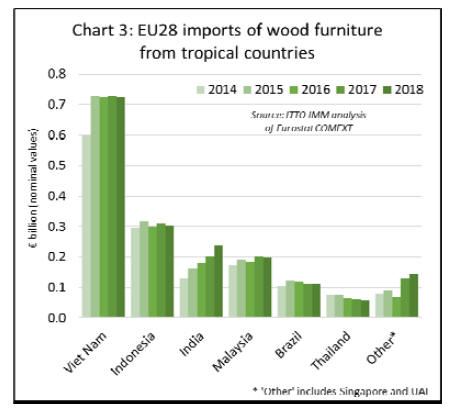

The main South East Asian supply countries have all

followed a similar trajectory in the EU wood furniture

market in the last two years. A rise in EU imports in 2017

was followed by a decline in 2018.

After increasing 1% to €728 million in 2017, EU imports

from Viet Nam fell 0.5% to €724 million in 2018. Imports

from Indonesia increased 4% to €311 million in 2017 but

fell back 2% to €304 million in 2018. Imports from

Malaysia increased 10% to €203 million in 2017 and were

2% down at €199 million last year.

In contrast, EU wood furniture imports from India

continued to rise, up 18% to €239 million in 2018 after a

12% increase to €202 million in 2017. Imports from Brazil

were €113 million in 2018, matching the 2017 level (Chart

3).

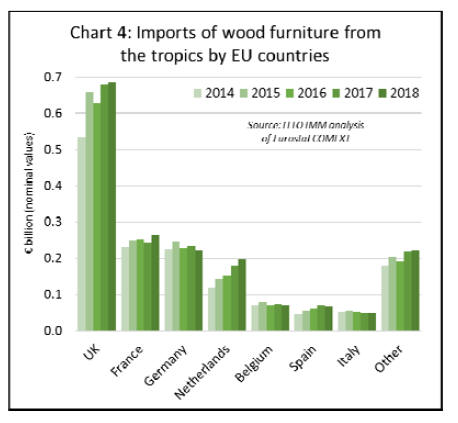

There were also shifts in the destinations for wood

furniture imported into the EU from tropical countries in

2018. Imports in the UK, the largest market, were €687

million last year, 1% more than in 2017. There were also

rising imports in France (+9% to €264 million) and

Netherlands (+9% to €198 million).

However, these gains in 2018 were offset by falling

imports of tropical wood furniture in Germany (-6% to

€220 million), Belgium (-2% to €72 million), Spain (-4%

to €67 million), and Italy (-1% to €50 million) (Chart 4).

Brexit saga damages prospects for market expansion

The UKˇŻs dominant position in the EU as by far the

leading destination for wood furniture imports from

tropical countries, suggests that the on-going Brexit saga

may have significant long-term effects.

While there may be long term benefits for external

suppliers resulting from the UKˇŻs decision to pull back

from deeper EU integration, these benefits seem to be a

very distant prospect. At present, the uncertainty is

significantly undermining prospects for market growth in

the short to medium term.

UK economic growth in 2018 was only 1.4%, down from

1.8% in 2017 and the joint worst year (with 2012) since

the financial crisis.

According to the latest UK government summary of

independent forecasts, UK growth is expected to be

around 1.3% in 2019 and even this is dependent on the UK

resolving the Brexit issue one way or the other.

Even now that the official Brexit date of 29th March 2019

has passed, the full economic and political fallout of the

UKˇŻs vote to depart the EU are very hard to predict.

With the UK government asking the EU for a delay until

such time as serious internal political differences can be

resolved, there is still uncertainty over the timing of

Brexit, or whether the UK will depart on terms agreed

with the EU or, failing that, there is a ˇ°disorderly exitˇ±

with attendant severe economic disruption. It is still

possible the UK changes course entirely and decides to

remain in the EU.

Overall the indications are that the UK market for wood

furniture, after making some small gains last year, will

contract in 2019.

EuropeˇŻs role in the global furniture trade

Despite recent deterioration in the EUˇŻs balance of

furniture trade, European manufacturers remain a major

force in the international furniture sector. Their dominance

of the EUˇŻs internal wood furniture market is also unlikely

to be seriously challenged in the foreseeable future.

This is made clear in a series of detailed reports on

EuropeˇŻs place in the global furniture sector newly

released by the Italy-based research organisation CSIL.

More details of the reports ˇ°The Fumiture Industry in

Europeˇ±, 'World Furniture Outlook 2019' and 'Forecast

Report on the Furniture Sector in Italy, 2019- 2021' are

available from www.worldfurnitureonline.com or by email

csil@csilmilano.com).

CSIL estimate the total value of global furniture trade in

2018 was around US$149 billion, 4% up on the previous

year and building on a 6% increase in 2017. CSIL expect

the world furniture trade to continue to grow by 4% in

2019.

CSIL reckon world furniture consumption was US$460

billion in 2018 (production prices excluding the markup

for distribution). World furniture consumption is forecast

by CSIL to rise around 3.2% in real terms this year with

growth concentrated in Asia and Pacific.

In the EU, CSIL estimate that total furniture production

continued to grow in 2018, rising between 1% and 2% in

real terms. According to CSIL forecasts, this rate of

growth should continue until at least 2020.

The CSIL global ranking of 100 countries identifies

Germany, the UK and France as the main importing

countries worldwide after the United States (although at a

distance). Germany, Italy and Poland are the main

exporting countries at a global level, after China (at a

distance).

CSIL highlight that while Asia has become more dominant

in the global furniture sector, Europe remains the second

largest furniture manufacturing region in the world and

still accounts for around one quarter of global furniture

production.

Europe is also the headquarters of some of the largest and

most important sector players (around one third of the top

200 largest furniture companies in the world are located

here).

Europe accounts for roughly one quarter of the global

world furniture market. Per capita furniture consumption

is the highest in the world (alongside North America).

Europe accounts for around 44% of world furniture

imports and 41% of world furniture exports.

CSIL points out that the EU furniture sector now employs

around one million workers, many of which are highly

skilled, in 121,500 manufacturing firms, mainly micro and

small sized. This, together with a rich cultural heritage,

gives European manufacturers a competitive edge and

promotes the development of creative competences which

are recognized worldwide.

CSIL note that ˇ°the European industry is able to combine

new technologies and innovation with cultural heritage,

tradition and style, providing jobs for skilled workers and

is also a world leader in the high-end segment of the

furniture marketˇ±.

CSIL suggest that in addition to the barriers created by a

large and highly competitive domestic industry, there are

other obstacles to non-EU producers entering the market,

including logistical costs and requirements for various

forms of certification to specific technical and

environmental standards.

|