|

Report from

Europe

Tropical timber yet to benefit from more resilient EU

trade

Drawing on interviews with timber trade associations

across the region, the latest newsletter of the European

Timber Trade Federation (soon to be published at

http://www.ettf.info/ettf_news) will show that the

European timber market continues to grow slowly and

broadly in line with GDP forecasts of 2.4% in 2018 and

2.3% and 2% in 2019.

It also highlights that trade growth is becoming more

widespread and resilient in southern European countries,

including in Italy, Spain and Greece.

However, growth has lost momentum in the UK, the

largest EU importer from outside the region. ITTOˇŻs own

analysis of trade data also indicates that much of the recent

gain has been in internal EU trade and imports from

neighbouring European countries, rather than in imports

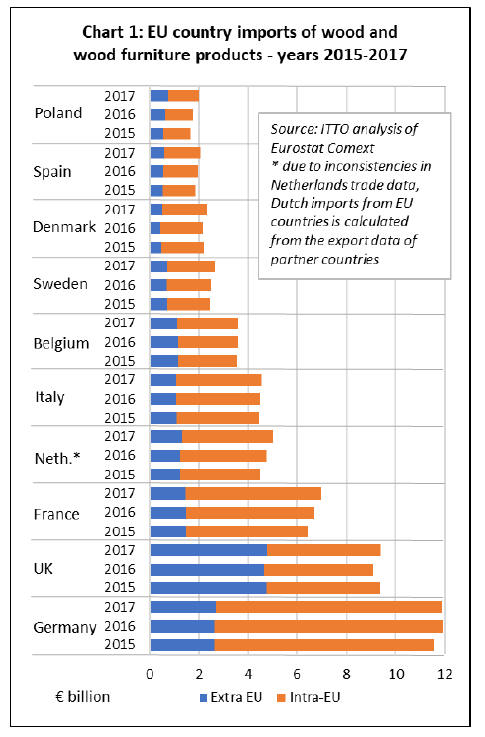

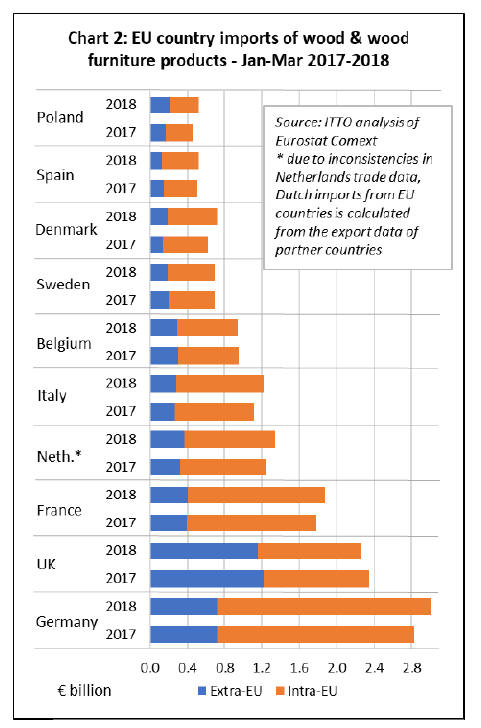

from the tropics and other regions (Charts 1 and 2).

German timber imports rise in 2018 after stalling last

year

In 2017, total German imports of wood products

(including all those in HS 44 and wood furniture in HS 94)

declined 0.7% to €11.88 billion. GermanyˇŻs imports from

inside the EU fell slightly, by 1.7%, to €9.17 billion in

2017, while imports from outside the region increased

2.6% to €2.71 billion.

Most of the gains in German imports during 2017 were

from Russia, Belarus and Ukraine. However, trade also

increased 5% with Indonesia, GermanyˇŻs largest tropical

supplier, to €158 million. In the first quarter of 2018,

German imports were up 6% to €2.28 billion, with nearly

all the gains in imports from other EU countries.

According to GD Holz, German sales of lumber and

planed timber slowed in the first quarter of 2018, but

flooring and building products sales were very robust.

From a tropical perspective, a decline in garden and

outdoor products sales was a concern in the first quarter,

but this trend is likely to have reversed as the weather has

improved. Construction is also set for a strong year in

Germany.

German importers report some shortages in certain timber

categories, including tropical plywood and decking, but

with woodworking order books full, traders are expecting

further growth in overall demand for timber products.

French trade benefits from rising construction trend

In France, the importers association Le Commerce du Bois

reports that trade was buoyed by 2%-plus GDP growth last

year and continues to benefit from a rising trend in

construction, with housing starts in March at the 427,000

per annum level which compares to 360,000 starts in 2016.

The French timber trade also expects to benefit

increasingly from government measures to improve

building energy performance and incentivise wood use in

construction and from the new €10 million promotional

programme, ˇ®Pour mois, cˇŻest le boisˇŻˇ±.

This campaign is led by the French national wood

association France Bois For¨şt and supported by other trade

and industry bodies. It aims to ˇ°increase the volume of

wood consumption in France and increase market share

for domestic productionˇ±.

To date, signs are that the revival in French demand and

the promotion campaigns are benefitting mainly European

suppliers. The total value of French imports of wood

products increased 4.4% to €6.99 billion in 2017.

However, imports from inside the EU increased 6.3% to

€5.52 billion while imports from outside the EU declined

2.3% to €1.48 billion.

In the first quarter of 2018, French imports increased 5.4%

compared to the same period in 2017, with imports from

inside the EU rising 6.3% to €1.47 billion and imports

from outside the EU up 2.2% to €402 million.

All key sectors expanding in Belgium

In Belgium, the Fedustria association, which since last

year has also covered the importing sector, reports that all

key sectors enjoyed growth in 2017. The main drivers

were higher consumer spending and construction growth

of 3.1%. Sales of wood building products and systems

were up 5.3%, while sheet materials also performed

strongly.

Although Belgian timber sector confidence dipped a little

in early 2018, Fedustria is optimistic of boosting market

prospects via the latest wave of its wood promotion

campaign: ˇ°Wood gives oxygenˇ±.

Similar to France, the recent gains in Belgian trade have

mainly benefitted other European countries. Belgian wood

products imports increased 0.8% to €3.60 billion in 2017.

Imports from within the EU increased 3.2% to €2.48

billion while imports from outside the EU declined 4.1%

to €1.12 billion.

Belgian imports in the first quarter of 2018 were €950

million, no change from the same period in previous year.

Imporst from inside the EU increased 0.7% while imports

from outside the EU declined 2.2%.

In the panels sector, Fedustria highlight that the industry

faces ever-tighter rules on emissions, adhesives and ˇ®best

available techniquesˇŻ application. Consequently, the

Belgian association is working with the European Panel

Federation to ensure products imported into the EU meet

the same high standards and do not compete ˇ®unfairlyˇŻ.

Netherlands growth at the highest level for a decade

In the Netherlands, economic growth is at its highest point

since 2008, consumer confidence is high, and timber trade

turnover is rising. The Netherlands imports of wood

products increased 5.3% to €5.03 billion in 2017.

Imports increased from inside the EU by 4.7% to €3.7

billion and from outside the EU by 7% to €1.33 billion.

These trends continued in the first quarter of 2018, with

imports rising another 7.2% to €1.34 billion compared to

the same period in 2017. Imports from inside the EU

gained 5.6% to €975 million and from outside the EU the

rise was 11.7% to €366 million.

Most of the growth in Netherlands imports from outside

the EU has comprised wood furniture from China,

Indonesia, Vietnam and India, and sawnwood from

Russia.

While demand is expanding, the Netherlands Timber

Trade Association reports that the trade is experiencing

some pressures with stock prices rising and supply

constraints for some products. A lack of skilled labour is

also curbing constructionˇŻs growth capacity and civil

works are still not back to pre-recession levels.

Italian imports rising more strongly in 2018

According to the ETTF newsletter, new Fedecomlegno

Secretary General Massimo Fiorini takes ItalyˇŻs rise in

timber imports in 2017 as a key indicator of the sectorˇŻs

recovery.

Overall, ItalyˇŻs wood and wood furniture imports

increased 1.8% to €4.6 billion in 2017. Imports from

within the EU increased 2.3% to €3.53 billion and imports

from outside the EU increased by 0.2% to 1.06 billion.

ItalyˇŻs imports also picked up pace in the first quarter of

2018, rising 8.9% to €1.22 billion, increasing 9.9% from

inside the EU and 5.9% from outside the EU.

One market driver in Italy is an upswing in the property

sector since 2017, which resulted in rising imports of sawn

timber, wood flooring, and joinery products.

While the signs in Italy are encouraging, the recovery has

yet to extend to tropical wood. Imports from the largest

suppliers of tropical timber into Italy ¨C Cameroon and

Indonesia ¨C fell during 2017.

Italian imports from Brazil increased, but this was mainly

plantation softwood plywood rather than tropical

hardwood.

From within the EU, there was a significant increase in

imports from Austria, ItalyˇŻs largest external wood

supplier, together with Poland and Slovenia.

Much of the recent gain in Italian imports from outside the

EU has comprised furniture from China ¨C which may be

seen as a negative by ItalyˇŻs large and still dominant

domestic furniture sector ¨C together with sawnwood from

Ukraine and birch plywood from Russia.

Volatility in the UK trade

The UK Timber Trade Federation (TTF) reports that the

last two yearsˇŻ have been volatile due to uncertainties over

Brexit and subsequent currency fluctuation. The timber

trade had weathered this until now, but into 2018

conditions have worsened, with wood and wood products

imports declining 3.2% in the first quarter compared to the

same period in 2017.

Imports from within the EU fell 1.5% to €1.11 billion

while those from outside the EU fell 4.7% to €1.15 billion.

The decline in UK imports from outside the EU this year

has been concentrated in plywood and joinery products

from China, sawn hardwood from the USA, and pellets

from the USA and Canada.

The slowdown in UK imports is attributed partly to poor

weather and the collapse of giant contractor Carillion and

partly uncertainty surrounding Brexit with the UK moving

from the fastest to the slowest growing EU economy.

With the UK due to leave the EU in March 2019, the full

impact of Brexit has yet to be felt. The TTF has warned

that Brexit could land the UK trade with a ˇ®£1 billion tax

billˇŻ in non-deferrable VAT on wood imports from the

EU. Currently under EU rules, importers can clear goods

through customs and pay VAT later, a major cashflow

benefit.

However, once the UK leaves the EU VAT area, 20%

VAT will have to be paid on goodsˇŻ arrival. The TTF is

concerned that this will contribute to additional costs for

storing at ports and delays due to administering customs

checks and documentation. The TTF is therefore urging

government to maintain existing EU VAT arrangements.

While from the perspective of the TTF, the extra

bureaucracy of doing trade with the EU after Brexit is a

clear disadvantage, these issues may create some new

opportunities for suppliers outside the EU.

In 2017, the UK imported wood and wood furniture

products with a total value of €9.4 billion (US$10.9

billion) of which 49% derived from other EU countries.

The UK is already by far the largest EU importer of wood

products from outside the region ¨C alone accounting for

25% of all extra-EU imports and 27% of EU tropical

imports - and Brexit may increase this tendency to trade

with countries outside the EU.

However, these new opportunities need to be balanced

against the potential negative impact of Brexit on the

overall UK economy.

Rising optimism in Danish trade

According to the Danish Timber Trade Federation,

Denmark is enjoying 2% annual GDP growth and its

construction sector is optimistic again after several years

of crisis.

The timber sector is benefitting accordingly with a rise in

both import and consumption of wood products, both from

within and outside the EU. Prices are also trending

upwards in softwood, hardwood and certain panel

products.

In 2017, Denmark imported wood and wood furniture

products to a total value of €2.37 billion, nearly 10% more

than in 2016. Imports increased 9% to €1.88 billion from

other EU countries and 13.5% to €490 million from

outside the EU.

DenmarkˇŻs imports increased a further 16% in the first

quarter of 2018 comparted to the same period in 2017,

rising 10% from inside the EU and over 37% from outside

the EU.

A large proportion of the increase in Danish imports from

outside the EU comprises biomass from Russia and the

US, however there was also an increase in wood furniture

imports from Vietnam and, to a lesser extent, Indonesia.

Tourist industry puts floor under Greek demand

In Greece, the level of timber trade is still restricted

following the financial crises which came to a head in

2010 and led to a 25% reduction in total national GDP and

an estimated 85% contraction of the wood sector. In 2017,

Greek wood and wood furniture imports declined 2% to

€420 million, after a 10% rise the year before.

However, in 2018 investment in construction for the

tourist sector, particularly for major hotel developments

but also including the small private rental market, is giving

the Greek timber industry a modest, but much needed

boost, according to HTCA, the Greek timber trade

association.

The HTCA acknowledges that building and timber

industries have been particularly hard hit in the economic

crisis. But domestic and inward investment in tourism

related projects is on the increase, and, in line with a wider

upturn in the use of timber in construction, these are

featuring more wood products and systems than in the

past.

This is beginning to have an impact on imports which

were €69 million in the first quarter of 2018, nearly 10%

more than the same period in 2017, rising 13% from

within the EU and 6% from outside the EU. From outside

the EU, there has been particularly strong growth in Greek

imports of wood furniture from China and plywood from

Russia this year.

Russian timber sector in buoyant mood

According to a report in the ETTF Newsletter by

Sviatoslav Bychkov, Ilim Timber Managing Director,

Marketing and Communications, the Russian timber sector

is in buoyant mood and increasing capacity, including in

wood-based construction, after a robust performance in

2017.In 2017 Russia GDP grew 1.5%, successfully taking

the country out of economic recession.

The woodworking industries were part of this success,

contributing 1.9% to GDP, with the sawmill sector

achieving 2.2% growth and its further expansion reflected

in a 60.7% increase in production and processing

equipment imports.

Saw log production rose 4% to reach 79 million m3, while

exports contracted 1.5% to 11 million m3, with the bulk

going to China. Meanwhile market prices for Russian

sawn softwood exports grew an average of 10% in Asia,

Europe and the Middle East and North Africa (MENA),

driven by a number of factors, including demand on the

domestic market.

China overall accounted for 58% of sawn timber and 95%

of log exports from Russia in 2017. The former percentage

represented 21% volume growth to a total of 15.5 million

cu.m.

Reflecting the migration to processed timber exports,

Manzhouli, the major land port for Russian timber exports

to China, achieved a record high volume of sawn timber

handled, at 8 million m3 and saw a record low volume

throughput of saw logs at 3.8 million m3. In 2017, Russian

exporters also started to explore railway connections to

ChinaˇŻs Sichuan province using container block trains.

At the same time the reorientation of lumber exports away

from CIS and MENA markets continued, resulting in these

accounting for just 20% of the total.

In this buoyant market, all major Russian producers

reported that they were increasing production volumes,

adding shifts and also modernizing technology. Capital

investment was estimated to have increased sawn goods

capacity by 600,000cu.m in 2017, with a further

500,000cu.m forecast for 2018.

Due to demand, sawmillers in the North West region

started to experience some saw log shortages, while

Siberia reported record high harvest volumes.

Further reflecting production growth, a number of mills in

Siberia and eastern regions have started fuel pellet

production to manage by-products output, increasing

overall industry capacity by 31%.

Annual plywood production, primarily birch, has been

stable at 3.7 million m3 for three years, with 50%

exported, mainly to the US, UK and rest of the EU, but an

estimated 200,000cu.m of new capacity is forecast to be

added this year.

FSC certification has grown to cover 48.3 million hectares

of Russian commercial forest. Russia now accounts for

25% of the FSC certified forest area worldwide.

Yacht industry calls for co-operation with Myanmar on

teak

According to a report in the ETTF newsletter, an

international alliance of yacht sector and associated

organisations has cautioned against a ban on trade in

Myanmar teak. Instead it urges industry, governments and

NGOs to support the countryˇŻs efforts to reform forest

management and improve legality assurance.

The Large Yacht Cluster (LYC) comprises shipyards, teak

importers and suppliers, national and international trade

bodies and NGOs. Its core aim is a ˇ®sustainable teak value

chainˇŻ. The organisation says teak is prized in yacht

making, not just for aesthetics, but also its durability and

anti-slip characteristics and the fact that it does not warp,

attract insects, or absorb moisture.

At the same time the cluster says it is ˇ°fully aware of the

fragile status of teak and the consequences of unlawful

traded timberˇ±.

However, it warns that banning trade in the timber will

only promote exports to less environmentally concerned

markets, reduce support for Myanmar to strengthen

environmental controls and undermine its ability to tackle

illegality.

The cluster says the requirements on legality assurance of

the EU Timber Regulation, US Lacey Act and Australian

Illegal Logging Prohibition Regulation are promoted in the

industry, as well as 'certification references such as FSC

and PEFC'.

But it also urges greater international harmonisation of

market legality requirements 'to ensure a global approach,

a level playing field and harmonised enforcement'.

It additionally backs development of alternative materials

to partly spare teak and is working on guidelines for using

less teak per vessel to reduce pressure on stock.

The core appeals in the position paper are for:

international support for MyanmarˇŻs efforts to create a

sustainable teak value chain; endorsement of this stance

from national and international institutions and trade

bodies; support for education of the yacht industry on teak

issues; national enforcement agencies to work

collaboratively ¨C 'taking a constructive approach and

refraining from unconstructive and unequal measures and

penalties against those that do their utmostˇŻ.

EUTR having a significant impact on purchasing

decisions

Much timber trade policy discussion in the EU now

focuses heavily on developments in the EU Timber

Regulation (EUTR) which, given its scope covering nearly

all timber products and importing companies in the EU, is

having a significant effect to influence purchasing

decisions, particularly in relation to tropical timber

products.

The latest European Timber Trade Federation newsletter

(soon to be published at http://www.ettf.info/ettf_news) is

said to include cludes details of the European timber

tradeˇŻs views on the implementation and enforcement of

EUTR.

Information on the latest EUTR developments is also

provided in a regular briefing note issued by UNEPWCMC

in its capacity as a consultant to the European

Commission and based on information provided by the

Member States Competent Authorities (CAs).

Drawing on a survey of 20 CAs in the second half of 2017,

the latest UNEP-WCMC briefing provides details of

EUTR compliance checks performed and penalties

imposed to enforce EUTR implementation.

The respondents reported conducting checks on more than

467 domestic operators, 388 importing operators, 300

traders dealing with domestic timber, 177 traders dealing

with imported timber and three monitoring organisations,

over the period June-November 2017.

The report also includes a summary of the latest

FLEGT/EUTR Expert Group meeting in Brussels during

April where it notes that ˇ°some Member States reported

substantiated concerns regarding companies placing

timber from high-risk countries on the EU market,

including from Myanmar and Brazil.

The conclusion of the EUTR Expert Group meeting of 20

September 2017 was reiterated and it is still not possible

for operators to demonstrate compliance with EUTR due

diligence obligations as regards timber imports from

Myanmarˇ±.

According to WCMC-UNEP, the FLEGT/EUTR Expert

Group meeting in April also included a presentation on a

TAIEX mission to Ukraine which reported that ˇ°a

substantial corruption risk can be found in every supply

chain and is widespread throughout the country however,

there was not enough public information available to

convince EU operators of the risksˇ±.

Eurostat data compiled by ITTO shows that in 2017 the

EU imported EUTR regulated products with a total value

of €950 million from Ukraine, which compares to €554

million in 2013 when the EUTR was first introduced, a

72% increase.

EU timber imports from Ukraine comprise a wide range of

products, led by sawn hardwood and softwood and

veneers, mainly destined for Poland, Germany, Romania,

Hungary and Italy.

Links to the UNEP-WCMC briefing notes together with

other EC information on the EUTR are available at

http://ec.europa.eu/environment/forests/timber_regulation.

htm#products.

|