|

Report from

Europe

EU tropical timber imports flat-line in 2018

The slowdown in EU imports of tropical products, which

began in 2016 and continued throughout last year, levelled

off in the first quarter of 2018.

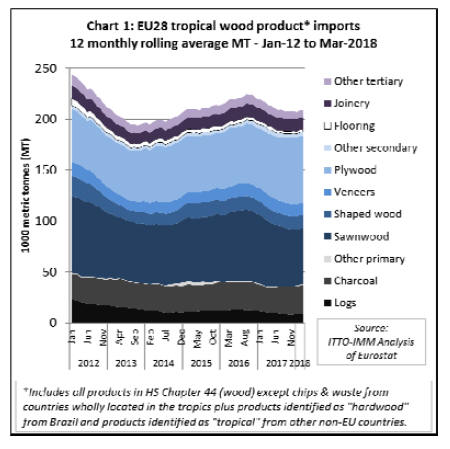

Chart 1 shows twelve monthly rolling average imports (to

iron out seasonal fluctuations) into the EU of all tropical

wood products listed in HS Chapter 44 (excluding wood

waste and chips). It shows that imports peaked at an

average of 224,000 metric tonnes (MT) per month in

September 2016, slipped to a low of 207,000 MT in

January this year and recovered only slightly, to 209,000

MT, by March 2018 (Chart 1).

EU imports of tropical wood products in the first quarter

of 2018 were only around 7% more than the all-time low

of 195,000 MT per month recorded in the middle of 2013

at the height of the euro-zone crises.

In value terms, EU imports of tropical wood products

averaged around euro203 million per month in the first

quarter of 2018, 13% more than the all-time low in 2013

but 6% down on the level prevailing in 2016.

Most of the rise and subsequent slowdown in EU tropical

imports in the last three years was driven by sawnwood.

The stabilisation of the EUˇŻs tropical wood trade so far in

2018 is mainly due to a slight uptick in imports of

plywood and charcoal.

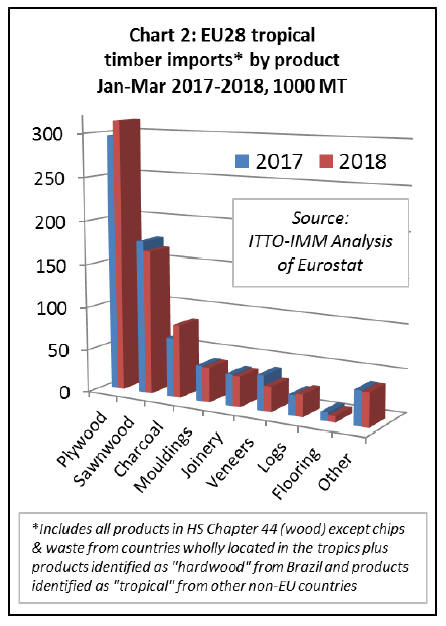

In the first quarter of 2018 compared to the same period in

2017, total EU imports of tropical wood products

increased 1% to 740,000 MT. There was a 23% rise in

imports of tropical charcoal to 85,000 MT, a 6% rise in

imports of tropical plywood to 314,000 MT, and 9% rise

in imports of other secondary products (such as fibreboard

and sleepers) to 14,000 MT.

However, these gains were largely offset by a 6% decline

in EU imports of tropical sawn to 166,000 MT, a 28%

decline in imports of tropical veneer to 29,000 MT, a 2%

fall in imports of tropical mouldings to 40,000 MT, and a

10% fall in imports of various tertiary products (such as

flooring, glulam and other joinery, marquetry, and wooden

tools) to 64,000 MT (Chart 2).

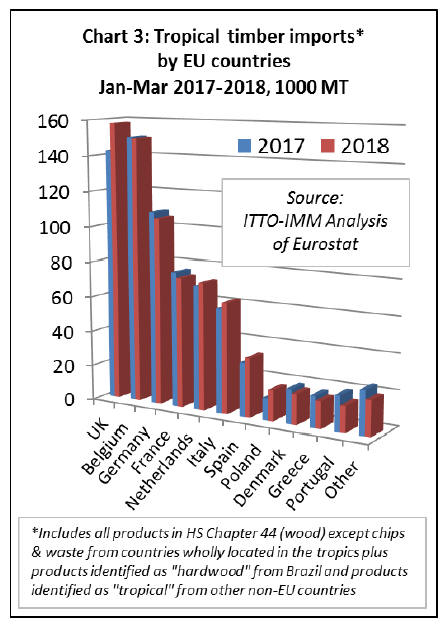

Recorded rise in UK tropical imports may be

misleading

In the first quarter of 2018, imports of tropical wood

products appear to have been more buoyant in the UK than

other EU markets. UK imports were 158,000 MT during

the period, 11% more than the previous year.

However, this gain was almost all due to an apparent rise

in UK imports of hardwood plywood from Brazil. The

sharp increase recorded in Eurostat import statistics is not

matched by any significant increase in Brazilian export

statistics for hardwood plywood to the UK.

This may well be a statistical error (such as Elliottis pine

plywood being misidentified as hardwood).

Other EU markets reporting growth in tropical wood

imports the first quarter include the Netherlands (+3% to

72,300 MT), Italy (+6% 62,600 MT) and Spain (+10% to

33,300 MT). However, the fastest growth of all was in

Poland which registered an increase of 39% to 17,300 MT.

This was due almost entirely to a sharp rise in PolandˇŻs

imports of charcoal from Nigeria.

Imports of tropical wood products in Belgium were

150,000 MT in the first quarter of 2018, the same as in

2017. Imports in Germany and France slipped a little in

the first three months of 2018, down 3% and 4%

respectively compared to the same period last year. (Chart

3).

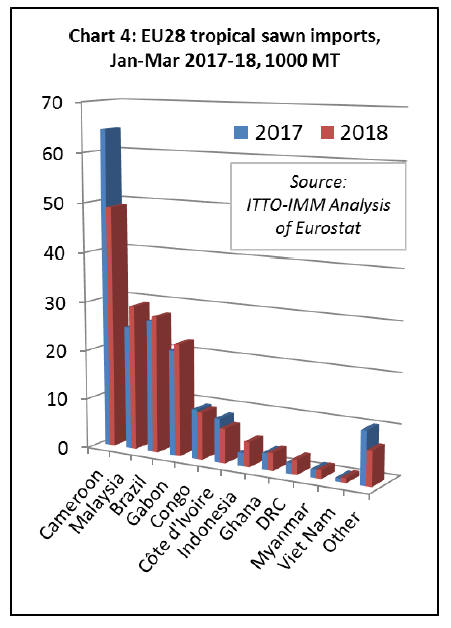

First quarter decline in EU imports of tropical

sawnwood

EU imports of tropical sawn wood decreased 6% to

166,100 MT in the first quarter of 2018. This was mainly

due to a continuing slide in imports from Cameroon, ongoing

since the end of 2016.

EU imports of tropical sawn wood from the central

African country declined a further 24% to 49,000 MT in

the first three months of 2017. Imports also fell from

Congo (down 4% to 9,400 MT), and Côte d'Ivoire (down

21% to 6,800 MT).

However, after a decline in 2017, EU imports of tropical

sawn wood from Malaysia increased 18% to 29,300 MT in

the first quarter of 2018. There was also a rise in imports

from Brazil (+3% to 27,600 MT), Gabon (+7% to 22,600

MT), and Ghana (+8% to 3,600 MT) and DRC _+36% to

3,000 MT). (Chart 4).

An 86% rise in EU imports of sawn wood from Indonesia

(to 5,000 MT), a country which restricts exports in this

product group to profiled wood, may be partly due to

reclassification of some wood mouldings products from

HS4409 to HS4407.

Introduction of the FLEGT licensing system in Indonesia

since November 2016 has led to some changes in the HS

codes used for Indonesian products by EU customs and

operators to ensure consistency between codes identified

on the licences issued in Indonesia and the codes entered

on to customs forms for entry into the EU.

In the first quarter of 2018, tropical sawn hardwood

imports declined 14% to 51,900 MT in Belgium, 9% to

18,600 MT in France, 30% to 10,700 tonnes in the UK,

11% to 6,800 MT in Germany, and 50% to 3,800 MT in

Portugal.

These losses were partially offset by a 33% rise to 35,200

MT in the Netherlands, a 22% rise to 17,800 MT in Italy

and a 6% rise to 12,600 MT in Spain.

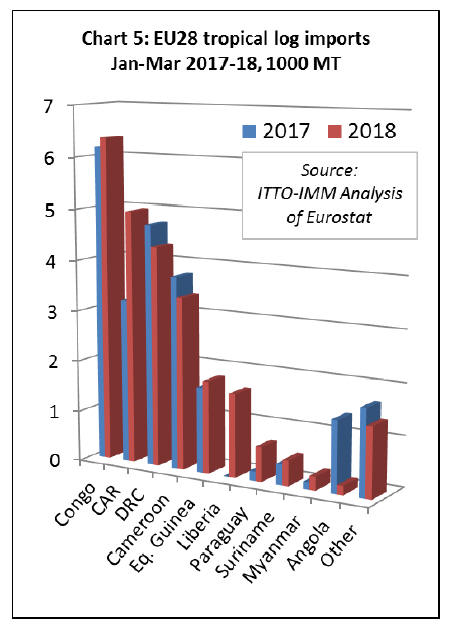

EU imports of tropical logs recover a little ground

After a downturn in 2017, EU imports of tropical logs

recovered a little ground at the start of 2018. Imports of

25,500 MT during the first quarter of the year were 9%

greater than the same period in 2017. EU imports of

tropical logs increased from the two leading suppliers,

Congo (rising 3% to 6,400 MT) and CAR (rising 54% to

5,000 MT).

EU log imports from Equatorial Guinea also increased

during the period, by 8% to 1,800 MT. Imports from

Liberia, of which there were none in the first quarter last

year, were 1,600 MT in the same period this year.

However, during the first quarter of 2018, EU imports of

tropical logs declined 9% from DRC to 4,300 MT and

11% from Cameroon to 3,400 MT. EU log imports from

Angola, which increased sharply in 2017, were again at

negligible levels in the first quarter of this year (Chart 5).

Most of the gain in EU imports of tropical logs in the first

quarter of 2018 was concentrated in France (+43% to

11,400 MT) and Belgium (+15% to 5,800 MT). Imports of

tropical logs in Portugal fell 32% to 3,800 MT during the

period.

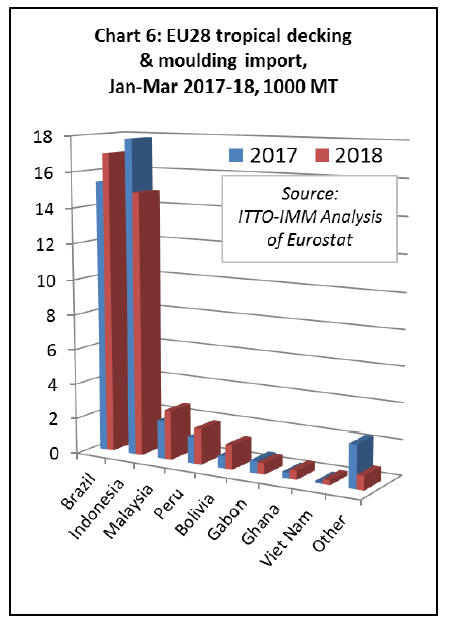

Stability in EU tropical decking imports

EU imports of tropical mouldings (which includes both

interior mouldings and exterior decking products) fell

slightly, by 2% to 40,200 MT in the first quarter of 2018.

A 10% rise in imports from Brazil to 17,000 MT offset a

17% decline in imports from Indonesia to 14,900 MT. As

noted earlier, the latter decline may be partly due to

alterations in the HS codes used to record imports from

Indonesia following introduction of FLEGT licensing.

EU imports of mouldings increased for some smaller

suppliers of this commodity in the first quarter of 2018

including Malaysia (+29% to 2,800 MT), Peru (+33% to

2,000 MT) and Bolivia (+100% to 1,400 MT) (Chart 6).

In the first quarter of 2018, imports of tropical decking

increased in France and Belgium but declined in Germany,

the Netherlands and the UK.

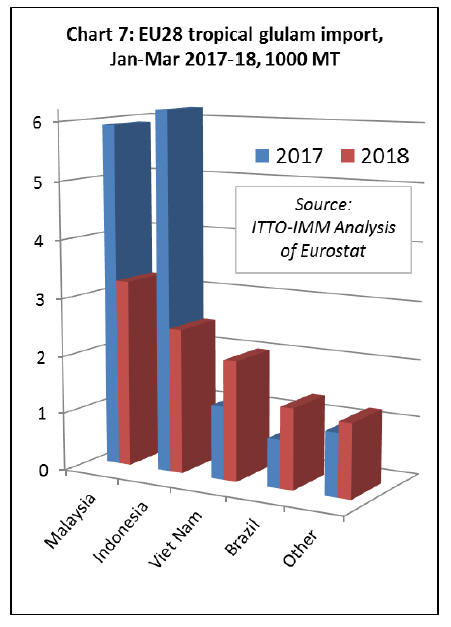

Sharp fall in EU imports of tropical glulam

EU imports of tropical glulam, mainly laminated window

scantlings, decreased 37% to 9,800 MT in the first quarter

of 2018. Imports decreased from both the leading

suppliers, falling 45% to 3,200 MT from Malaysia and

60% to 2,500 MT from Indonesia. (Chart 7).

Following introduction of FLEGT licensing in Indonesia,

a proportion of Indonesian products previously identified

as glulam (EU CN product code 44189010) is now being

classified as plywood (EU CN Code 4412) on EU customs

forms to ensure consistency with the FLEGT licenses

issued in Indonesia. Indonesia has no code comparable to

the EU code for ˇ°glulamˇ± in their national system to

classify products in trade.

In the first quarter of 2018 EU imports of tropical glulam

fell by 73% to 1,880 in the Netherlands, by 18% to 3,000

MT in Belgium, and by 38% to 1850 MT in Germany.

However, imports increased by 146% to 2,250 MT in

France.

Note that EU import data for the first quarter of 2018 for

tropical veneer, plywood, flooring, and wood furniture

will be included in the next market report.

European economic recovery loses momentum

During the first quarter of 2018, there was a loss of

momentum in the economic recovery that has been

underway in the EU since the start of 2017. The pace of

economic expansion in Germany was cut in half during the

period due mainly to weaker trade.

The 0.3% increase in GDP in EuropeˇŻs largest economy

was softer than forecast and the weakest in more than a

year. Dutch and Portuguese growth also cooled more than

expected in the first quarter, while a similar trend was seen

across central and eastern Europe.

Overall, euro-area growth was only 0.4% during the 3-

month period, well below expectations. It is unclear at this

stage whether the slowing rate of growth at the start of

2018 is merely a soft patch or indicative of something

more alarming.

So far, official forecasters have largely dismissed the

sluggish start to the year -- blaming factors such as colder

weather -- and expressed confidence that weakness will

dissipate.

The IMFˇŻs latest forecasts, published following the first

quarter results, suggest that growth in advanced European

economies, mainly the euro zone, would slow to 2.3% this

year from 2.4% in 2017 and then decelerate to 2.0 percent

in 2019.

The European Commission also downplayed concerns and

has maintained its forecast that full-year growth will

almost match the decade-high pace hit in 2017.

However, there are threats. The euro fell to six-month low

after the German GDP figures and other discouraging data

from the latest IHS Markit purchasing managersˇŻ surveys

which showed that forward looking indicators had also

deteriorated, suggesting no immediate bounce-back.

The IMF latest report highlights that European

governments have so far largely failed to use the breathing

space offered by improved economic conditions to push

forward with reforms needed to boost long-term growth.

Despite the recent growth, some of the biggest euro zone

economies like France, Italy or Spain have been slow to

further reduce their budget deficits towards a balanced

position while others, like Belgium, are increasing the

shortfall.

Concerns are also mounting in Europe about rising trade

protectionism, higher oil prices, the fallout from Brexit

scheduled for March next year, and the political situation

in Italy.

Of these issues, the last is potentially the most critical.

Economists calculate the cost of the promises made by

ItalyˇŻs newly installed government ¨C which include lower

taxes, higher benefits, and earlier retirement ¨C could reach

Euro170bn, or about 10% of ItalyˇŻs GDP. This would add

to the countryˇŻs Euro2.1trn debt mountain and potentially

trigger the EUˇŻs worst-case scenario: a Greek-style debt

crisis in the eurozoneˇŻs third-biggest economy.

There are also clouds on the horizon in the UK. One of

the UKˇŻs leading economic thinktanks has slashed its

forecasts for 2018 following evidence that growth almost

came to a halt in the first three months of the year.

The National Institute for Economic and Social Research

(NIESR) said it expected GDP expansion of 1.4% in 2018

¨C a sharp reduction from the 1.9% it had been predicting

three months ago. The revision followed publication of

official figures showing the UK economy grew by only

0.1% in the first three months of 2018 ¨C well below the

0.5% the think-tank had been forecasting.

As elsewhere in the EU, it is not clear if this is just a soft

patch or the start of a prolonged period of weakness. At

present, NIESR still expects UK to pick up to average

around 0.4% in each of the next three quarters.

The latest data on UK construction provides some little

reassurance. A pick-up in housebuilding helped the

building sector, which suffered from very poor levels of

activity in the first quarter, to bounce back in April.

However, overall demand for new buildings in the UK

remained subdued, according to the Markit/Cips UK

construction purchasing managersˇŻ index, with total new

work rising only modestly on the month. While

housebuilding bolstered growth in April, the picture was

less positive in other areas of construction, with

commercial building and civil engineering work rising

only marginally.

UK construction market analysts suggest that heightened

economic uncertainty, alongside lack of clarity on the

Brexit negotiations, is creating a risk-averse mood among

clients, leading to spending plans being delayed. Growth

in the UK construction sector is also likely to be

dampened by a planned 5.4% reduction in public sector

investment this year.

|