|

Report from

North America

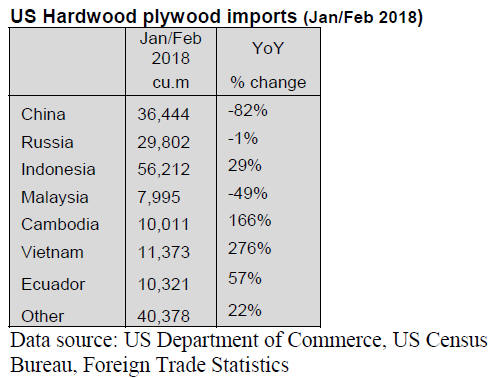

Indonesia currently largest supplier of hardwood

plywood to US

Hardwood plywood imports were down 14% in February

(173,179 cu.m.). Imports from most countries declined

month-over-month with the largest fall in shipments from

China and Russia. Imports from Malaysia increased from

January, but MalaysiaˇŻs shipments to the US have not yet

recovered to 2017 levels.

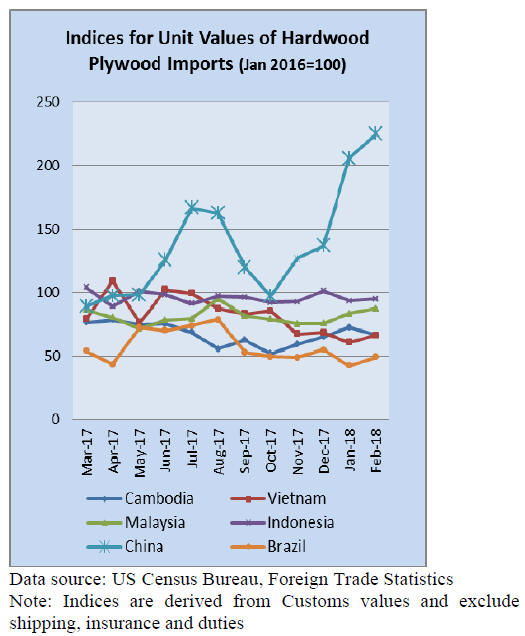

Year-to-date plywood imports fell 40% compared to

February 2017, but the value of imports decreased by only

25% due to higher prices of Chinese plywood in recent

months.

Unsurprisingly the largest drop was in imports from

China, while imports from Vietnam and Cambodia gained

after the US introduced antidumping and countervailing

duties on Chinese hardwood plywood. In terms of volume,

Indonesia has replaced China as the largest supplier of

hardwood plywood to the US.

Wood product imports down except hardwood flooring

Hardwood flooring imports were up in February while

imports of tropical veneer, hardwood moulding and

assembled flooring panels declined from January.

Hardwood flooring imports increased 18% year-to-date

and 25% month-over-month in February.

Flooring imports from Malaysia tripled from January to

737,580 cu.m. Hardwood flooring shipments from China

and Vietnam were down in February. In assembled

flooring panels (engineered and laminate) imports from

Europe grew significantly in February.

Tropical veneer imports from China fell in February,

following two months of higher imports. Veneer is not

affected by the U.S. duties on hardwood plywood.

Decline in wooden furniture imports

Wooden furniture imports declined in February to under

US$1.6 billion, but year-to-date imports remain higher

than in February last year.

The month-on-month decline was mainly in imports from

China and Vietnam, but imports from most other suppliers

(except Canada) were also down. Non-upholstered seating

imports were unchanged from January, but imports of all

other types of wooden furniture posted declined.

Furniture and home furnishing retails sales rise first

quarter

The furniture and wood products manufacturing industries

reported growth in March, according the Institute for

Supply ManagementˇŻs survey (Manufacturing ISM Report

On Business).

New furniture orders in January were up 2% over orders in

January 2017, according to the Smith Leonard survey of

U.S. residential furniture manufacturers and distributors.

Furniture shipments in January were unchanged from the

same time last year.

Retail sales at furniture and home furnishing stores picked

up in March, according to the U.S. Census release of

preliminary estimates. In the first quarter of 2018,

furniture and home furnishing retail sales were 4.8%

higher than in the first quarter last year.

Year-to-date cabinetry sales through February 2018 were

down 0.6% according to participating manufacturers the

Kitchen Cabinet Manufacturers AssociationˇŻs monthly

Trend of Business Survey. For the year 2017, U.S. cabinet

manufacturers reported a 3% increase in sales.

US trade policy viewed negatively by consumers

Economic growth was strong in the first quarter with GDP

increasing 2.3%, according to the advance estimate

released by the Bureau of Economic Analysis. In the

fourth quarter of 2017, GDP increased 2.9%. The

unemployment rate was unchanged at 4.1% in March,

according to the U.S. Bureau of Labor Statistics

employment in manufacturing increased.

Consumer confidence was down slightly in April from the

previous month. The U.S. administrationˇŻs trade policy

and new duties were viewed as negative by the majority of

respondents in the University of Michigan Surveys of

Consumers.

Affordability and supply affect housing market

Multi-family housing construction drove the growth in

housing starts in March, according to the latest data

release by the U.S. Census Bureau and the U.S.

Department of Housing and Urban Development.

Total starts were 11% higher than in March 2017, at a

seasonally adjusted annual rate. Single-family starts fell in

March but the number of permits for new houses is high

and indicates future growth.

Existing-home sales grew for the second consecutive

month in March. While demand for homes is up in the

current economic environment, low supply and rising

home prices hold back many would-be buyers, according

to the National Association of Realtors.

Moulding and trim market

Engineered wood and plastic moulding and trim are

expected to gain market share in the U.S. over the next

four years, but wood will remain the main material.

Demand for wood moulding and trim is projected to

increase 3.7% annually to US$5.5 billion in 2022,

according to a new Freedonia market study (Moulding and

Trim in the US by Material, Product, Market and Region,

7th Edition).

Wood will account for more than half of all moulding and

trim sales in 2022, despite having the slowest growth rate

of all materials. Engineered wood and plastic will grow at

a faster rate because of cost and durability considerations.

New home construction and renovation, especially in

single-family houses, as well as non-residential

construction (office and institutional) will drive the growth

in moulding demand.

The main market for wood is in residential construction and

renovation, while commercial construction uses mostly

metal. Office and institutional buildings use a range of

materials for moulding and trim, including wood and

engineered wood.

EPA declares biomass energy carbon neutral

The federal Environmental Protection Agency (EPA) has

declared biomass from managed forests as carbon neutral

when burned for energy production.

The agency noted that the decision was not based on

scientific evidence or recommendations by the

independent Scientific Advisory Board, who was tasked in

2011 to establish a factor for carbon emissions from the

entire life cycle of biomass feedstocks for electricity

generation.

Forest industry groups such as the American Wood

Council have welcomed the announcement. At the same

time the effect on biomass energy use in the U.S. is

unclear because many states have their own policies on

biomass use for renewable energy.

Environmental groups have criticized the declaration

given the Science Advisory BoardˇŻs finding that not all

wood biomass is carbon neutral. The National Resources

Defense Council noted that the EPA and the federal

government lack jurisdiction over the regrowth of most

U.S. forests and therefore cannot guarantee that the

biomass grows back.

ITTO/EC IMM Report

Market role of EUTR and FLEGT licensing

A key question for the long-term future of the EU trade in

tropical timber products is the impact of the EU Timber

Regulation (EUTR).

This is particularly true of suppliers in those tropical

countries, like Indonesia, that have a Voluntary

Partnership Agreement (VPA) with the EU and are

seeking an assurance that FLEGT licensed timber will

benefit in the market from the ˇ°green laneˇ± offered by

EUTR.

FLEGT licensed and CITES certificated timber products

are the only products recognised by EUTR as requiring no

further checks by EU importers to ensure their legal status.

For those suppliers of tropical timber products that are not

FLEGT licensed, there are key issues surrounding the

types of information that the EU importers will accept as

assurance that there is a negligible risk of illegal harvest.

These issues have been highlighted in recent weeks by the

prosecution of one UK importer for a failure to comply

with EUTR in relation to sawnwood imported from

Cameroon. The prosecution was solely focused on the

companyˇŻs due diligence systems relating to its purchases

of FSC-certified ayous from Cameroon in January 2017.

Although the prosecution acknowledged that none of the

material imported was from an illegal source, the company

was found guilty of failing to adequately check the legality

of the timber when placing it on the market.

The company was fined £4000 in the second successful

EUTR prosecution in the UK. The first was last year when

a designer furniture retailer was fined £5000 for importing

a sideboard from India without carrying out the required

due diligence assessment.

Commenting on the latest prosecution, a representative of

the British Woodworking Federation said: ˇ°Companies

bringing timber products in directly from outside the EU

need to have their own due diligence system in place even

for one-off transactions and cannot rely on suppliers to

carry this out on their behalf.

ˇ°This must include information about the supply of timber

products, an evaluation of the risk of placing illegally

harvested timber and timber products on the market and

necessary steps to mitigate this risk; for example

additional information and third party verificationˇ±.

ˇ°Simply bringing in FSC, PEFC or similar Chain of

Custody certified timber is not enough to satisfy the due

diligence requirements for these importers, although

FLEGT licenced timber would suffice.ˇ±

In practice, given the extra due diligence steps required to

import even FSC certified timber into the EU market,

EUTR should offer significant market advantages to

tropical suppliers of FLEGT licensed timber.

At present that applies only to Indonesia, which has

licensed timber for the EU market since November 2016.

The latest data from the FLEGT Independent Market

Monitor, hosted by ITTO, suggests that this market

advantage may be filtering through into a rise in EU trade

with Indonesia for product groups like plywood and

decking that have been an immediate focus of EUTR

enforcement activity.

There has been quite a sharp increase in EU imports of

Indonesian plywood since November 2016, lending

support to anecdotal reports of EU plywood importers

being encouraged to stock more Indonesian product due to

licensing. EU imports of decking products from Indonesia

were sliding in the first half of 2017 but recovered in the

second half of the year.

However, it would be a mistake to attempt to attribute

these trends to a single cause, even one so significant as a

regulation applicable to every company placing timber on

the market in the EU. An increase in trade can be expected

in a year when the EU economy began to grow more

strongly after a long period of slow growth following the

European debt crises.

ItˇŻs also apparent that the rise in trade with Indonesia

during 2017 was not universal across product groups. EU

imports of wood furniture from Indonesia were flat during

the year, while imports of Indonesian flooring and glulam

declined.

See: http://www.flegtimm.eu/index.php/newsletter/flegt-marketnews/

54-eu-imports-from-indonesia-in-2017).

These trends seem to be confirming earlier forecasts in the

ITTO MIS (16-30 Sept 2016 & 16-30 April 2017) that the

combination of EUTR and FLEGT licensing offer an

immediate opportunity for Indonesian suppliers to retake

share in those sectors ¨C like decking and plywood - where

Indonesian products are familiar to EU importers and

already favoured for their strong technical performance,

but where demand has been dampened by concerns over

the legality of wood supply.

However, in isolation, FLEGT licensing is less likely to

generate immediate benefits in those high value sectors

like furniture and joinery where the specific technical and

environmental features of Indonesian wood products have

been less significant barriers to competitiveness than wider

issues such as labour costs, red tape, logistics, processing

efficiency, innovation, and marketing.

In these sectors, increasing share may well be achieved if

FLEGT licensing is combined with market development

initiatives to improve the international competitiveness of

Indonesian wood manufacturers across a wider range of

issues, although this is likely to take time.

ClientEarth: EUTR not ˇ°effective, proportionate and

dissuasiveˇ±

The potential value of FLEGT licensing is also partly

dependent on the extent to which EUTR is being

implemented consistently across the EU. This is a question

considered in a new report issued by ClientEarth, a UK

based NGO specialising in analysis of environmental law.

In the report, ClientEarth provide their assessment of

whether the enforcement regimes, which under EUTR are

required to be implemented by the individual EU member

countries, are ˇ°effective, proportionate and dissuasiveˇ±

according to the law.

The report highlights that although the EUTR was first

introduced in March 2013, some EU member countries

delayed introduction of a national enforcement regime for

some time after that date, although nearly all had done so

by the end of 2016.

ClientEarth show that penalties for EUTR infringements

vary widely across the EU. Certain Member States (such

as Austria, Poland, Romania and Bulgaria) have chosen a

penalty regime relying mainly on administrative penalties;

others (such as Denmark and the Netherlands) rely mainly

on criminal penalties for key EUTR obligations. Some

Member States (such as Belgium, Finland, France,

Germany and Italy) have adopted a combination of the two

systems.

EUTR penalties include notices of remedial actions,

seizure of timber, suspensions of authorisations to trade,

fines and imprisonment. ClientEarth conclude that

competent authorities and Member State courts have been

more actively enforcing the EUTR since 2016 compared

to the years 2013 to 2015 when almost no penalties had

been imposed.

ClientEarth summarise all the EUTR actions that have

been reported publicly to date referencing the two UK

cases mentioned earlier together with two cases in the

Netherlands, two cases in Sweden, and one in Germany.

In the Netherlands, a fine of €1,800 per cubic metre of

timber was imposed on a company for a failure to gather

information tracing back the entire supply chain of

imported sawn timber deemed to be risky from Cameroon.

In another case, a preventive measure was ordered against

two Dutch importers of Burmese teak, imposing a fine of

€20,000 per cubic metre for each teak shipment placed on

the market in breach of the EUTR.

In Sweden, the cases so far have all involved prosecutions

for a failure to undertake appropriate due diligence in

imports of Myanmar teak.

One company was fined SEK 17,000 (approximately

€1,700), another the much larger amount of SEK 800,000

(approximately €79,500) due to a failure to implement

measures stipulated in an earlier injunction.

In addition to these cases which led to fines, in 2017

several other Swedish companies were prohibited under

EUTR from importing any products containing Burmese

teak.

In Germany, an administrative court confirmed in 2017 a

decision by the competent authority taken in 2013 to

confiscate timber imported from the DR Congo due to

irregular documentation. The timber will be auctioned and

the money from the auction allocated to the federal

budget.

While these few cases have been brought in a limited

number of Member States, according to ClientEarth, 'soft'

approaches involving no punitive action and a mainly

educative purpose still seem to be the preferred

enforcement option in many Member States. Such

measures include advice letters and warnings, as well as

injunctions and notices of remedial action without noncompliance

penalties.

Based on this analysis of the cases brought date, the text of

laws introduced at national level, publicly available

information on regulatory checks and sanctions regimes,

and interviews with several competent authorities,

ClientEarth conclude that ˇ°EUTR penalties rarely seem

enforced to the 'effective, proportionate and dissuasive'

legal standard, even in Member States where a positive

trend in EUTR enforcement is noticeable.ˇ±

Comment on ClientEarth assessment of EUTR

The ClientEarth study has limitations. The conclusions are

based on a technical analysis of sanctions regimes -

considering, for example, whether the costs of sanctions

are likely to significantly exceed the costs of

implementing EUTR due diligence measures and therefore

to provide an effective deterrent.

There is no actual appraisal of whether the national

differences in sanctions regimes is leading to significant

failures in enforcement or other negative impacts, such as

diversion of illicit trade through countries with weaker

enforcement regimes.

It is notable that in none of the cases cited was it ever

proved that the wood was from an illegal source - there is

no obligation under EUTR on the EU authorities to

provide such proof - the prosecutions were all due to the

failure on the part of the importer to demonstrate

compliance to the due diligence steps required in EUTR.

The fact that these prosecutions were brought and led to

significant sanctions, even without evidence of illegality at

source, suggests that the law has teeth and places a

significant lever to encourage more far-reaching due

diligence measures in the hands of the EU authorities.

ItˇŻs the kind of regulatory power that needs to be used

wisely to avoid unintended consequences, such as the

creation of technical barriers to trade, feeding of

protectionist instincts and discrimination against smaller

operators.

ClientEarth acknowledge that their conclusions are based

on inadequate information, noting that there is relatively

little publicly available information about the number of

penalties that have been applied since the EUTR has been

in force. The EC has already indicated an intent to

improve transparency on this issue and much more

information is expected to be available later in the year.

ClientEarth is also critical of what it refers to as ˇ®softˇŻ

approaches, arguing that they do not provide an effective

deterrent to timber products from placing timber at risk of

being illegal on the EU market.

This is one interpretation, but in practice EUTR is a

complex and innovative law for which most national

authorities have had to acquire new knowledge and skills,

often from the private operators they are required to

regulate, many of which were implementing responsible

procurement policies for years even before EUTR was

introduced.

Regulating the purchasing decisions throughout 28

Member States of a fragmented industry with nearly half a

million enterprises, one in five of all manufacturing

enterprises in the region, is unprecedented. In the early

years of implementing EUTR, there has been some

confusion and ambiguity over the exact measures required

by individual operators to demonstrate conformance.

Communicating to timber operators, often small traders

with only limited access to legal advice, that they cannot

accept either FSC certificates or government documents at

face value as evidence of a ˇ°non-negligible risk of illegal

harvestˇ± takes time and effort.

It is challenging to explain to operators that it is their

responsibility to identify which products are ˇ°nonnegligible

riskˇ±, particularly when the EC and other

regulators cannot advise on the relative risks associated

with different supply countries and product groups. In

such a situation it would be unjust to rush to prosecution ¨C

and runs the risk of discrediting the legislation,

particularly amongst those operators being regulated.

The success of the EUTR to date has been built to a

significant extent on the active support of the private

sector within the EU. This support would quickly

evaporate if a perception arose that it was just being used

as a rod to beat the industry.

A lengthy period of ˇ°softˇ± regulation seems most

appropriate, at least until such time as guidelines and

supporting information sources have been properly

developed and communicated and the authorities are

sufficiently competent to accurately interpret and enforce

the law. However, there may be a distinction between

certain member states using ˇ°softˇ± measures as part of a

concerted effort to evolve an effective, efficient and

equitable regulatory program, and others that may be

hiding behind these measures to avoid more meaningful,

and potentially costly, action.

If the latter attitude is widespread it could have the

negative consequences mentioned by ClientEarth; an

unequal playing field for trade in the EU, undermining the

efforts of those operators that are conscientiously

implementing due diligence procedures, undermining

demand for FLEGT licensed timber, and encouraging

diversion of illicit trade through less regulated countries.

So far, the information gathered by ClientEarth is not

sufficient to judge the effectiveness of EUTR and their

conclusion that the law does not provide a reliable

deterrent to trading illegally harvested wood seems

premature.

A clearer picture will emerge only when the EU publishes

more comprehensive information on the regulatory

measures and sanctions introduced at national level in the

EU and with more detailed analysis of actual trade flow

trends and the compliance steps being taken by operators

across the EU.

The European Commission monitors impacts and

implementation of the EUTR and updates can be found in

ITTOˇŻs market reports and the IMM website

http://www.itto.int/imm/.

Readers can find the ClientEarth report here and make their own

judgement on this:

https://www.documents.clientearth.org/library/downloadinfo/

national-eutr-penalties-are-they-sufficiently-effectiveproportionate-

and-dissuasive/

|