|

Report from

Europe

Structural obstacles constrain market opportunities

There are significant new opportunities for the

international hardwood sector, particularly with the growth

of new markets in emerging countries and the

development of new products such as hardwood CLT, but

the industry continues to be held back by structural

obstacles and is struggling to cope with rapid global shifts

in trade and intense competition from substitute materials.

These were the major messages of the International

Hardwood Conference (IHC) held in Venice on 15-17

November. Organised in association with the European

Timber Trade Federation (ETTF) and European

Organisation of Sawmill Industries (EOS) by Italian trade

federation Fedecomlegno, part of FederlegnoArredo. The

event attracted a capacity audience of 150, drawn from 17

countries.

Fedecomlegno chairman, Alessandro Calcaterra, opened

with a portrayal of the wood industry at a critical point,

facing increasing and shifting global demand. ˇ°By 2030

global industrial roundwood consumption is set to rise

60%, making it ever more important where wood comes

from, how itˇŻs produced (FAO forecast one third will

come from plantations by then) and where itˇŻs used,ˇ± he

said.

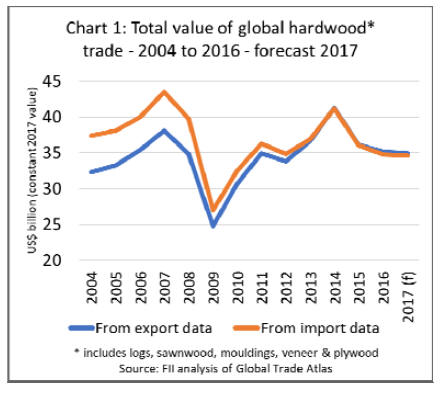

Value of global hardwood trade static at US$35 billion

In an overview of the global market position of hardwood,

analyst Rupert Oliver, of Forest Industries Intelligence,

said latest statistics indicated total international trade in

hardwood (including logs, sawnwood, mouldings, veneer

and plywood) was valued at US$35 billion in 2016, and

this level is projected to be maintained in 2017.

Considering the longer-term trend, Mr. Oliver said that

trade has been volatile in the last 15 years, declining

sharply during the financial crises in 2008 and 2009,

before rising to a peak in 2014, driven by demand in

emerging markets, particularly the speculative boom in

rosewood (hongmu) in China which receded in 2015.

(Chart 1).

Mr. Oliver highlighted, that underlying this volatility, is a

long-term lack of value growth. The total value of the

international hardwood trade in 2017 was no more than in

2004 despite, in the intervening period, the worldˇŻs

population increasing by more than 1 billion and 1.4

billion people being taken out of poverty.

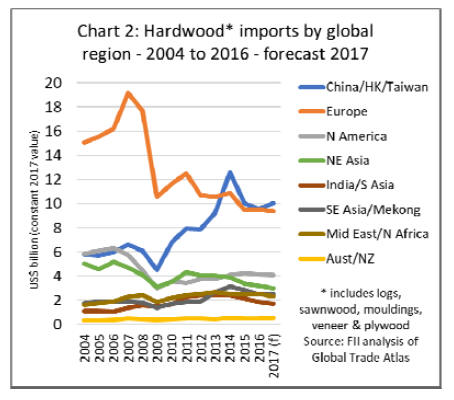

The overall stasis at global level obscures a significant

shift in in the balance of market influence away from

industrialised countries in Europe, North America and

North-East Asia to emerging markets, notably China.

Total hardwood imports by European countries declined

from a peak of USUS$19.2 billion in 2007 to a projected

level of USUS$9.4 billion this year.

During the same period, imports in North American

countries fell from USUS$5.8 billion to USUS$4.1 billion

and imports in North-East Asian countries fell from

USUS$4.7 billion to USUS$3.0 billion. In contrast,

imports increased from USUS$6.6 billion to USUS$10.0

billion in China and from USUS$1.9 billion to USUS$2.5

billion in South-East Asian countries (Chart 2).

Mr. Oliver said that India had been a hardwood log

consumer on the rise, but blocks on teak exports from

Myanmar and Malaysian supply issues had seen its

transition to more lumber buying.

But log imports by China, and to a lesser extent Vietnam

and other Asian hardwood product manufacturers,

continued their inexorable rise. In fact, Chinese imports hit

14.3 million metric tonnes in 2016, with 15.4 million

tonnes forecast for 2017.

In sawn hardwood, Mr. Oliver said total global temperate

trade was worth around US$6 billion in 2016 and tropical

US$4.5 billion, with the US the single leading exporter

and Thailand biggest tropical supplier. China again was

the consumer making the headlines with sawn hardwood

imports this year expected to be nine million tonnes, up

from 2016ˇŻs eight million and including around 1.5

million tonnes from the US alone.

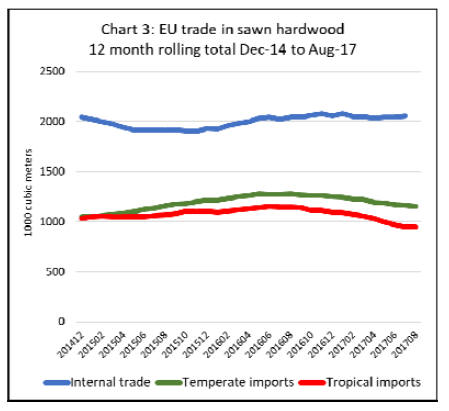

Focusing in on recent trends in the sawn hardwood trade

in the EU, Mr. Oliver showed that since 2014, internal

trade has remained flat at 2 million m3 per year, while

imports from outside the EU increased in 2015 and 2016,

but have been sliding again this year.

EU imports of temperate sawn hardwood increased from

1.05 million m3 in 2014, to 1.25 million m3 in 2016 and

are projected to fall to 1.15 million m3 this year. EU

imports of tropical sawn hardwood increased from 1.03

million m3 to 1.10 million m3 between 2014 and 2016,

but are projected to fall back to less than 950,000 m3 this

year. (Chart 3).

Mr Oliver concluded that the hardwood sector may

struggle near term to grow trade volumes, but had

opportunities to increase value. Difficulties to overcome

included over reliance on a few species, limitations of

current environmental controls to halt illegal trade and

industry fragmentation, which limited opportunities for

concerted promotion and investment.

But positives were revived interest among specifiers in

real wood as opposed to substitutes, development of

higher specification engineered and modified hardwood

products and emergence of more realistic risk-based

assurance of legality and sustainability. ˇ°Latest technology

can also better evaluate trade data and reduce

sustainability certification cost,ˇ± he said.

America's hardwood transition

At IHC, AHECˇŻs Executive Director Mike Snow

highlighted the dramatic transformation in the US

hardwood sector in the last 15 years. He explained that the

economic and construction crisis of the late 2000s and

before that US manufacturingˇŻs migration to lower labour

cost countries, saw sawn hardwood output in the US

slump. It has since recovered, but at 22.5 million cu.m in

2016, is still well below the peak level of around 30

million cu.m in 1999.

At the same time, reflecting the decline in domestic

construction and hardwood manufacturing demand, US

mills have refocused on industrial lumber for the US

market and graded lumber exports. ˇ°In 2005 grade lumber

accounted for 59.7% of US output, today thatˇŻs 48%,ˇ± said

Mr Snow. ˇ°Moreover, 45% of it is now exported and

rising, compared to 17% in 2000.ˇ±

ChinaˇŻs role in this evolution has been central, accounting

for all US sawn hardwood export growth since 1992, and

today buying 25% of the boards America produces. US

exports to China have grown particularly rapidly since the

international economic crisis, thanks to the potent

combination of contraction in the American domestic

market and the rise of ChinaˇŻs new middle class, firing

growth in its domestic consumption.

ˇ°In 2000 85% of our exports to China were re-exported as

finished goods,ˇ± said Mr Snow. ˇ°Today 80% goes into

products for its domestic market.ˇ± Asked which country

will be the ˇ°next Chinaˇ±.

Mr SnowˇŻs response was ˇ°still Chinaˇ± thanks to

accelerating development of its less industrialised western

regions. US mills see this as a further lumber market

opportunity; however, their growing concern is the

accompanying rise in ChinaˇŻs log imports.

ˇ°So far logs have gone mainly to finished goods makers

processing timber for their requirements,ˇ± said Mr Snow.

ˇ°The concern now is emergence of Chinese mills cutting

US logs for the general market.ˇ±

Mr Snow suggested that, despite IndiaˇŻs vast population

and a widening gap in wood supply, opportunities to

expand sales of sawn hardwood in India are unlikely to

match those in China, at least in the near term, because the

country is not pursuing investment in manufacturing ¨C or

in infrastructure ¨C and is focused instead on developing a

service economy. However, India is now developing as an

important market for hardwood furniture made elsewhere,

notably in China and Vietnam.

Questioned about the impact of the persistently strong

dollar on US hardwood exports, Mr Snow said that while

it will act as a temporary drag, in practice it has not

prevented US hardwood exports reaching record levels. It

also increases US consumer demand for finished products,

including hardwood furniture.

Mr. Snow suggested that, based on current economic

conditions, there is unlikely to be any significant

weakening of the US dollar in the near term.

Africa expected to become a net wood importer

Another perspective on the global hardwood trade was

provided at the IHC by consultant Pierre Marie Desclos

who suggested that population growth will accelerate

regionalisation and sharpen the focus on raw material

supply and logistics.

Mr. Desclos said that the hardwood resource in many

tropical regions and some temperate countries is becoming

depleted and that climate change may accelerate this trend.

He also noted that, according to UN estimates, world

population is projected to rise from 7.3 billion today to 9.7

billion by 2050, adding 80 million more inhabitants every

year, with longer life expectancy and higher buying

power.

Mr Desclos suggested this would likely result in a critical

increase in hardwood demand and changing relationship

between buyers and consumers.

Due to particularly rapid population growth, and limited

productive forest resources, Mr. Desclos suggested that

changes would be dramatic in Africa which would soon be

transformed from a significant exporter into a net importer

of wood products.

While population growth is expected to moderate in other

regions, in Africa it is expected to accelerate. Mr. Desclos

said that before the end of this century, one third of the

worldˇŻs population will be in Africa.

In 2050, Nigeria will be the worldˇŻs third most populous

nation, ahead of the US. African forests, which account for

only 15% of the worldˇŻs total forest area, will need to

focus on supplying domestic needs.

ETTF view of European hardwood market situation

ETTF President Andreas von Möller provided an overview

of the current state of the European hardwood market to

the IHC. He described the contraction of EuropeˇŻs tropical

wood imports in recent years as ˇ®sadˇŻ and due both to the

recession and to specifier misperceptionsˇŻ around the

materialˇŻs legal and sustainable credentials.

However, Mr von Möller, added that European market

prospects are generally positive, with most countriesˇŻ GDP

and construction sectors trending up. He noted that the

EUˇŻs construction production index had risen 5% since the

start of 2016 and made the following observations

regarding individual European markets:

The economy in Germany has been resilient in recent

years and is now benefitting from improving economic

conditions in neighbouring countries. Demand for wood

woods in the first half of 2017 was very good, particularly

for flooring and garden furniture.

Expectations are that the market will remain strong in

2018, with 30% of members of the German importing

association predicting that demand will be even better than

in 2017.

In the UK, the Brexit decision to leave the EU in March

2019 has created economic uncertainty and, together with

the weaker GBP, is leading to inflation and reduced

borrowing, business investment and consumer demand for

home improvement.

Nevertheless, the UK economy continues to expand, with

GDP growth projected to be 1.5% in 2017 and 1.4% in

2018. Modest new housing growth of around 0.5% is

expected in 2018.

The British Woodworking FederationˇŻs latest trade survey

for Q3 2017 indicates that medium term prospects of the

joinery industry remain sound. There are rising concerns

over skill shortages and rising raw material costs, but

many manufacturers expect sales to improve in the final

quarter of the year.

After a long and deep recession, the economy in Italy is

beginning to recover, with construction performing better

than expected this year. Hardwood stock levels in the

country are low and delivery times are now extended

which is feeding through into rising prices.

The wood sector in Belgium reported positive turnover

development in 2016 and the first half of 2017. Market

share of wood in new housing is rising rapidly, from 6% in

2011 to 9% in 2016, but this is benefitting softwood more

than hardwood. Outlook for wood demand in 2018 is

considered positive.

The Netherlands economy is recovering, recording 3.4%

growth in the second quarter of 2017 and 3.2% growth

forecast for 2017 and 2.4% in 2018. Over 55,000 housing

permits are expected to be issued in 2017, double the level

of 2013, although still some way below pre-crises levels.

France, a large market for wood products, is recovering

with building activity now rising to close to pre-crisis

levels. However, the unemployment rate is still high, at

around 10% for the last three years, and tropical wood has

yet to see any benefit from growth in the wider economy.

SpainˇŻs economy is reviving following the financial crises

with construction activity increasing consistently in the

last two years, much of focus now being in large urban

areas rather in coastal holiday towns and rural areas.

However, finance for construction is still difficult and

recent political events in Catalonia, which accounts for

about 20% of national economy, has created uncertainty

about market prospects in 2018.

Greece has been 9 years in recession and national GDP

this year will be 30% less than in 2008. Construction

activity is nearly 90% down compared to 2005.

Nearly one in four Greeks of working age are

unemployed. Construction and other business activity is

impaired by extremely high interest rates. Nevertheless,

the wood sector expects the downturn to hit bottom this

year and for recovery to start next year.

The economy in Denmark, which is a big per capita

consumer of wood, is expected to grow 1.7% this year and

the construction sector is performing well. EUTR

enforcement is very active in the country and creating

much confusion in the importing sector and tending to

hinder imports, particularly from the tropics.

European sawmills report static hardwood production

The European domestic hardwood supply situation was

summarised at IHC by EOS Board Member Nicolae

Tucunel.

He reported that European annual sawn hardwood

production has remained static at around 10.9 million m3

in the last three years despite the gradual economic

recovery. Lack of raw material was highlighted as a

problem in Germany, France and Belgium, where about

30% of hardwood sawmills across the three countries have

been closed in the last decade.

Mr Tucunel said that that supply problems this year have

become particularly pronounced in Romania, where

production is constrained both by declining log harvests

and lack of finance for investment in wood processing,

and in Croatia where the government implemented a ban

on exports of oak logs and lumber over 20% moisture

content, ostensibly for phytosanitary reasons.

EU exports of hardwood logs to China have also been high

this year, at 1.47 million tonnes in the first nine months,

10% more than the same period in 2016, with around 50%

comprising oak. As in North America, the level of log

exports to China is now creating concern in the European

hardwood processing sector.

ˇ°We must insist on a level timber market playing field,ˇ±

said EOS President Sampsa Auvinen, ˇ°without raw

material the European sawmill industry will be forced out

of the market.ˇ±

Role of EUTR in trade diversion away from Europe

Raw material availability and distribution also formed a

core theme for Davide Pettenella of Padua University. He

addressed whether national and regional timber legality

controls were creating a ˇ®dual marketˇŻ for tropical timber.

His study compared trends in primary tropical timber

product imports by EU states, the USA and Australia,

representing developed countries with strict timber market

legality regulation, and China, Vietnam and India

representing emerging consumers with lighter controls.

This highlighted import swings to the latter. In 2001 of all

tropical timber imported by these countries, the developed

economies accounted for 63% and 72% by volume and

value, the emerging countries 37% and 28%. Today the

respective division is 44% and 47% and 56% and 53%.

While legality controls may be implicated in this trend, Mr

Pettenella said it was not the exclusive factor. ˇ°Emerging

countriesˇŻ economic development and increasing southsouth

trade are also involved,ˇ± he said.

In fact, his conclusion was that monitoring should focus

more on these emerging market trends. ˇ°ItˇŻs a

phenomenon which should be of interest to policy

makers,ˇ± said Mr Pettenella. ˇ°In 1990, there were just 20

regional trade agreements. Today there are 283.ˇ±

Innovation to expand opportunities for hardwood

Turning to hardwood use, European Director David

Venables described AHECˇŻs work supporting application

of hardwood species in engineered and thermally modified

form in construction. Mr Venables observed that there is a

new generation of timber towers being built which are

rising ever higher, a development made possible by glulam

and Cross Laminated Timber (CLT).

Engineers now believe that the maximum possible height

of a CLT tower is only around 11 storeys but that hybrid

towers, for example comprising a concrete core with a

CLT shell, can extend up to 22 storeys.

Mr Venables said that interest in using engineered wood

for high density urban construction is driven mainly by

cost-savings and reduced time of construction.

The BskyB building, the tallest commercial timber

structure in the UK, was designed and constructed in less

than one year, half the normal time of a project this size.

The building weighs considerably less than an equivalent

concrete building, therefore greatly reducing the costs and

time required for delivery of materials on-site.

AHECˇŻs own work has focused on promoting the use of

American hardwood for manufacture of specialist grades

of CLT and glulam. ˇ°CLT production is forecast to reach 1

million m3 next year,ˇ± said Mr Venables. ˇ°softwood

dominates the market, but imagine if hardwood took just a

percentage.ˇ±

This work is drawing on experience acquired during

AHECˇŻs high profile showcase projects at the London

Design Festival ¨C the Endless Stair and The Smile ¨C where

engineers and architects were commissioned to utilise

experimental tulipwood CLT panels. Testing for these

projects demonstrated that tulipwood CLT panels were

three times stronger than spruce panels of equivalent size

and weight.

The demonstration projects led directly to the first

permanent use of hardwood CLT at a ˇ°Maggies Centreˇ± in

Oldham in north England.

The panels for the project comprised the lowest grades of

tulipwood, the natural wood fully on display using a

hardwood previously considered suitable only for paint

grade.

Tulipwood was chosen not only for its strength and

aesthetic, but also because of the health benefits of an

untreated natural material, a factor particularly important

for a structure designed for the treatment of cancersufferers.

The exterior panels were thermally modified to

enhance durability.

In another major project, Mr Venables reported that

American white oak was used for the 22-meter, 4-tonne,

glulam structural beams installed as the core roof structure

of the new stand at Lords cricket ground in London. White

oak was chosen for these, the longest cantilevered beams

in the world, because of the extremely high strength to

weight ratio of the hardwood.

Mr Venables said that, while CLT and glulam offer

opportunities to extend applications of hardwood, there are

challenges. One issue is that manufacturers only purchase

square-edged fixed-width timber which is often not

supplied as standard in the hardwood industry, unlike the

softwood sector which is more accustomed to supply large

volumes in fixed dimensions.

Another problem is that the technical standards bodies are

dominated by softwood interests and need to be persuaded

to approve hardwoods for use in structural panels.

Mr. Venables said AHEC has been forging links with the

relevant Eurocodes committees who now appear to be

more open to the idea of extending the standards to

include hardwood species.

This is less because of AHECˇŻs direct lobbying of

committee members, and more because architects and

engineers now recognise the potential of hardwood and are

themselves demanding that the relevant standards be

changed.

|