Japan

Wood Products Prices

Dollar Exchange Rates of 10th

April 2017

Japan Yen 110.94

Reports From Japan

Falling unemployment and low inflation

boosts

consumer confidence

According to the Cabinet Office, consumer confidence in

Japan improved more than expected in March rising to a

three year high. All components of the consumer

confidence index trended higher with the indexes for

income growth, employment, the willingness to buy

durable goods and the measure for overall livelihood

rising surprisingly sharply.

The boost in consumer confidence stems partly from the

decline in unemployment and because inflation is minimal

which means households feel there disposable income is

stable. The main downside to an even bigger boost to

consumer confidence is the poor wage growth after the

latest round of wage negotiations with the unions.

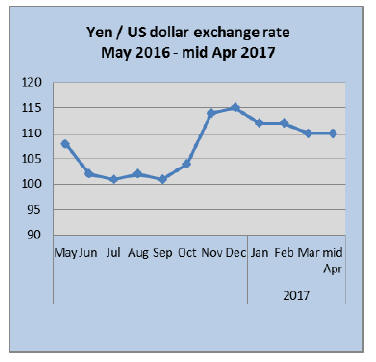

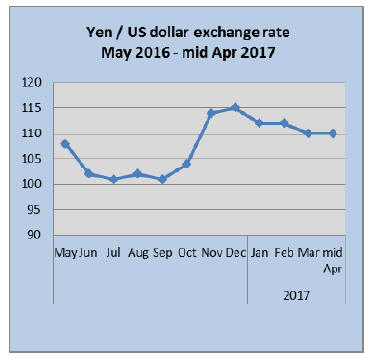

Yen swings higher again

The yen barely moved from 110 to the US dollar in the

first two weeks of April and still hovers at a four month

high against the dollar.

Uncertainty in the US and regional tensions have

driven

investors back to the safe haven Yen. The stronger Yen

will boost importer sentiment and will work to suppress

inflation because of its impact in lower energy costs.

Home renovation statistics would improve

understanding of housing market trends

The stock of old houses in Japan, many of which have

been left untended, is of concern to the authorities as these

houses could eventually become unsafe. The government

has brought in legislation which encourages owners of

homes no longer occupied to either sell or demolish but

selling an old home in Japan is no easy task.

In recent years the concept of house reform (renovation)

has gained ground driven partly by the interest from

middle income earners to own a home.

Most of the old homes on the market were built in

the

1980s but were not built to last, commonly in Japan,

homeowners assume they will have to replace their house

after 30-40 years which tends to lead to minimal

maintenance.

Against this background the new trend in ˇ®reformˇŻ is

creating opportunities but has exposed some problems, the

main one being the absence of consistent regulatory

supervision.

Unlike construction companies, a ˇ®reformˇŻ company can

open without registration which means anyone can start a

reform business and is under no obligation to report

customer spending on remodeling. This diminishes to

value of statistics on the housing market as only new build

data is available.

Exhibition exploring Japanese domestic architecture

The Barbican Centre, a performing arts and exhibition

centre in London, is one of the largest of its kind in Europe

and is currently exhibiting Japanese architecture.

The Barbican website has details of its exhibition ˇ®the

Japanese houseˇŻ which the Barbican says ˇ°is the UKˇŻs first

major exhibition exploring Japanese domestic architecture

from the end of the Second World War, a period which

has consistently produced some of the most influential and

ground-breaking examples of modern and contemporary

design.

In the wake of the war, the widespread devastation of

Tokyo and other Japanese cities brought an urgent need

for new housing and the single family house became the

foremost site for architectural experimentation and debate.

Since then, Japanese architects have used their designs to

propose radical critiques of society and innovative

solutions to changing lifestyles.ˇ±

See:

https://www.barbican.org.uk/artgallery/eventdetail.

asp?ID=19951

Import round up

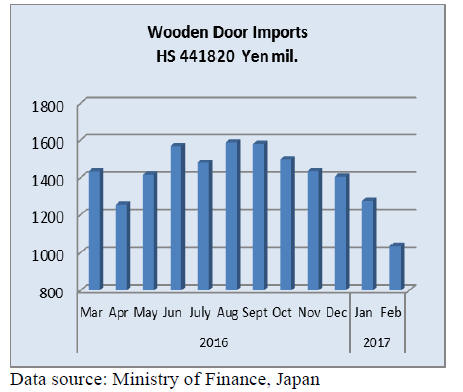

Doors

Year on year JapanˇŻs February 2017 imports of wooden

doors (HS 441820) were down once again, this time

falling 32% compared to February 2016 and from a month

earlier they were down around 19%.

The continuing downward trend in wooden door imports

marks five consecutive monthly declines since September

2016. The level of February imports is an unprecedented

low.

The top suppliers in February in order of rank were China

(46%), the Philippines (24%), Indonesia (13%) and

Malaysia (6%) accounting for 89% of JapanˇŻs wooden

door imports for the month.

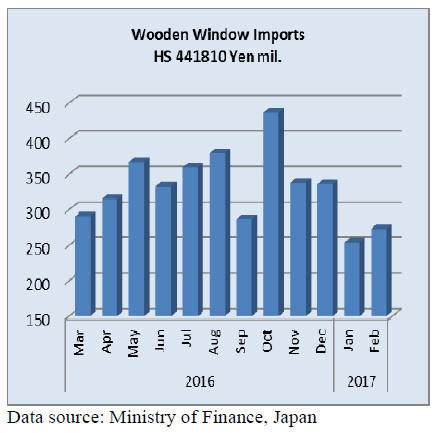

Windows

Year on year, JapanˇŻs wooden window (HS441810)

imports fell 7% but February 2017 imports rose 7%

compared to levels reported for January 2017.

Four shippers accounted for almost 80% of JapanˇŻs

February 2017 wooden window imports led by the US

(42%), China (19%) and the Philippines (18%).

The balance of February 2017 imports came from EU

member countries with Italy and Sweden together

accounting for 18% of the value of windows shipped.

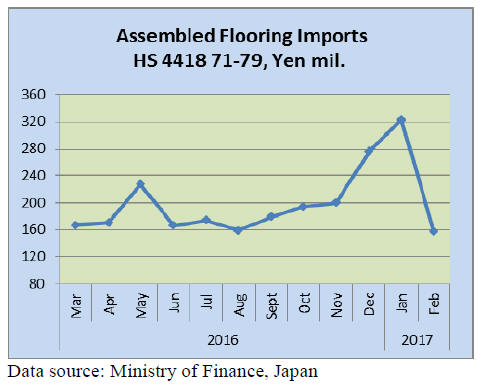

Assembled flooring

Three categories of assembled flooring are included in the

data presented below, HS 441871, 72 and 79.

There was a massive correction in JapanˇŻs imports of

assembled flooring in February 2017 with the value of

imports falling over 50%.

Assembled flooring imports had been rising since August

2016 and there was an unexpected burst in imports in

December last year followed by another surge in January

this year. Against the backdrop of a weaker yen making

imports more expensive the sudden rise is difficult to

explain.

The top assembled flooring suppliers to Japan in

February

2017 were Indonesia (37%), China (28%) and Sweden

(15%).

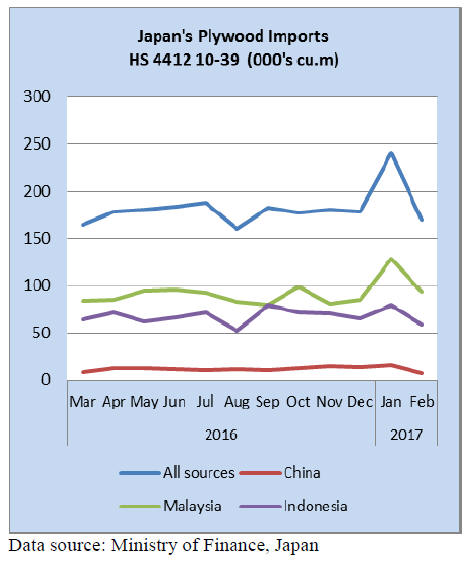

Plywood

The figure below shows the trend in imports of 4

categories of plywood, HS 441210/31/32 and 39.

Throughout 2016, as was the case in 2015, almost 90% of

JapanˇŻs plywood imports are from Malaysia, Indonesia

and China.

This trend continued into February this year. Most

of

JapanˇŻs plywood imports are within HS 441231 (87%).

Year on year February 2017 shipments of plywood from

China fell 25% and shipments from Indonesia also

dropped (-17%). On the other hand, February shipments

from Malaysia increased 15%.

While Malaysian shippers managed a year on year

increase imports from all three of the major suppliers

Malaysia, Indonesia and China in February 2017 were

well below levels in January.

China posted the steepest decline with February

shipments

to Japan dropping 53%. Shipments from Malaysia and

Indonesia were down 28% and 26% respectively.

Trade news from the Japan Lumber Reports (JLR)

For the JLR report please see:

http://www.nmokuzai.

com/modules/general/index.php?id=7

Questions and answers on the Clean Wood law

The Clean Wood Act will be effective since May 20 this

year. Please refer to the article of Clean Wood Act in No.

693 dated March 10, 2017.

Registration of business will not start until this

fall so

there is ample time but it is necessary to register when

delivery of legally proven wood products is requested.

With this Act what would change and what one has to do

to deal with this Act.

Question : Is there any penalty for violation of the Act?

Since the Clean Wood Act is promotion law so there is no

legal penalty. If one handles suspicious wood products and

they are found illegally harvested wood later, there will

not be any penalty. However, if one handles the products

knowing they are illegally harvested wood, there are

possibilities of inspection, having guiding advice.

If one acts maliciously, registration will be cancelled and

the name will be publicised.

Question : What does the Act specify ˇ®woodˇŻ ?

It covers wide range of products from logs, lumber,

plywood, building materials, furniture and paper.

In these, there will be a certain standard how much wood

is used for furniture. If wood use is less than the standard,

it is not subject of the law. If products are mainly made of

recycled wood like MDF, OSB and particleboard, they are

not the subject.

Products like concrete forming panel, scaffolding and

sheet pile, which are used only at construction site are not

subject but raw materials to make such products

like plywood and lumber need to be proved legality.

Question : What does ˇ®confirmation of legalityˇŻ mean ?

Present methods to prove legality are forest certifications

like FSC, PEFC and SGEC, group certification by

industrial group and individual certification system like

major paper manufacturing companies have then local

products certification by prefecture.

Forest certification is sufficient by itself. Items mentioned

on statement of delivery of Group certification may be

changed or harvest registration may be requested to attach.

On imported wood products, it is necessary to have

statement to verify that the product is conformed to legal

system of producing countries.

If such certification is not available, secondary

certification such as EU wood rules or Lacey Act of the

United States may be used.

Question : If legality of wood product is not proved, is

handling such product prohibited ?

Even with hard effort, if legality is not proved, such

product can be handle3d separate from legally proven

products. Purpose of the Act is to keep reducing such

products little by little.

Question : What is difference between certified enterprise

by group certification and registered enterprises by the

Clean Wood Act ?

Group certification is a mean to confirm legality and

registered enterprises are entitled to use this method.

Means of confirming legality are various like prefectural

certification.

Registered enterprises confirm legality by forest

certifications and group certification and declare to handle

such products actively.

Once one becomes registered enterprise, it does not mean

that one cancels group certification since registration does

not mean to have means of proving legality.

Question : Who are wood related enterprises ?

There are two kinds. First group is ones which receive

wood initially such as importers, which receive logs or

lumber from overseas suppliers and log auction markets,

which receive logs direct from log harvesters. Then there

is second group, which received wood from first group

such as wood processor, wood distributor and final use of

wood like house builders.

Lumber mills, plywood mills and wood chip mills, which

receive wood directly from log suppliers are classified as

the first group but if logs are supplied through auction

market, it is the second group.

Timber owners, log suppliers, overseas wood products

suppliers, DIY stores and retailers are not subject of the

Act.

Plywood production in February

New orders for softwood plywood by major precutting

plants are slowing down now but there is no cancellation

for delayed deliveries. Since total inventories are low,

users fell uneasiness of future deliveries.

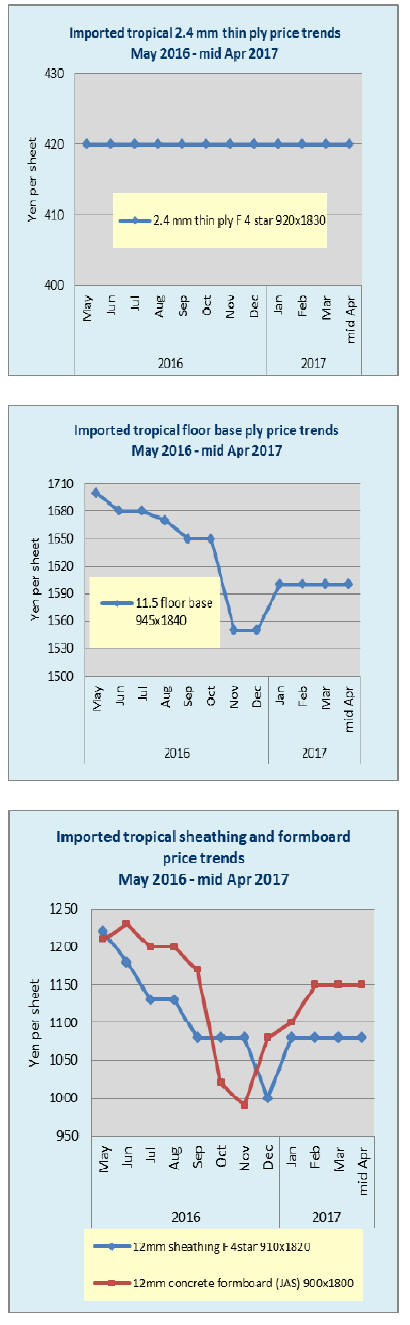

Import plywood market is slightly firming on structural

and green concrete forming panels but the prices of coated

plywood are weakening and there are some spot low

prices.

Production of domestic softwood plywood in February

was 234,000 cbm, 0.8% less than February last year and

2.7% more than January. In this, structural panel

production was 224,500 cbm, 0.6% less and 3.0% more.

Meantime, shipment of softwood plywood was 231,600

cbm, 0.9% less and1.4% less.

The production exceeded the shipment for the first time in

eight months so the inventories were 78,900 cbm, 2,400

cbm increase from January. The supply had been tight

since last April then deliveries are much quicker since

March but softwood inventories are only for one week

consumption so once orders increase from precutting

plants, the supply would get tight in no time.

Plywood mills continue full production

Import plywood supply in February was 206,400 cbm,

5.7% less and 33.1% less. It was nearly 100,000 cbm less

than January.

By source, 65,600 cbm from Malaysia, 14.2% more and

27.6 % less. 65,600 cbm from Indonesia, 15.1% less and

25.9% less. 32,500 cbm from China, 22.2% less and

52.9% less.

Actually, January arrivals were high with over 300,000

cbm by orders placed in late fall, which arrived in

December, then carried over volume from December by

the customs clearance delay is registered in January.

The market of imported plywood in Japan continues weak

with sluggish demand for coated concrete forming panels.

Review of plywood and panel market of 2016

Total supply of wood panel in 2016 was 8,795,762 cbm,

3% more than 2015. Majority of about 260 M cbm

increase was plywood. Domestic plywood production

exceeded three million cbm, the highest since 2007.

Softwood plywood marked record high of 2,897,218 cbm,

11.9% more than 2015.

Housing starts in 2016 were 967,237 units, 6.4% more

than 2015. In particular, wood based units were 546,336

units, 8.3% more. This stimulated demand for plywood

and other panels. Imported plywood volume was

2,770,650 cbm, 4% or 115,000 cbm less than 2015, the

lowest since 1990. Wooden panels like particleboard,

MDF and OSB increased slightly.

Domestic plywood alone increased significantly. Domestic

plywood production in 2013 was 2,810 M cbm when

housing starts were more than 2016. Structural plywood

production in 2013 was about 2,450,000 cbm then it

increased to 2,800,000 cbm in 2016.

An average production during 2013 and 2015 was about

2,430,000 cbm so the increase in 2016 was about 400 M

cbm. Structural plywood production maintained level of

2013 even when housing starts dropped from about

980,000 units in 2013 to about 900,000 units in 2014 and

2015.

Meantime, import plywood peaked in 2013 and the

volume dropped by about 150,000 cbm in 2014 and about

600,000 cbm in 2015. To fill short supply of imported

plywood, domestic plywood production increased.

Domestic panel was 4,958,058 cbm, 7% more then

imported panel was 3,837,740 cbm, 2% less. Therefore,

share of domestic was 56.4% and import 43.6%. Domestic

panel increased by 324,665 cbm. Besides plywood, MDF

increased by 222,000 cbm and particleboard by about 20

,000 cbm.

Imported panel volume dropped by about 80,000 cbm,

three consecutive yearsˇŻ decline. The largest factor is

decline of imported plywood, which was down by 115,000

cbm in 2016 from 2015. Imported MDF increased by

7,500 cbm and particleboard also increased by 21,000

cbm. Majority of the increase is OSB.

Market of imported plywood mainly concrete forming

panels remained sluggish then the market turned round in

third quarter finally bu t the demand remained weak so the

import was held down all through the year. As a result,

Malaysian plywood import was the lowest at 1,075,700

cbm since the peak year of 2006.

Despite reduced import, the market prices continued

decreasing with weak demand. Irritated with prolonging

depressed market in Japan, Malaysian plywood mills

decided to reduce the supply volume for Japan uniformly

in August until Japan market recovers.

High export prices became chronic since availability

of

quality logs becomes hard and transportation cost climbs

as harvest areas are farther and farther.

The Sarawak government put tight control on illegal log

harvest and tighten log export quota.so log availability

gets less and less and the prices continue climb. There

seems to be any chance of increasing log supply in

Sarawak. Sarawak plywood suppliers proposed higher

prices and at the same time, the yen started skidding so the

import yen cost increased, which discouraged purchase by

the Japanese importers.

Indonesian import was 903,300 cbm, 44,300 cbm more

than 2015. Indonesian plywood mainly used for floor base

as compared to MalaysianˇŻs concrete forming panel. The

prices of Indonesian plywood dropped some in Japan

market but not as much as Malaysian plywood.

Japanese softwood plywood mills are now trying to take

over floor base market so the mills are manufacturing new

product apart from traditional structural panel. Some mills

are now manufacturing softwood plywood for concrete

forming to compete with Malaysian plywood.

|