Japan Wood Products

Prices

Dollar Exchange Rates of

25th September 2015

Japan Yen 120.59

Reports From Japan

¡¡

More stimulus likely as consumer prices fall

Consumer prices in Japan fell in August marking the first

decline since the Bank of Japan (BoJ) began its economic

stimulus efforts two years ago. This data comes at a time

when other indicators suggest the BoJ efforts have been

undermined by falling oil prices and the slowdown in

exports especially to China.

On the face of it more quantitative easing appears likely

but some in the Cabinet are reluctant to approve further

stimulus as this could drive the yen lower against the US

dollar and add to the problems of small companies which

rely on imported raw materials.

New housing policy being developed

A panel at the Land, Infrastructure, Transport and Tourism

Ministry is working to revise the Basic Housing Plan ¡ª

which sets the direction of housing policies for the next 10

years to take account the decline in the nation¡®s

population, the pace of which will accelerate in the 2020s.

Unless the supply of new houses is adjusted, the problem

of vacant houses will no doubt become even more serious.

A recent estimate by Nomura Research Institute shows

that the number of vacant houses could reach 13.9 million

in 2023.

Previous housing policies have encouraged construction of

new houses and investment in housing accounts for around

4% of GDP. Building some new houses will be necessary

to replace old structures but a continuation of policies that

spur house building will eventually exacerbate the vacant

housing problem in Japan.

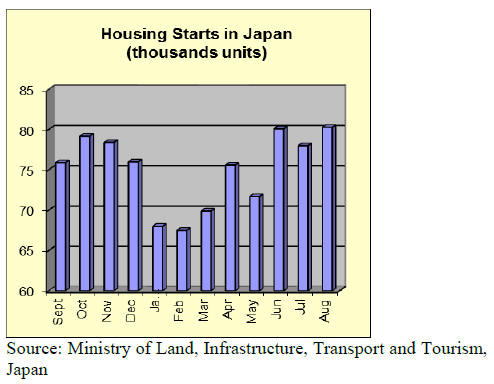

August housing starts followed the trend for the past six

months by rising against levels in the same period last

year.

Housing starts increased nearly 9% in August compared to

August 2014. The August figure lifts projections of

annual starts to 931,000. Despite the positive picture on

starts, the level of orders for new construction received by

the largest house builders dropped sharply in August.

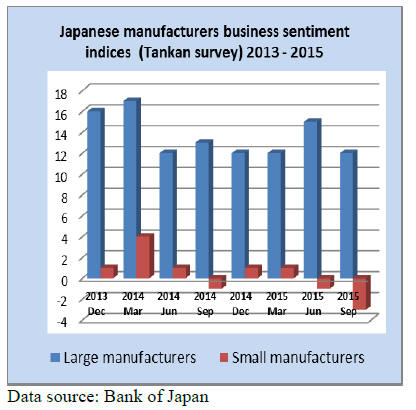

Tankan survey for September

The results of the latest business survey (Tankan) shows

that confidence amongst both large and small Japanese

manufacturers turned negative for the first time in three

quarters. Analysts are now forecasting another round of

monetary easing will be announced by the Bank of Japan.

For the full data see:

https://www.boj.or.jp/en/statistics/tk/gaiyo/2011/index.ht

m/

Japan at centre of TPP talks

Negotiations on the Trans-Pacific Partnership (TPP)

continue with both the US and Japanese governments

determined to reach an accord. The TPP if agreement can

be reached will create the world¡®s largest free-trade pact.

Negotiating countries include: Australia, Brunei, Canada,

Chile, Japan, Malaysia, Mexico, New Zealand, Peru,

Singapore, the United States and Vietnam which together

account for about 40% of global trade.

The Peterson Institute for International Economics in the

US has estimated that over the next decade the TPP could

add almost US$300 billion in annual global trade with SE

Asian countries participating in the negotiations set to

benefit hugely as tariffs on their exports , including those

on wood products, are dismantled.

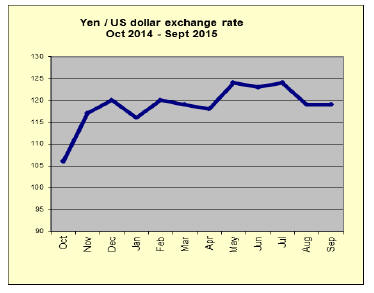

Yen strength of concern to exporters

In late September the yen strengthened against major

currencies drive higher by concerns that slowing Chinese

growth will ripple through the global economy. The

strengthening of the yen was also affected by dealers

buying yen as a safe-haven in the current unsettled

situation.

The firming yen is not good news for Japanese exporters

and analysts foresee further upward pressure on the yen.

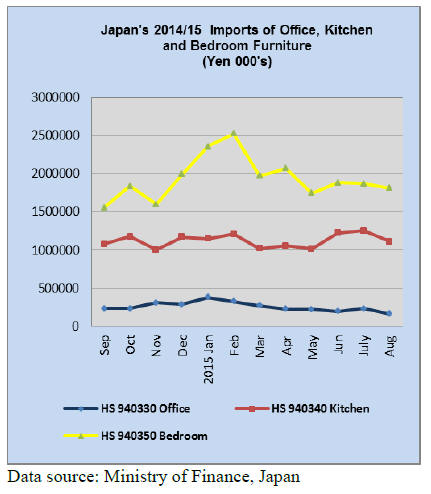

Japan¡¯s furniture imports

Japan¡®s imports of office, Kitchen and bedroom furniture

fell in August. Office furniture imports have shown a

steady decline since the beginning of the year.

The dip in kitchen and bedroom furniture came as a

surprise as housing starts, while weakening, have not

shown a sharp decline.

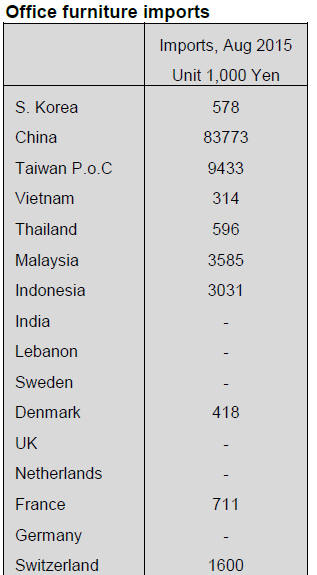

Office furniture imports (HS 940330)

August imports of office furniture fell sharply dropping

26% from July and year on year August 2015 office

furniture imports were down a massive 42%.

The top three suppliers in August were China, Italy (the

new comer), Portugal and Taiwan another new comer to

the top league of suppliers.

Office furniture imports from China were down 24% in

August while imports from Italy tripled. Portugal¡®s supply

of office furniture declined in August compared to a

month earlier. Unlike imports of kitchen and bedroom

furniture, SE Asian suppliers do not feature significantly

in the office furniture market in Japan.

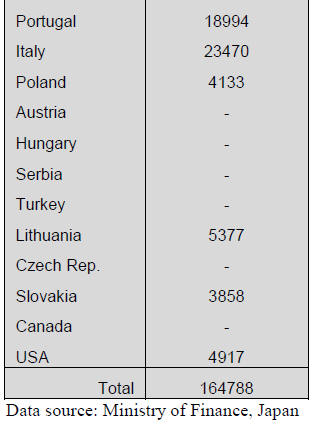

Kitchen furniture imports (HS 940340)

The top three suppliers of kitchen furniture to the Japanese

market (Vietnam. Philippines and China) account for

around 85% of all wooden kitchen furniture imports.

Vietnam is the largest supplier and in August the value of

exports to Japan was only slightly higher than in July.

On the other hand both Philippines and China saw their

share of kitchen furniture shipments to japan decline

compared to levels in July.

August figures show a 27% rise in imports of kitchen

furniture from Germany in sharp contrast to the 60%

decline for Indonesia. SE Asian suppliers of kitchen

furniture to japan account for 77% of total kitchen

furniture imports

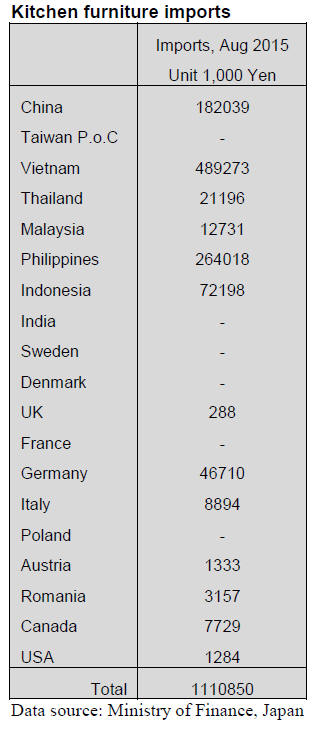

Bedroom furniture imports (HS 940350)

Japan¡®s wooden bedroom furniture imports (HS 940350)

in July were disappointing low and the downward trend

continued into August although the pace of decline has

slowed.

Two countries, China and Vietnam account for around

84% of Japan¡®s bedroom furniture imports but, unlike the

situation for office and kitchen furniture, SE Asia

suppliers (buoyed by the huge supply from Vietnam)

enjoyed a 32% share of Japan¡®s August bedroom furniture

imports.

Year on year August 2015 imports of bedroom furniture

by Japan rose around 9%.

Trade news from the Japan Lumber Reports (JLR)

For the JLR report please see:

http://www.nmokuzai.

com/modules/general/index.php?id=7

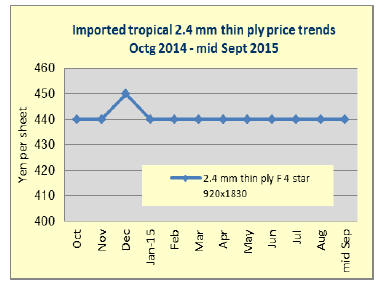

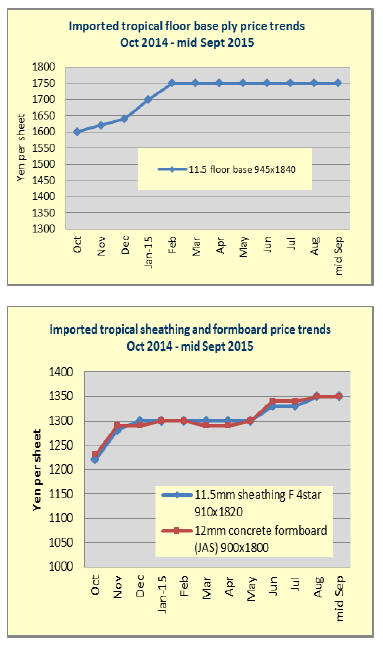

Plywood supply

Domestic production has been curtailed then the volume

of imports declined. The most noticeable change in

imports is Indonesian volume exceeded Malaysian

volume. Total imports were 232,900 cbms first time to

exceed 210,000 cbms after three months.

Malaysian volume has been declining for the last six

months and Indonesian volume surpassed for the first time

in about four years since October 2011. Malaysian volume

in July was 27.7% less than July last year, the lowest since

October 2011. This does not mean demand has shifted to

Indonesia from Malaysia. Seven months total from

Indonesia was 18.2% less than 2014.

Overwhelming share of Malaysian supply is now changing

in supply structure. Decline in Malaysian supply is partly

because of tightened log supply but sluggishness of

Japanese market is another large reason. Supply from

China continues low with seven month total of 390,000

cbms, 18.1% less.

Domestic production in July was 215,400 cbms, 5.5% less

out of which softwood was 199,500 cbms, 6.4% less, the

lowest since August 2014.

South Sea (tropical) Logs

After Indian buyers made big purchases of 250-300,000

cbms to cover two months demand in July in Sarawak,

they pulled out so supply side was pausing without much

activity. It is said that India will be in monsoon period for

two months so they procured before this season.

Also, China¡®s purchases weakened by high log inventories

in China and sluggish market. The suppliers are reducing

harvests in this situation. The Japanese buyers wish to take

this occasion to reduce the export prices.

Since late august Chinese currency, yuan depreciated and

the yen appreciated from 124 yen to the dollar to 120 yen.

Then the Malaysian currency, ringgit dropped to the

lowest since 1998. This increases revenues for suppliers.

At the same time, log supply in Sabah is increasing and

Japanese buyers shift to Sabah for log purchases. This

becomes a good leverage in negotiating with Sarawak log

suppliers.

Present prices of Sarawak meranti regular are US$280-290

per cbm FOB, slightly down from August but still high for

the Japanese plywood manufacturers. In PNG, after China

quiets down, purchase is easier for Japanese buyers but

due to weak yen the cost remains high.

|