|

Report

from

Europe

German and UK recovery boost European GDP

The Eurpean economy has climbed out of recession and,

after six years of trauma, appears to be on the mend. The

countries that required European Union-backed rescues

are beginning to exit these.

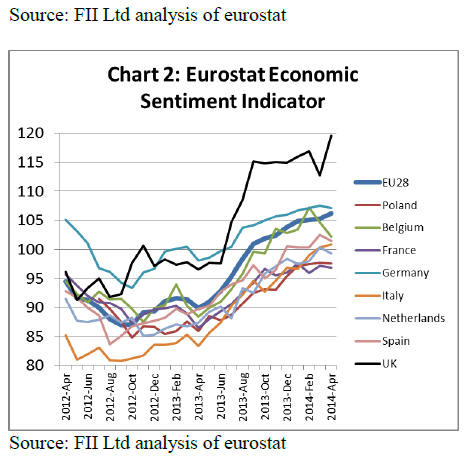

However the latest GDP figures (released on May 15 by

Eurostat) indicate that the recovery is very slow and

tentative (Chart 1).

GDP in the 18-nation euro-zone expanded by just 0.2% in

the first quarter of 2014, half the figure economists were

projecting. Total EU growth in the first quarter was only a

little higher at 0.25%, despite a strong performance by the

UK outside the euro-zone where the economy expanded

by 0.75%.

Germany, as usual, was the leader amongst European

countries, posting a gain of 0.8%. After a very long period

of economic contraction, Spain‟s economy is now growing

modestly, expanding 0.4% in the first quarter of 2014.

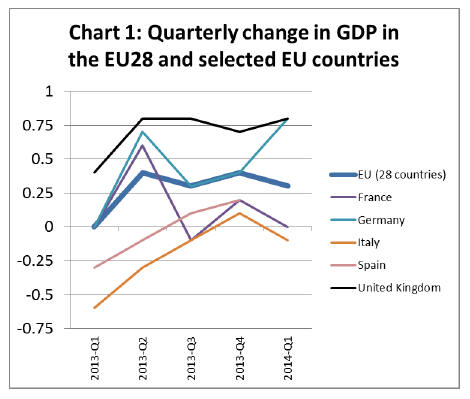

More positively, economic sentiment in Europe has

continued to rise sharply in recent months (Chart 2). The

rise is apparent across the EU but is particularly dramatic

in the UK and Germany.

Improvement in this indicator implies that both consumer

and investor confidence will continue to rise during the

European summer.

However, economic conditions in other countries of

Southern Europe remain fragile. Italy's economy shrank by

0.1% in the first three months of 2014, matching the

average of the three previous quarters.

France‟s recovery has faltered. France recorded zero

growth in the first quarter of 2014, a big downturn

compared to expansion of 0.6% in Q2 2013.

Portugal shrank 0.7% in the first quarter of 2014,

following positive numbers in the preceding nine months.

While figures weren't available for Greece in Q1, the signs

there are not good. Greek GDP dropped 2.5% in the final

three months of last year.

Economic growth in the EU is likely to remain very slow

this year. The latest forecast from the International

Monetary Fund estimates euro-zone GDP will expand a

mere 1.2% in 2014, compared with 2.8% for the U.S.

With prices barely rising, there is mounting concern that

the euro-zone could plunge into debilitating deflation. This

would make the debt burden of Europe‟s weakest

economies even heavier.

Europe has also made little progress in solving its‟

significant unemployment problem. The latest euro-zone

jobless rate is 11.8%, only marginally better than 12% a

year ago.

Only limited progress has been made to liberalise overregulated

labour markets which dampen job prospects

throughout much of Europe.

There is also conflict between European politicians‟ need

to encourage further economic integration to resolve the

problems of the euro-zone and the increasing

disenchantment of many EU citizens with centralised

control from Brussels.

EU construction �C uninspiring forecasts for 2014

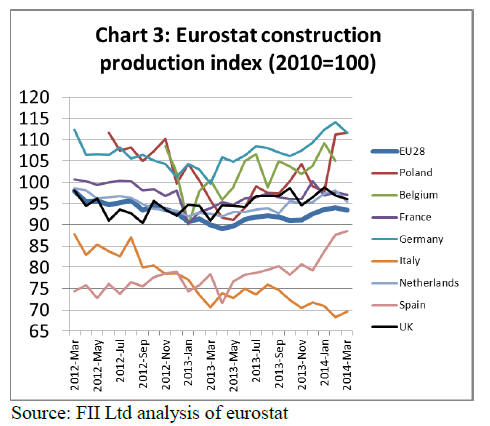

Europe‟s construction sector is by far the most important

driver of timber demand in the region. Recovery in this

sector has been even weaker than in the overall economy.

There has been only a slow and faltering increase in the

Eurostat construction production index since it hit an alltime

low in March 2013 (Chart 3).

Construction production in Germany, Poland, and

Belgium has strengthened significantly in 2014.

Construction production has also improved significantly in

Spain this year, although from a very low level.

Smaller gains have been made in the UK and the

Netherlands. However construction production has been

flat in France and continues to fall in Italy.

Modest improvement in construction expected from

2015

Various indicators of future construction activity suggest

that the overall EU market will remain static at a low level

in 2014. There is potential for a slow but sustained

recovery to start next year, led by the UK and Germany

and spreading into Belgium, Netherlands and Poland.

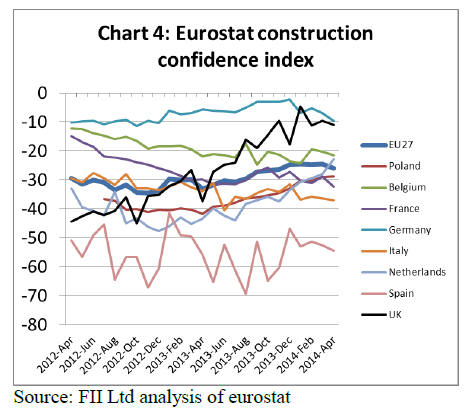

There was gradual improvement in Eurostat‟s EU-wide

construction confidence index (CCI) between March 2013

and March 2014 (Chart 4). However the CCI declined

slightly in April 2014 and remains firmly in negative

territory.

This means that a balance of those surveyed still believe

order books and employment in construction will continue

to decline in the following 3 months.

The German CCI remains high relative to other EU

countries but weakened a little in the opening months of

2014. The UK CCI, which increased sharply over the

winter months, has now flattened out at a higher level. The

Belgium CCI has also remained static in recent months but

is at least higher than in most other EU countries.

Confidence in the Netherlands construction sector has

improved significantly over the last 12 months after hitting

a very deep low at the start of 2013. Construction

confidence in France, Italy and Spain remains at a low

level.

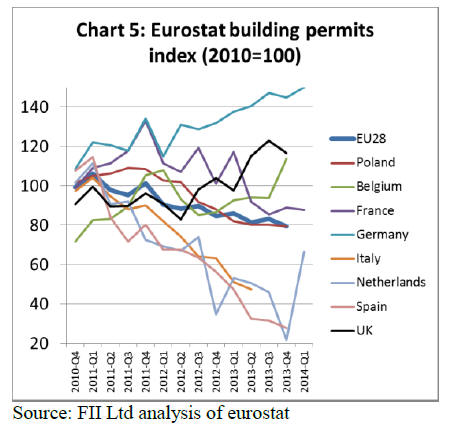

The latest EU-wide building permits data, for the last

quarter of 2013, is not encouraging from the perspective of

future construction activity (Chart 5). The numbers of

building permits issued across the continent continued to

decline throughout last year.

While there was a rise in permits issued in Germany, the

UK and Belgium, this was offset by declining permits in

Italy, Spain, France, the Netherlands and Poland.

First quarter 2014 data for building permits from those few

countries that have reported so far is more encouraging.

Building permits issued in Germany have continued to rise

this year, while there has also been a sharp rebound in

building permits issued in the Netherlands.

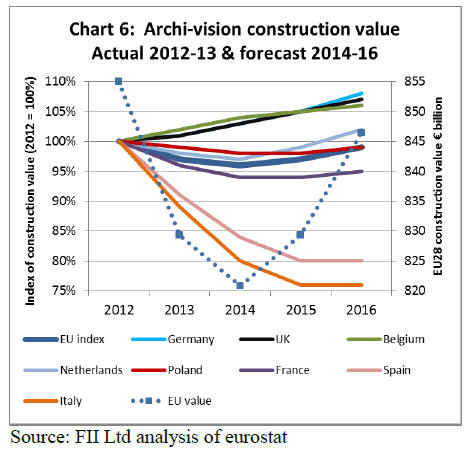

Value of EU construction forecast to fall in 2014

The independent research organisation ��Archi-vision��

estimates that total European construction value will fall

from €830 billion in 2013 to €820 billion this year (Chart

6).

However, construction value is expected to rebound to

€830 billion in 2015 and €845 billion in 2016. These

forecasts draw on Archi-vision‟s quarterly survey of 1600

architects across the EU combined with analysis of other

European construction industry data.

Archi-vision forecast that construction value will rise at

around 2% per year in the UK, Germany, Netherlands and

Belgium between 2014 and 2016. Construction value is

expected to remain static in France and Poland during this

period.

Construction value is expected to continue to fall in Italy

and Spain during 2014 and 2015 before stabilising at a low

level in 2016.

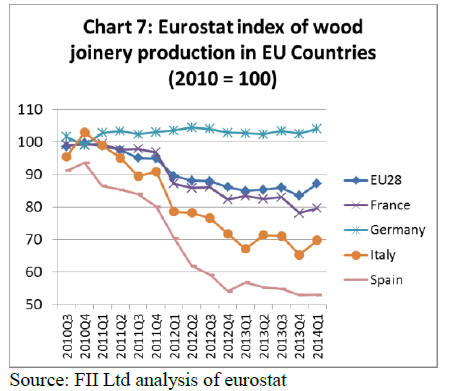

Improvement in EU joinery production in first quarter

of 2014

Overall joinery activity in the EU was static at a low level

in the first nine months of 2013 and then fell sharply in the

last quarter. However, activity picked up a little in the first

quarter of 2014 (Chart 7).

In line with forecasts for the European economy and

construction industry as a whole, joinery activity across

the region is expected to recover only slowly during 2014.

Of all European countries, only Germany has maintained

comparatively high levels of joinery activity over the last

two years.

Recovery in the EU joinery sector is expected to be led by

continued good levels of activity in Germany and a

relatively strong rise in the UK.

UK construction recovery now stronger and broader

The UK Construction Products Association (CPA)‟s latest

forecasts highlight that the recovery in UK construction is

becoming stronger and broader.

Rapid increases in private house building, together with

growth in the infrastructure and commercial sectors, will

drive activity. CPA forecast 4.5% growth in 2014 and a

further rise of 4.8% in 2015.

According to CPA, UK private housing starts are set to

rise 18.0% in 2014 and 10.0% in 2015, before falling to

5.0% in 2016 and 2017.

The current rise is assisted by a „Help to Buy‟ scheme,

which is subsidising mortgage provision, in addition to a

strengthening UK economy.

Growth in private housing should lead also to increases in

public housing. UK planning consent now usually requires

provision of some public housing as part of large-scale

private developments. CPA forecasts that public housing

starts will rise 8.0% in 2014 and 5.0% in 2015.

The UK‟s private housing repair, maintenance and

improvement sub-sector is forecast to rise 3.5% in 2014

and a further 4.0% in 2015. The CPA note that such

growth is well below potential given considerable demand

for energy efficiency measures in the UK's existing

housing stock.

Poor implementation and lack of decent incentives has led

to only poor uptake of the UK government's "Green Deal"

and ECO schemes designed to increase work in this area.

Commercial offices construction remains one of the

largest single components of UK construction and is

expected to increase 7.0% in 2014 and 10.0% in 2015,

although most growth will be concentrated in London.

Rising consumer confidence and pent-up demand for

refurbishment mean that activity in the UK retail subsector

should increase 4.0% in 2014 and 8.0% in 2015.

Public sector construction is forecast to marginally rise

0.7% in 2014 and 2.3% in 2015 as schools and hospitals

projects finally get underway after long delays during the

period of austerity.

Downturn in EU imports of joinery products

With the exception of flooring products, imports

contribute only a small proportion of total EU

consumption of joinery products. In terms of value, only

around 4.5% of doors and glulam, and around 0.5% of

wood windows installed in the EU are imported from

outside the region.

This is indicative of the very strong commercial benefits

from proximity to the consumer in the joinery sector and

the essential need for detailed knowledge of national

construction markets.

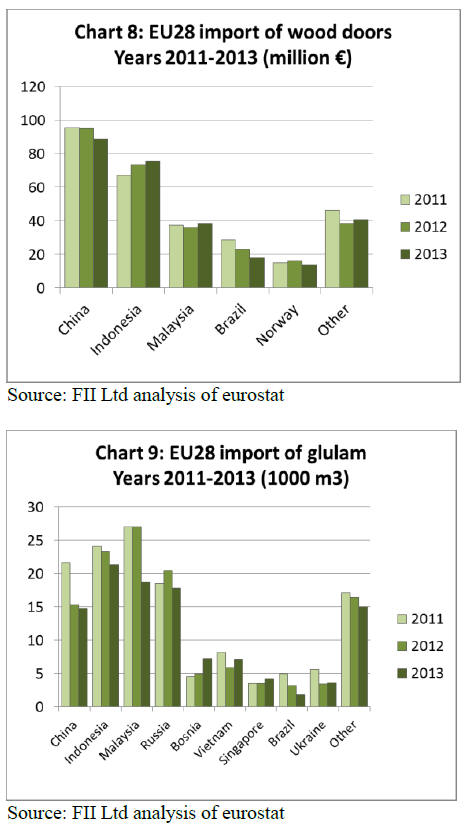

The EU imported wooden doors with total value of €275

million in 2013, 2.8% less than the previous year (Chart

8). The value of wooden door imports from China, the

largest non-EU supplier, fell 6.8% to €88.5 million in

2013.

However imports increased from Indonesia and Malaysia -

the second and third largest non-EU suppliers. Imports

from Indonesia rose 2.6% to €75.4 million in 2013.

Imports from Malaysia were up 6.3% at €38 million.

The EU imported 111,700 m3 of glulam in 2013, 9.5%

less than the same period in 2012 (Chart 9). During 2013

there was a significant fall in imports from Malaysia,

Indonesia and Russia, the three largest external suppliers

of glulam to the EU.

Imports from China, the fourth largest external supplier

were at a similar level to the previous year. Imports of

glulam from Vietnam increased slightly. The European

glulam market is currently suffering from saturation, with

too much production chasing limited demand.

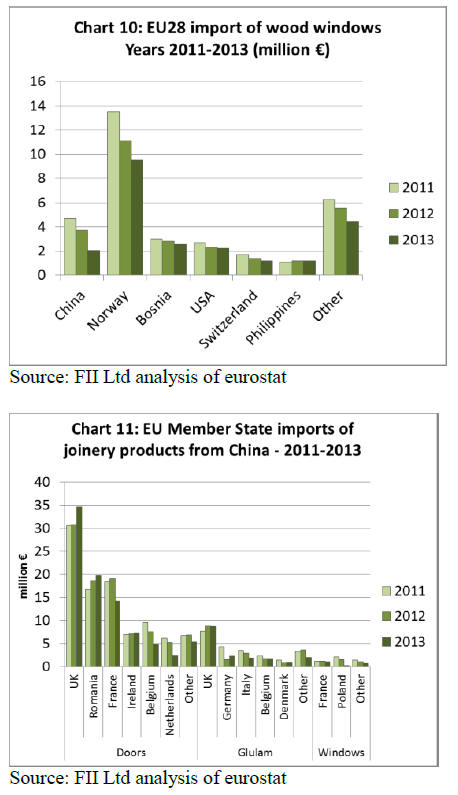

EU imports of wood windows were €23.1 million in 2013,

17.6% less than the previous year (Chart 10). Most of

these imports derive from other European countries,

notably Norway, Bosnia and Switzerland.

Imports from China, the largest supplier outside Europe,

were only €2.1 million in 2013, 45% less than the previous

year. Chart 11 provides more detail of recent trends in EU

markets for joinery products imported from China.

Imports of wooden doors from China increased into the

UK, Ireland and Romania during 2013, but declined into

France, Belgium and the Netherlands. German and Danish

imports of Chinese glulam increased during 2013, but this

was insufficient to offset declining imports into UK, Italy,

and Belgium.

EU imports of wooden windows from China have been

mainly destined for France and Poland, both markets

which weakened significantly in 2013.

European flooring industry reports continuing

challenges

Discussions at the spring meeting of the European wood

flooring manufacturers association FEP indicate that the

industry continues to face major challenges. There are

some signs of improving demand in a few countries and of

a more stable situation in others.

However the market remains very difficult in Southern

Europe. Lack of consumer confidence, the weak European

construction sector as well as an ever increasing

competition are daily challenges for the European wood

flooring industry.

FEP country representatives reported as follows:

Austria: a small increase of around 1% is

forecast in consumption in the first quarter of

2014 compared to Q1 2013. There is increasing

competition for wood flooring from Luxury

Vinyl Tiles (VLT).

Belgium: the wood flooring market has

stabilised. Although total construction output fell

1.3% in 2013, there was improvement in nonresidential

construction, both new build (+2.2%)

and renovation (+1%).

Denmark: parquet sales were static at a low level

in the first quarter of 2014, but the market is

expected to grow by a few percentage points

during the whole of the year.

Finland: parquet consumption is expected to

remain stable during 2014 with total sales of

around 1 million m2.

France: the year 2014 started badly with parquet

sales down an estimated 8% to 10% in the first

quarter of 2014 compared to the same period in

2013. Consumer confidence is still lacking.

Traditional retailers no longer regard wood

flooring as a priority product. Competition with

other flooring types is becoming even more

intense.

Germany: Despite the good economic situation

in Germany, the parquet market remains static

with zero growth expected this year and intense

competition from other products. As in the past,

wider boards are becoming increasingly popular.

DIY stores are moving towards new products

such as LVT.

Italy: parquet consumption is estimated to have

decreased by 10% in the first quarter of 2014

compared to the same period in 2013. Conditions

are very uncertain with a lot of new competitors

on the market.

Netherlands: After a very poor year in 2012, the

market stabilised in 2013. First quarter sales in

2014 were the same as in the first quarter of

2013.

Norway: sales increased by around 2% in the

first quarter of 2014 compared to the same period

in 2013. Imports of building materials into

Norway increased by 18% in the first 3 months of

2014, an indication of an active market.

Spain: parquet sales in the first quarter of 2014

were down 5% compared to the same period of

last year. However, there is a slow rise in

optimism as some macroeconomic indicators are

recovering.

Sweden: parquet consumption was up around 2%

in the first quarter of 2014 compared to the same

period in 2013. The housing sector is starting to

recover.

Switzerland: a very mild winter meant that

parquet sales in the first quarter of 2014 were 5%

higher than the same period in 2013. Wood

flooring remains popular and the market mood is

good.

|