|

Report

from

Europe

EU tropical wood imports decline 13% in 2013

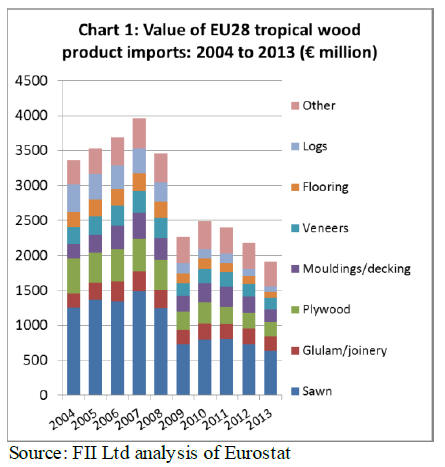

The EU imported tropical wood products with a total value

of €1.91 b illion in 2013, 12.6% less than the previous

year.

Between 2012 and 2013, import value declined across all

product groups including:

sawn wood (down 13.2% to €633 million),

joinery products (down 8.8% to €208 million),

plywood (down 5.6% to €206 million),

mould ings and decking (down 26.4% to €177 million),

veneers (down 4.9% to €168 million),

flooring (down 21.7% to €88 million),

logs (down 15.6% to €83 million)

and

other products (down 8.8% to €347 million).

EU tropical wood import value last year was around 50%

of the peak achieved in 2007 and is the lowest recorded in

recent years (Chart 1).

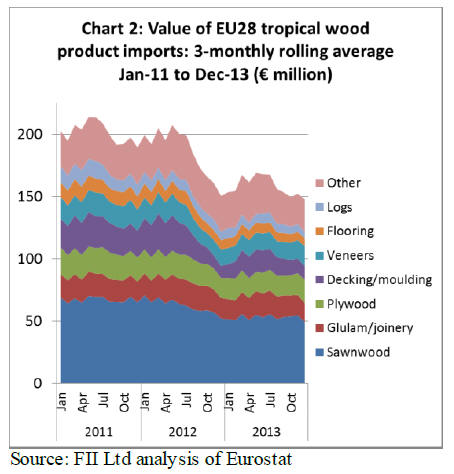

Closer analysis of monthly data indicates that EU tropical

wood imports hit a low of €150 million in December 2012

and then staged a brief recovery over the spring and

summer period to reach a high of €169 million in May

2013 (Chart 2).

However, monthly imports fe ll back again to only €148

million in December 2013 when there was a particularly

sharp downturn in sawn hardwood imports. The fall in EU

imports of tropical wood products in 2013 was part of a

wider trend of declining imports across nearly all forest

product groups, including sawn softwood, temperate

hardwood products, wood furniture and pulp and paper.

This is explained by the combined effects of recession in

Europe, supply diversion to other more active global

markets, and rising share of domestic production in EU

consumption.

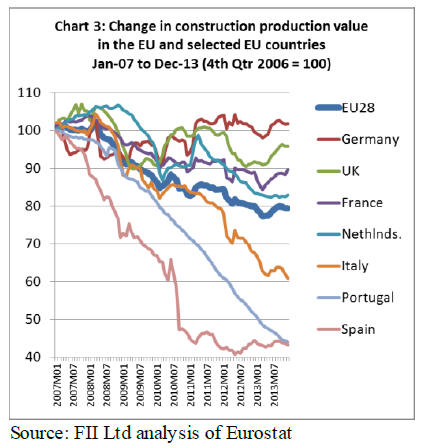

EU construction rises slightly but remains 20% below

pre-crises levels

A variety of indicators show that March 2013 was the

point at which economic activity across Europe was at its

lowest ebb at the end of a long cold winter. This is

particularly true of the construction sector, such an

important driver of timber demand in Europe.

Total construction value across the EU in March 2013 was

23% less than in early 2007 just prior to the financial

crises. In the months following March 2013, EU

construction activity increased marginally to around 20%

below the pre-crises level.

Chart 3 reveals how the t iming and depth of construction

industry recession and recovery have varied widely

between countries. Construction activity in Germany, the

UK and France has been relatively resilient over the last 5

years and was showing signs of revival in the second half

of 2013.

This is in contrast to Spain, Portugal and Italy where the

value of construction is well down on pre-recession levels

and has yet to show any signs of recovery.

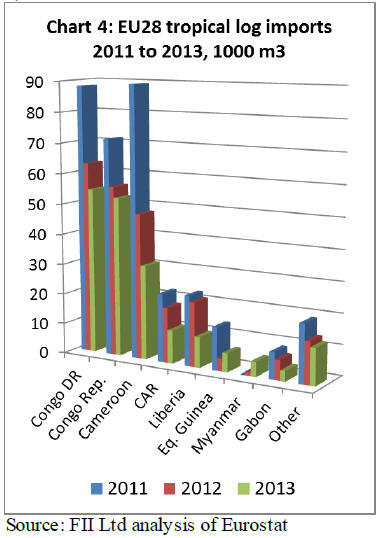

EU tropical log imports fall another 20%

EU imports of tropical hardwood logs were 186,000 m3 in

2013, down 20% compared to the previous year. Imports

of this commodity into France, the main destination, were

down 20% at 86,350 cu.m.

Imports from all the leading supply countries declined,

including Congo (Kinshasa), Congo (Brazzaville),

Cameroon, Central African Republic, and Liberia (Chart

4).

The decline is due to the combined effects of weak

European demand, supply constraints, and regulatory

uncertainty. The European okoume plywood

manufacturing sector, formerly a major buyer of logs, has

struggled to compete during the recession and capacity is

now small, with a significant share of production having

relocated to Gabon.

Due to supply problems and rising log prices, more central

European mills that formerly imported tropical hardwood

logs for sawing and slicing have switched to temperate

hardwoods this year.

On the supply side, polit ical unrest restricted log

availability from Central African Republic in 2013. The

Liberian government placed a freeze on all logging

activities in January 2013, including on the exportation of

logs from the country.

Meanwhile, encouraged by the EUTR, environmental

groups have focused heavily on finding discrepancies in

the legal documentation for log exports from the Congo

basin. This has added to the already high level of

uncertainty in the EU tropical hardwood log trade.

The only significant upward t rend in EU tropical log

imports was of teak from Myanmar. This has followed the

end of trade sanctions and has also been encouraged by

Myanmar��s announcement of a ban on log e xports fro m

April 2014. The main European end users in the boat -

building sector have been building stocks in advance of

the measure.

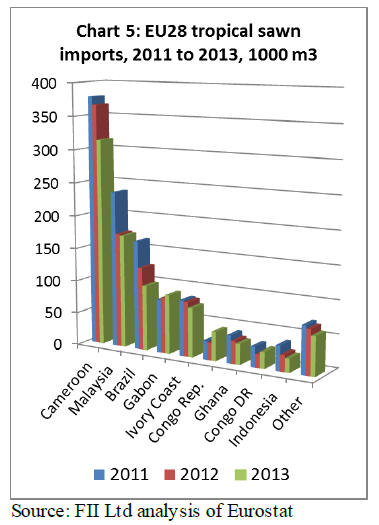

EU sawn tropical hardwood imports down another 8%

EU28 imports of tropical sawn hardwood in 2013 were

930,000 m3, 8% down on the previous year (Chart 5).

Declining imports from Cameroon, Malaysia, Brazil, Ivory

Coast, Ghana and Indonesia were only partly offset by

rising imports from Gabon and the Congo countries.

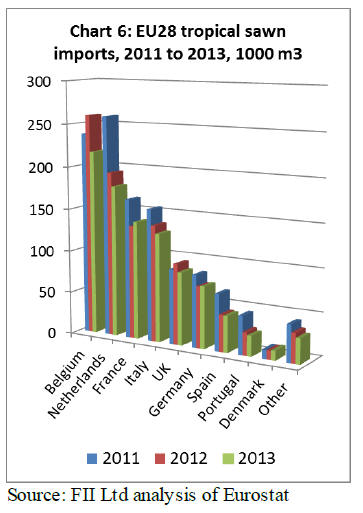

Imports of sawn tropical hardwood declined into Belgium,

Netherlands, Italy, UK, Spain, and Portugal. However

there was a 4% increase in imports into France and

imports into Germany remained level (Chart 6).

EU imported 314,000 m3 of sawn hardwood from

Cameroon in 2013, 14% less than the previous year. This

was partly due to mounting supply problems in Cameroon

which have been particularly pronounced for sapele, the

most popular commercial species in Europe.

By the end of 2013, lead times for delivery into Europe of

new orders of sapele from Cameroon were around 6

months. This resulted in sharply rising prices both on an

FOB basis and for landed stock in the EU.

EU imports of sawn wood from Cameroon were low in the

first half of 2013 before recovering slightly in the third

quarter. However they fell back sharply in December

2013, a short trading month when there was also a strike at

Came roon��s ma in port of e xport in Douala.

Gabon was the second largest African supplier of tropical

sawn wood into Europe in 2013, supplying 89,000 m3

during the year, a gain of 6% compared to 2012. In the

early months of 2013, EU imports of sawn hardwood from

Gabon were affected by the economic slowdown in

France, the main market, and by harvesting restrictions

which led to reduced log supply in the country.

However, both problems eased during the course of 2013

which led to a strengthening recovery in EU imports from

the country.

Some of the large European owned operations in Gabon

which have made a strong commitment to delivery of

certified wood products may also now be benefitting from

the introduction of EUTR in March 2013.

This might also partly explain the 65% increase in EU

imports of sawn hardwood from the Congo Republic to

44,000 m3 in 2013.

EU imports of tropical hardwood from Cote d��Ivoire fe ll

10% to 75,000 m3 in 2013. Most of this decline occurred

in the early months of the year when EU importers were

concerned about possible EUTR conformance issues.

However, EU imports from the country recovered in the

second half of 2013 as traders grew more confident that

the available legal documentation would stand up to

EUTR scrutiny. EU imports from Ivory Coast also

benefitted from slow recovery in demand for key species

like framire and ayous in the UK and Italian markets

during the second half of 2013.

EU imported 172,000 m3 of sawn hardwood from

Malaysia in 2013, 1% less than the previous year. Imports

from Malaysia were particularly weak in the first half of

2013, due to very slow activity in the northern European

construction market.

Orders picked up towards the end of the year, part ly in

response to improved demand, part icularly in the German

and UK construction sectors, together with restocking in

advance of the increase in EU import duties on Malaysian

products from 3.5% to 7% on 1 January 2014 due to a

change in Malaysia��s GSP status.

EU sawn hardwood imports from Brazil fell 21% to

99,000 m3 in 2013, continuing the sharp downward trend

which set in at the start of the European recession.

The decline from Brazil is due to the combined effects of

weak EU demand, exchange rate volatility and rising

prices in response to improved US demand and more

restricted supply as the Brazilian government has taken

steps to curtail illegal logging.

The problems of obtaining legality assurance in the

complex fragmented supply chains that exist in the

Brazilian Amazon may be another contributing factor

since implementation of EUTR.

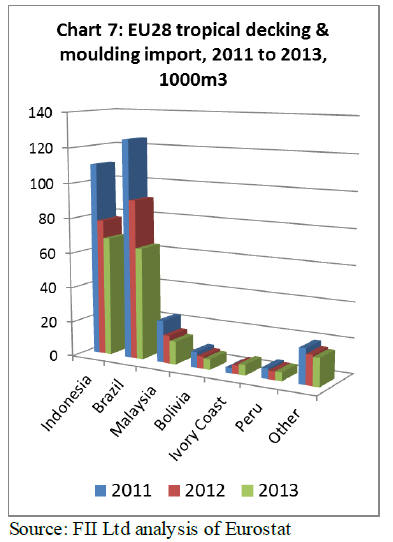

Downward trend continues in EU decking and

mouldings imports

EU imports of �Dcontinuously shaped�� wood (HS code

4409) from tropical countries fell 19% in 2013 to 178,000

m3 (Chart 7).

Imports from Brazil fell part icularly heavily, down 30% to

64,000 m3. Imports also fell from Indonesia (-13% to

68,000 m3), Malaysia (-19% to 13,000 m3).

Continuously shaped wood products listed under HS4409

include both decking products and interior decorative

products like moulded skirting and beading. The market

for tropical hardwood decking timbers in Europe during

2013 was very slow.

Imports were impacted by a stock overhang after low

levels of consumption in 2012. As prices for Asian

bangkirai declined in 2013, Amazonian species like garapa

and massaranduba became less competitive so that imports

from Brazil fell part icularly heavily.

Tropical hardwood also suffered a further loss of share in

the decking sector both to other wood species and to

Wood Plastic Composites.

EU imports of tropical mouldings for interior applications

were also declining in 2013 due to falling competitiveness

relative to EU domestic production.

For e xamp le, Bra zil��s hardwood industry continues to

suffer from high and rising labour and other business

costs. Hardwood decorative mouldings of all types are also

coming under intense competitive pressure from pine and

MDF.

However there were isolated reports in 2013 of some

tropical interior mouldings products regaining market

share at the expense of temperate hardwoods. For

example, in recent years American tulipwood made

significant inroads into the European market for painted

mouldings.

In 2013 Ghanaian wawa was retaking share as the price of

American tulipwood increased. During 2013, lack of log

supply and rising US and international demand led to a

significant increase in prices across the full range of

American hardwood species.

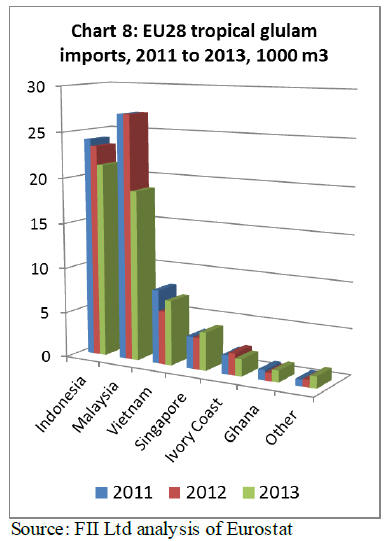

Falling EU imports of engineered wood window

scantlings from the tropics

Weak construction sector activity during 2013 led to

further declines in EU glulam imports (Chart 8). EU

imports of this product, which consist primarily of

scantlings for the window sector, were 56,000 m3 in 2013,

12% less than the previous year.

EU imported 19,000 m3 of scantlings from Malaysia in

2013, 31% less than the previous year. Imports from

Indonesia declined 9% to 21,000 m3 in 2013. However,

there was a slight increase in EU imports of glulam

products from some smaller suppliers, including Vietnam,

Singapore and Ghana.

Short-term prospects for meranti window scantling in the

EU market remain poor. Despite limited imports in 2013,

importers�� inventories are still quite high relat ive to slow

demand.

However longer term prospects appear more promising.

More building permits are now being issued in Germany,

the leading European market, and there is rising

confidence in the German construction sector.

The UK construction sector is also rebounding more

strongly than expected this year. The UK has not been a

significant market for tropical hardwood glulam in the

past, but interest in engineered scantlings is now rising

with introduction of tougher quality and energy-efficiency

standards for wood windows.

These factors, together with limited supply of sapele, the

leading African wood used in European joinery, might

lead to improving European demand for meranti window

scantlings during summer 2014.

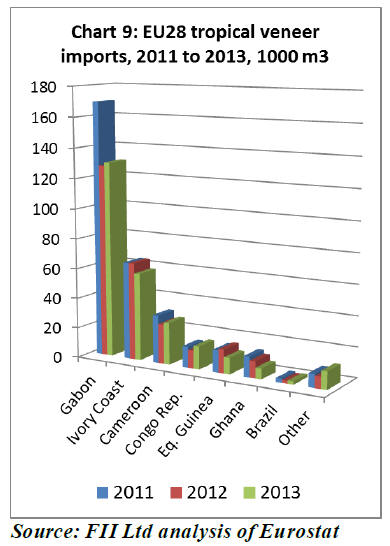

Tropical hardwood veneer imports stabilise at a low

level

After significant falls in previous years, EU imports of

tropical hardwood veneers stabilised at a low level in 2013

(Chart 9).

Imports were 263,000 m3, 1% down compared to the

previous year. Imports from Gabon - which fell heavily

between 2011 and 2012 - increased 2% to 130,000 m3 in

2013. Imports also increased 5% from Cameroon and 29%

from the Congo Republic in 2013.

However imports from Ivory Coast fell 10% and imports

from Equatorial Guinea were down 31%.

The EU market for hardwood veneers remains very

difficult, with producers suffering from declining turnover

in the face of lower sales volumes, declining prices and

continuing loss of market share to competitors.

Prices continue to be under pressure for mass -production

grades for the plywood, flooring and furniture, and this

pressure also now extends into the market for more

specialist grades. Demand and prices are not expected to

recover significantly in 2014.

ETTF reports only limited impact of EUTR so far

While it��s possible that some of the recent downturn in EU

imports of tropical wood was due to legal uncertainty

following implementation of the EUTR, other economic

and commercial factors were probably much more

significant drivers of trade during 2013. According to a

recent analysis of the trade impact of EUTR by the

European Timber Trade Federation:

�Dlonger term trends are obscured by the overwhelming

effect of the economic downturn and by supply problems

due to capacity closures and diversion of wood fibre to

other markets over recent years��.

Furthermore, while EUTR has been enforceable since

March 2013 in theory, it is still very early days in practice.

This is clear from the recent survey of EUTR authorit ies in

EUWID. The German trade journal reports that Competent

Authorities are already active in Denmark, UK, Germany,

and the Netherlands.

However the pace of implementation has been slower in

France and southern and eastern Europe. The EC process

to formally recognise Monitoring Organisations is also

taking time, with only two so far appointed - Conlegno in

Italy and Nepcon with EU-wide coverage.

Even in countries where Competent Authorities are act ive,

building up the necessary capacity and knowledge

required to provide advice and pursue successful

prosecutions remains a challenge.

The real impact of EUTR will only become clearer as the

EU economic recovery gathers pace and as more progress

is made to develop enforcement capacity and impose

sanctions.

|