Japan Wood Products

Prices

Dollar Exchange Rates of

23th April 2013

Japan Yen

99.45

Reports From Japan

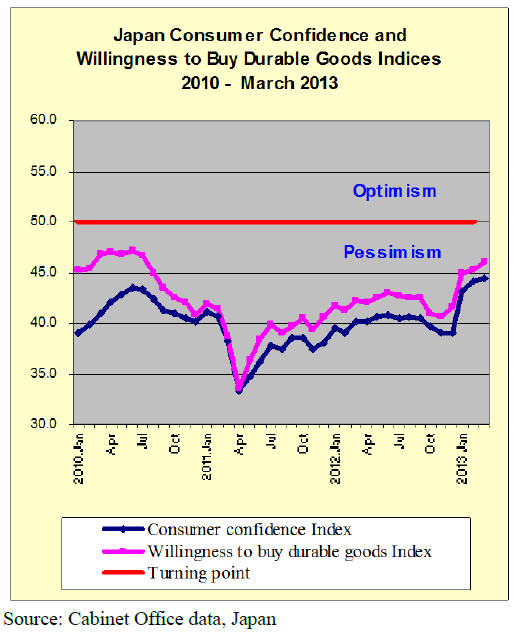

Consumer confidence upbeat but target missed

The results of a survey of consumer confidence in Japan

were released in mid April. The consumer confidence

index rose to 44.5 in March, the highest level since

February 2007 when it was 48.4. However, the

government was expecting the index to climb to 46.0.

The March index was the third consecutive rise after the

full 1.0 point rise in February this year. Analysts suggest

that aggressive government and central bank policies fiscal

are having the desired effect.

The Japanese Cabinet Office upgraded its view on the

consumer sentiment index saying it is showing signs of

improvement. However it should be remembered that a

reading below 50 suggests consumer pessimism.

The view of Japanese households of overall livelihood was

unchanged for March with the relevant index unchanged at

42.9. Expectations for higher earnings were also

unchanged from the previous month.

However, Japanese consumers were slightly less

pessimistic about the employment situation and the index

for their intention to buy durable goods was better.

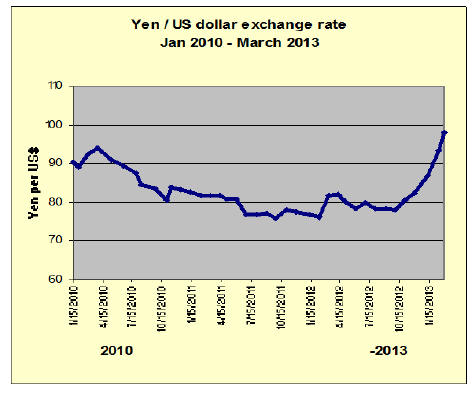

Any further exchange rate fall will be decided by

institutional investors

On 17 April the yen fell to 99,72 to the US dollar, its

lowest in almost four years. The steep drop in the value of

the yen surprised markets and was driven by a debt buying

spree by the Bank of Japan (BoJ).

The BoJ began its debt buying on 8 April, purchasing

almost US$16 billion in its first phase of its stimulus plan.

This move by the BoJ will ensure that borrowing costs

remain low.

The yen fell to new lows against major currencies in the

first week of April almost testing the 100 yen to the US

dollar mark.

However, every fall in the value of the yen pushes up the

cost of imported fuel and this poses a risk to domestic

demand as almost all fuel is imported. Almost all nuclear

reactors in Japan have been shut down for safety checks

after the recent disaster and power generation depends

entirely on imported fuel.

For a sustained weakening of the yen there would need to

be decisive moves by Japanese institutional investors to

start buying higher-yielding assets. Some hints that this

has begun as the yield on some European bond yields have

fallen.

Weak yen impacts Eurozone prompting calls for EU

growth strategy

The Japanese yen had, by the end of this month, fallen by

more than 20% against the euro and, while Japan accounts

for just 4-5% of trade in the EU, cheaper exports from

Japan are undermining the competitive position of EU car

makers and heavy machinery makers amongst others.

To compete, EU manufacturers are faced with having to

reduce market sales prices and some analysts are openly

talking of a price war in the EU.

In a market which is burdened by austerity policies lower

priced imports such as those now available from Japan

weaken domestic EU companies who are now calling for

more growth friendly policies to combat EU deflation.

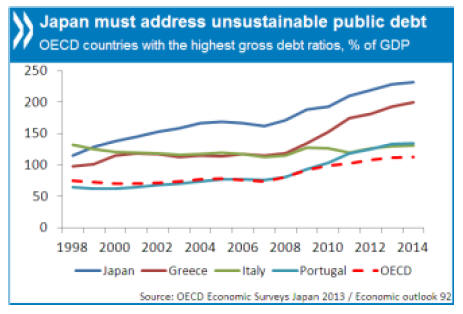

OECD lends support to Japan’s economic policies

Critics of „Abenomics‟, the term coined to describe

Japan‟s bold economic policies, are trying to decide if this

will aid global economic recovery or just create a shortterm

boost to the economy.

An OECD press release introducing the latest OECD

Economic Survey of Japan provides the organization‟s

view of prospects for the Japanese economy.

Overall, the OECD is supportive of the moves taken by the

Japanese government and central bank but warns; “ Japan

is poised for an economic expansion, but long-term growth

prospects remain contingent on additional efforts to

revitalise the economy and reduce unsustainable levels of

public debt.”

The new Survey, presented in Tokyo by OECD Secretary-

General Angel Gurría, forecasts the Japanese economy

will grow by about 1.5% annually in 2013 and 2014.

For the press release see:

http://www.oecd.org/newsroom/japan-is-poised-forexpansion-

but-must-curb-government-debt.htm

The press release says “Japan‟s gross public debt reached

220% of GDP in 2012, the highest level ever recorded in

the OECD area, while the budget deficit is hovering

around 10% of GDP.

With the debt ratio moving further into uncharted territory,

the report underlines the urgent need to restore fiscal

sustainability.

The sustainability of public finances is a major concern

but that the medium-term fiscal plan that the government

has promised to present later this year should include

spending cuts and tax increases large enough to bring the

budget back into primary surplus by 2020 and stabilise the

public debt ratio.”

A detailed and credible package is essential to maintain

market confidence in Japan's fiscal situation, mitigating

the risk of a run-up in long-term interest rates says the

OECD.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to extract and reproduce news on the Japanese

market.

The JLR requires that ITTO reproduces newsworthy text

exactly as it appears in their publication.

For the JLR report please see:

http://www.nmokuzai.

com/modules/general/index.php?id=7

Wood supply and demand statistics

The Ministry of Agriculture, Forestry and Fisheries

announced wood demand and supply statistics of 2012.

Total demand was 24,650 M cbms, 0.3% up. In wood

supply, domestic wood was 18,470 M cbms, 1.0% up.

Imported wood was 6,177 M cbms, 1.6% down so that

share of domestic wood was 74.9%, 0.5 points up from

2011.

Wood demand in 2012 (log shipment volume to sawmills,

plywood mills and chipping plants) was almost unchanged

from 2011. Both sawmills and plywood mills‟ demand

dropped some from 2011 but the volume for wood chip

plants increased.

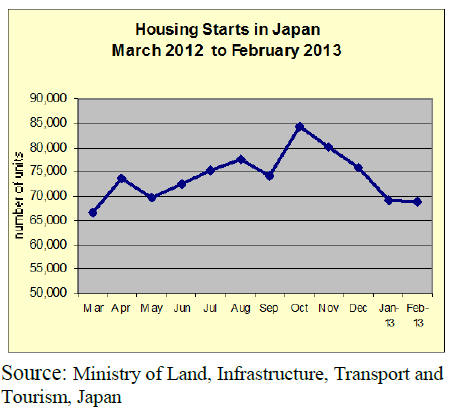

Housing starts were 882,797 units in 2012, 5.8% more

than 2011 but plywood mills curtailed the production by

over supply in 2011 with rush orders after the North East

Japan Earthquake in March 2011, which reduced wood

consumption in 2012.

Domestic logs for plywood use were 2,602 M cbms, all

time high record.

In imported wood, North America and New Zealand

increased but import from Russia and South Sea Asia

significantly decreased in 2012.

Number of sawmills in 2012 was 5,927, 315 mills or 5%

less than 2011. Number of sawmills in 2002 was 10,394 so

it dropped by almost half in ten years.

Shipment of lumber in 2012 was 9,302 M cbms, 1.4% less

than 2011 out of which kiln dried lumber was 2,744 M

cbms, 4.3% more.

Tropical logs

Rainy season in Malaysia is almost over but Sarawak still

has foul weather and log production remains low.

Local plywood mills are aggressively buying logs to run

the mills steadily.

India has resumed log purchase again since last month.

Thus, supply and demand of logs are badly imbalance so

the log suppliers continue asking higher prices.

Sarawak meranti regular prices are $280 per cbm FOB or

higher, more than $10 up from previous contract.

Shipment for Japan is down to one shipment in two

months after many South Sea log peeling plywood mills

are gone.

Log inventories are over three months now so that they

procure minimum volume only.

Meranti small prices are about $240, $10 up. Sabah kapur

regular prices are firming at about $365.

China buys PNG logs actively so that log prices are

climbing. For Japan market, callophylum prices are $290,

$10 up. Mersawa is $280-290 and MLH is $185, $20 up.

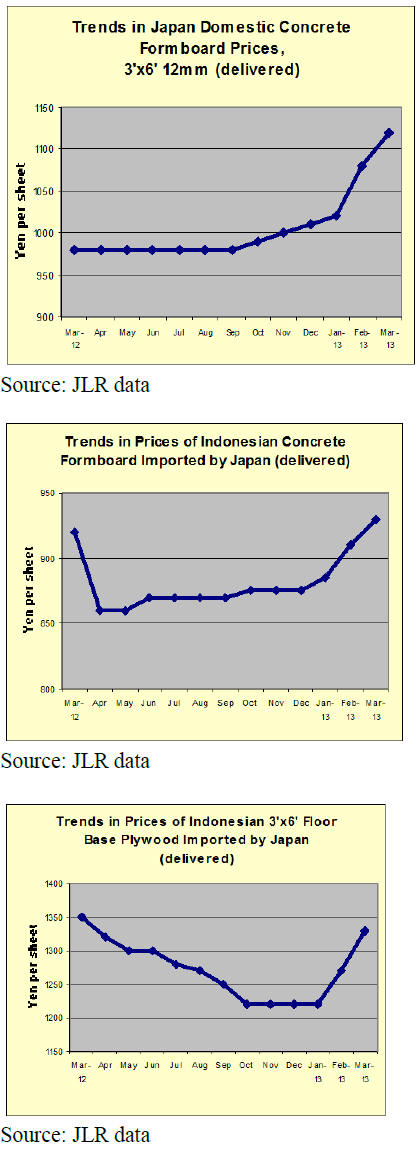

Log prices in Japan are firm due to weak yen. Meranti

regular log prices are 8,800 yen per koku CIF, 500 yen up

from March. Log prices will be higher in coming months

by higher FOB and weak yen so plywood mills asked 20%

price hike on plywood.

since last February but the hike so far is only less than

10%.

Market for imported tropical plywood

The suppliers in the South East Asia continue asking

higher export prices. In Malaysia, weather remains

unstable yet and log production is low so that the log

prices are gradually increasing.

Plywood mills‟ production is inactive so that the order

balances keep swelling up. With higher log cost and

climbing labor cost, plywood mills are asking higher

plywood prices.

Meantime, the yen is getting weaker so the largest

exporting plywood mill closed up April delivery of JAS

concrete forming 3x6 at 52,000 yen per cbm C&F and has

started asking 55,000 yen now. The price was 40,000 yen

in December last year so this is real steep hike.

In Japan, movement of imported plywood is momentarily

resting so that sharp price increase is difficult. Therefore,

importers are cautious to commit high priced future

cargoes until higher prices are accepted in the market.

The importers are restraining both purchase and sales now.

Actually they seem to wait until actual demand shows up

and necessity comes up to procure future cargoes. They

can tide over by adjusting the inventories for some time.

By limited supply with higher export prices by the

suppliers, the market prices in Japan are holding so it

looks like confrontation by three parties, suppliers,

importers and distributors continues for some time.

However, the inventories continue declining in Japan with

reduced purchase since last February so there are some

worries about shortage in the market in coming months.

Current market prices in Tokyo on JAS concrete forming

3x6 panel are 1,080-1,100 yen per sheet delivered, 30-50

yen up from March.

Orders for major house builders in March

March orders were very brisk for major house builders as

more people think this is time to buy. Factors are future

hike of mortgage interest rate, recovery of stock market,

coming raise of consumption tax and higher house prices

in future by materials inflation by weakening yen.

However, for house builders, works have been delayed by

shortage of carpenters and craftsmen and some builders

notify customers it would take time to complete.

Sekisui House had active orders in March. Orders for

detached units increased by 7% compared to March last

year. Rental units were up by 26% and units built for sale

were up by 34% but condominiums and renovation

business were down so overall house business was up by

10%.

Daiwa House had 4% more orders for detached unit, five

consecutive months increase. Units built for sales were up

by 49% so overall housing business including property

trading was up by 16%.Condominium sales and

renovation business were down by 9% and 5%.

Sumitomo Forestry had 4% more orders for detached

custom made units. Sales of environmentally friendly

houses and units for rebuilding have been steady.

Misawa Home had 8% more orders on detached units in

March, out of which custom made units were 7%, units

built for sale were 18% and rental units were 14% up,

making overall house business increase of 9%. Mitsui

Home‟s custom made units increased by 25%.

For the complete housing data see the Construction

Research and Statistics Office

Policy Bureau, Ministry of Land, Infrastructure, Transport

and Tourism website at:

http://www.mlit.go.jp/toukeijouhou/chojou/stat-e.htm

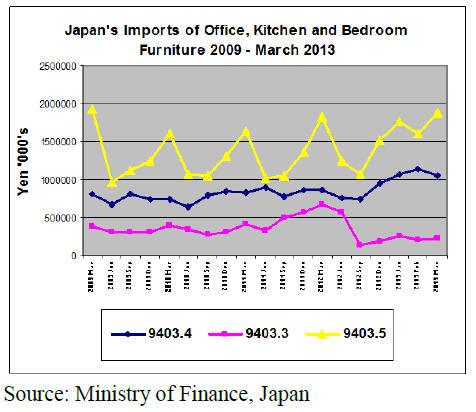

Japan’s furniture imports

January 2013 furniture imports

The source and value of Japan‟s office, kitchen and

bedroom furniture imports for March 2013 are shown

below. Also illustrated is the trend in imports of office

furniture (HS 9403.30), kitchen furniture (HS 9403.40)

and bedroom furniture (HS 9403.50) between 2009 and

March 2013.

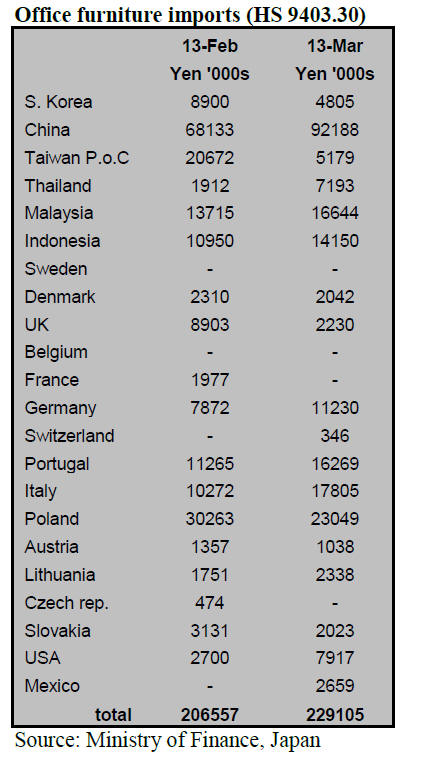

Office furniture imports (HS 9403.30)

In March 2013 three countries provided more than half of

the total office furniture imports by Japan.

The combined total of imports from the top three

suppliers, China Poland and Italy in March amounted to

yen 133 bil. or 57% of total office furniture imports.

Imports from China rose 35%, those from Poland fell 23%

while imports from Italy jumped around 70%.

The other major suppliers were Malaysia and Indonesia

which, together added a further 13% to the total trade in

office furniture.

In March, Japan‟s total office furniture imports totaled yen

229 bil up 11% from February. It is interesting to note that

Vietnam does not feature as a top 20 supplier of office

furniture to Japan despite being a major supplier of kitchen

and bedroom furniture to the Japanese market.

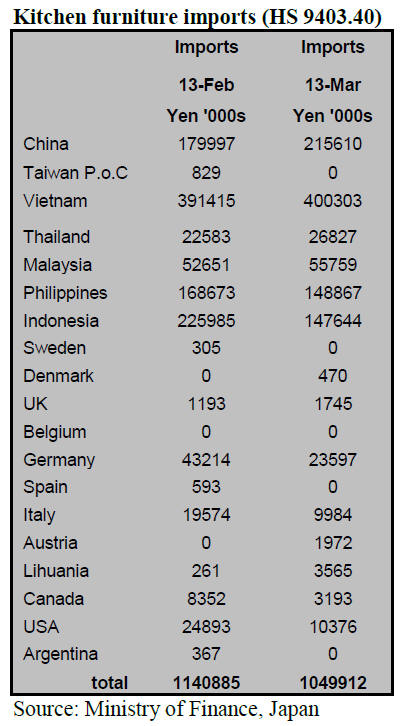

Kitchen furniture imports (HS 9403.40)

Kitchen furniture imports remain the second largest

segment of all wooden furniture imports into Japan after

bedroom furniture.

Vietnam maintained its number one position as the

supplier of kitchen furniture to Japan in March and the

value of imports from Vietnam were largely unchanged

from February at yen 400 bil.

The top five suppliers of kitchen furniture accounted for

over 90% of all kitchen furniture imports. Vietnam

supplied yen 400 bil. (unchanged in March), China yen

215 bil. (up 16%), Philippines yen 148 bil. (down 12%),

Indonesia yen 147 bil. (down 34%) and Malaysia yen 56

bil. (up 6%). Total imports of kitchen furniture in March

were yen 1,049.9 bil ., down from yen 1140.8 bil in

February, an 8% decline.

The US and Canada feature as suppliers of kitchen

furniture but in March both experienced a fall in Japanese

imports. US sales were down 45% while Canadian sales to

Japan were down around 37%.

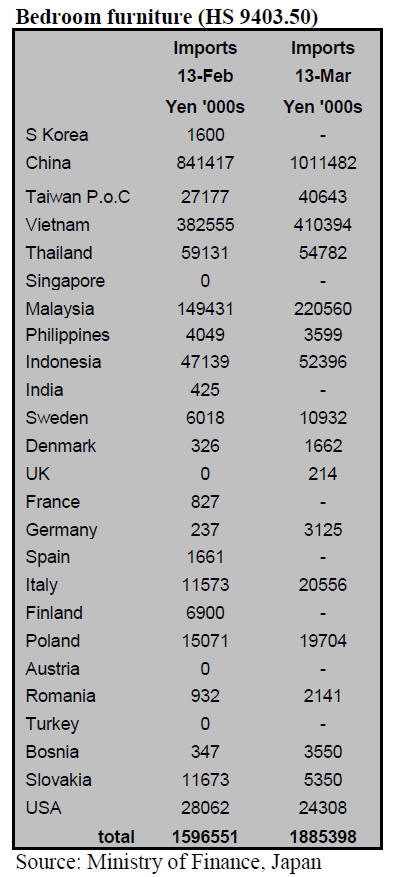

Bedroom furniture (HS 9403.50)

The value of Japan‟s bedroom furniture imports in March

2013 rose 18% from a month earlier, from Yen 1.6 bil. to

Yen 1.9 bil.

As in February this year the top suppliers were China and

Vietnam which together accounted for around 75% of all

wooden bedroom furniture imports to Japan.

Imports from China during March increased 20% and

imports from Vietnam increased around 8%. Other

countries supplying over yen 40 mil. include Malaysia,

Taiwan P.o.C, Thailand and Indonesia.

|