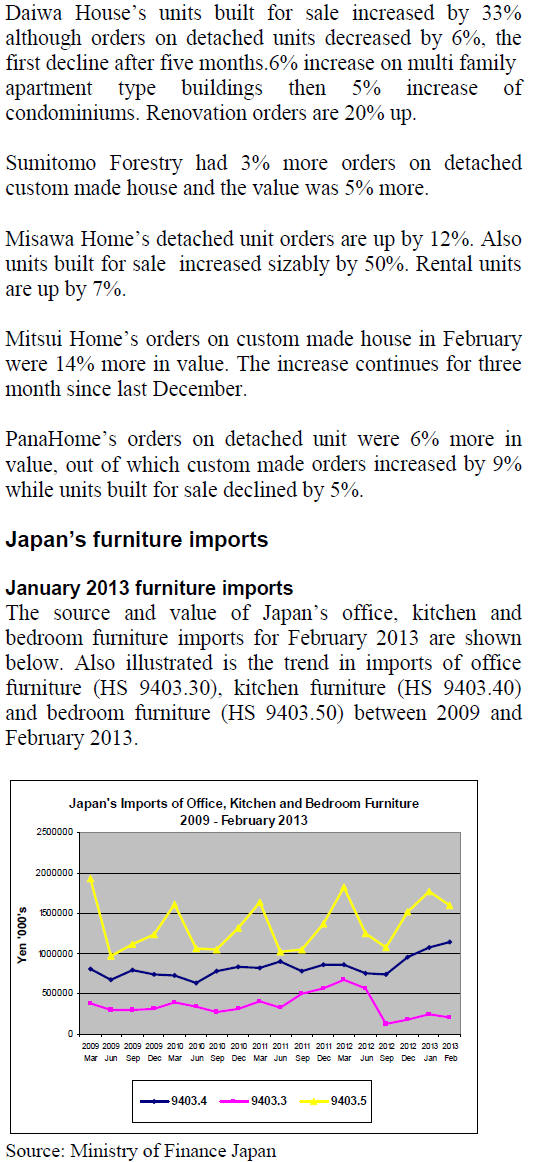

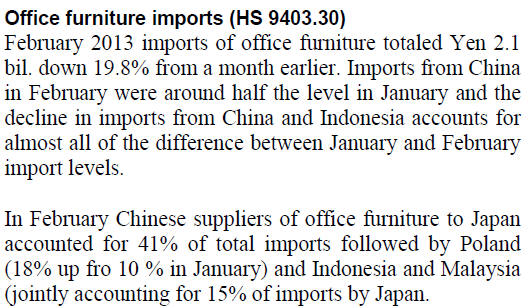

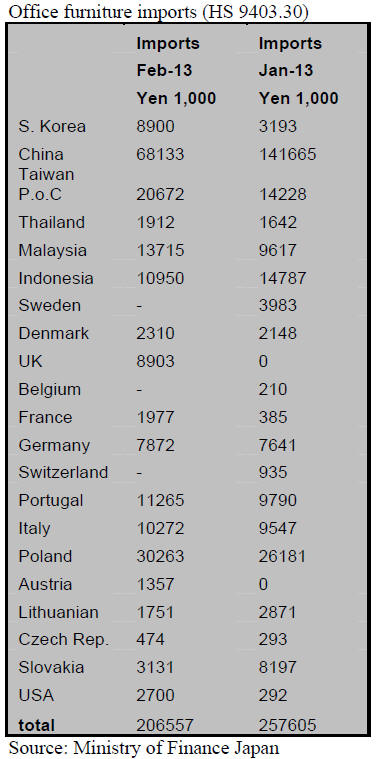

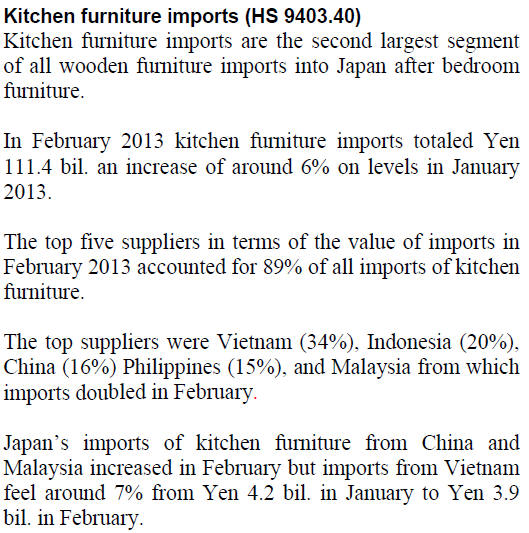

Japan Wood Products

Prices

Dollar Exchange Rates of

12th April 2013

Japan Yen

98.41

Reports From Japan

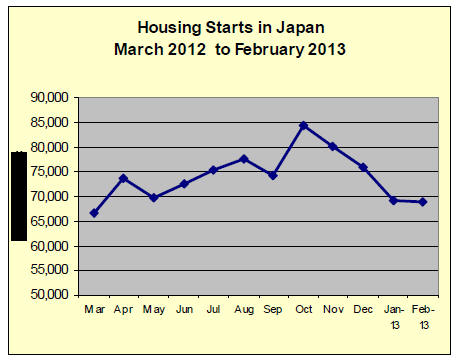

February housing starts better than forecast

Housing starts in Japan increased at a slower pace in February, marking the

fourth month of reduced growth. Housing starts rose 3.0 percent in February

2013 compared to levels in the same month in 2012.

Despite the decline in the pace of growth February figures were better than

the expected 2% decline but worse than the 5.0% year on year rise in housing

starts reported in January this year.

The better than expected numbers were the result of improved consumer

sentiment, low interest rates and firm demand as home owners try to beat the

planned sales tax increase due some time next year.

Major house builders reported that orders in February rose over 16% compared

to February 2012.

For the complete housing data see the Construction Research and

Statistics Office Policy Bureau, Ministry of Land, Infrastructure, Transport

and Tourism website at:

http://www.mlit.go.jp/toukeijouhou/chojou/stat-e.htm

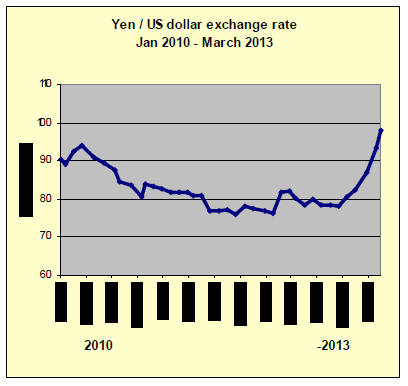

Yen continues its slide against major currencies

On 8 April the yen fell to 99 to the US dollar, its lowest in almost four

years. The steep drop in the value of the yen surprised markets and was

driven by an immediate buying spree by the Bank of Japan (BoJ), sweeping up

debt issued by the government.

The BoJ began its debt buying on 8 April, purchasing almost US$16 billion in

its first phase of its stimulus plan. This move by the BoJ will ensure that

borrowing costs remain low.

The yen fell to new lows against major currencies in the first week of April

almost testing the 100 yen to the US dollar mark.

However, every fall in the value of the yen pushes up the cost of

imported fuel and this poses a risk to domestic demand as almost all fuel is

imported. Almost all nuclear power plants in Japan have been shut down for

safety checks after the recent disaster.

When the yen 100 level is crossed analysts expect profit taking which could

slow the depreciation of the yen but probably not for long.

For a sustained weakening of the yen there would need to be decisive moves

by Japanese institutional investors to start buying higher-yielding assets.

A suggestion that this has begun is the yield on some European bonds which

have fallen.

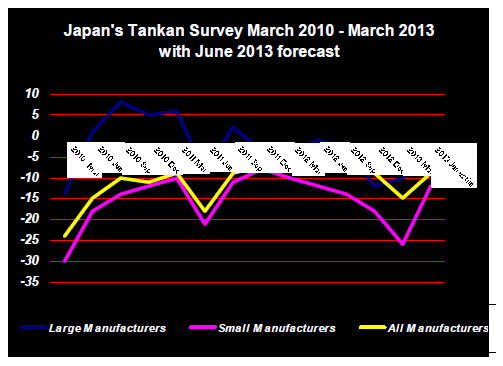

Business sentiment improves but less than expected

The Bank of Japan (BoJ) released its first quarter 2013 Tankan survey on 1

April.

The Tankan is an economic survey of Japanese businesses used by the BoJ to

decide monetary policy. The survey results are issued four times a year in

April, July, October and mid-December.

The survey reports views on prospects derived from around 10,000 companies

with a specified minimum amount of capital, although firms deemed

sufficiently influential may also be included.

The companies are asked about current business trends and conditions as well

as their views on future investment and sales.

Overall, business sentiment improved in the January to March quarter but the

improvement was less than expected, highlighting the challenge facing the

Japanese government as they try to revive economic growth.

The index for big manufacturers remains negative but improved from minus 12

in December to minus 8 in the latest survey. A negative figure indicates

that private sector pessimists outnumber optimists.

Analysts had forecast a substantial improvement in business sentiment

amongst the large manufacturers anticipating an index improvement to -1 for

the Jan-Mar quarter but the latest data suggest that even in the second

quarter the pessimists will outnumber the optimists.

Weaker yena boost to exporters

The new government and the central bank have taken various steps to try and

revive domestic demand and weaken the yen. Analysts say these moves helped

improve company profit outlook for large sized businesses and boost

sentiment.

This is the first survey since the government and BoJ adopted aggressive

policies to lift the economy out of recession. While these moves have helped

business sentiment and the weaker yen is providing a boost to exporters

business remain cautious.

The survey reports that large firms plan to reduce capital investment in the

current financial year and this is interpreted by analysts as suggesting

business leaders are yet to be convinced that domestic demand will improve

or that the risk of external shocks has diminished.

Small companies yet to feel benefit of stimulus measures

For small manufacturers sentiment remains very negative. The small companies

included in the survey anticipate an even larger reduction in capital

investment than the larger companies.

The slow pace of improvement in business conditions in the private sector

reflects fears that the economic stimulus measures being proposed by the

government and BoJ will be slow to arrive. Adding to the concerns of

businesses is the unsettled global economic outlook and the continuing stain

in Sino-Japanese relations.

The disappointing results of the Jan-Mar 2013 Tankan influenced the bold and

unprecedented moves by the BoJ which, at its last meeting, announced further

wide ranging monetary easing measures.

If pessimism dominates the next Tankan it will be very difficult for the BoJ

to achieve the 2 percent inflation target it has set as succeeding with this

would require companies to increase investment and wage levels.

Many analysts, including the previous BoJ governor say that stimulus

measures alone will not end 15 years of deflation and that structural reform

and deregulation must be addressed also.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade journal published every

two weeks in English, is generously allowing the ITTO Tropical Timber Market

Report to extract and reproduce news on the Japanese market.

The JLR requires that ITTO reproduces newsworthy text exactly as it appears

in their publication.

For the JLR report please see:

http://www.n-mokuzai.com/modules/general/index.php?id=7

Plywood supply in February

Total supply of plywood in February was 494,200 cubic metres, 3.1% more than

the same month a year ago and 7.3% less than January. This is the first time

that the supply dropped below 500,000 cubic metres in five months. This is

due to decline of imported plywood by about 40,000 cubic metres.

Imported plywood in February was 284,200 cubic metres, 2.0% more than

February last year and 12.5% less than January. In particular, the volume

from China dropped by 25,500 cubic metres from January, 32.1% less than

January because of delayed shipments by Chinese New Year holidays.

Average monthly import volume for last twelve months is 293,300 cubic metres.

Decline of import from Malaysia and Indonesia is result of log shortage in

rainy season.

Plywood suppliers in both countries reduce offer volume and meantime

Japanese buyers reduce purchase volume due to high offer prices.

Domestic production in February was 215,000 cubic metres, 4.6% more than

February last year and 0.6% more than January, out of which softwood plywood

was 197,200 cubic metres, 5.0% more and 1.0% more.

Monthly production volume exceeded 190,000 cubic metres for six consecutive

months. The shipment of softwood plywood was 204,900 cubic metres, 30% more

and 6.9% less.

The monthly shipment volume exceeded 200,000 cubic metres for five straight

months. The inventories are 127,600 cubic metres, 7,600 cubic metres less

than the inventories at the end of January. This is the lowest since October

2011.

Domestic made softwood plywood has been moving well despite demand slow

winter months so dealers had been making speculative purchase since late

December but it finally simmered down in late March. Until the inventories

dealers carry are digested, there won’t be much active purchase but total

inventory level remains low.

At the end of February, the softwood plywood inventories were 127,600 cubic

metres, lower than monthly consumption of about 200,000 cubic metres and

this is the lowest since October 2011 so the supply and demand balance will

be held for some time.

The manufacturers eased stiff sales policy after speculative purchase was

over. Current prices of JAS 12 mm 3x6 are 890-900 yen per sheet delivered,

40 yen up from March.1,790 yen on 24 mm 3x6, 90 yen up and 1,300-1,330 yen

on 9 mm 3x10, 50-80 yen up.

On imported plywood, speculative purchases were over and the market prices

stay in high level. The prices shot up sharply since late January by rapid

depreciation of the yen then the suppliers’ export prices also climbed

because of log shortage and high log cost.

This induced speculative purchases by the dealers then delayed arrivals in

late March eased tightness of supply.

The market prices in Tokyo region are 1,080-1,100 yen on 3x6 JAS concrete

forming, 30-100 yen up from March. 1,180-1,200 yen on JAS coated concrete

forming, unchanged from March. 1,100 yen on structural 12 mm 3x6, same as

March.

House builders flush with orders

Major house builders have ample orders in February. Low mortgage interest

rate, recovery of stock market and gradual rise of property prices seem to

stimulate housing demand. More people are visiting house exhibition sites

and people think this is time to buy house.

This is nothing to do with consumption tax increase in April next year so as

long as economic recovery continues, housing demand seems to stay active

even after the tax is raised.

|