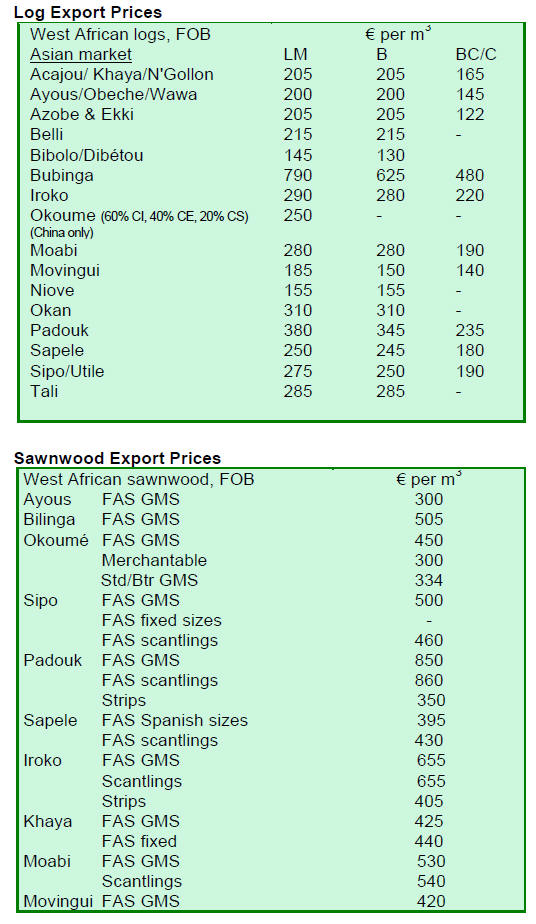

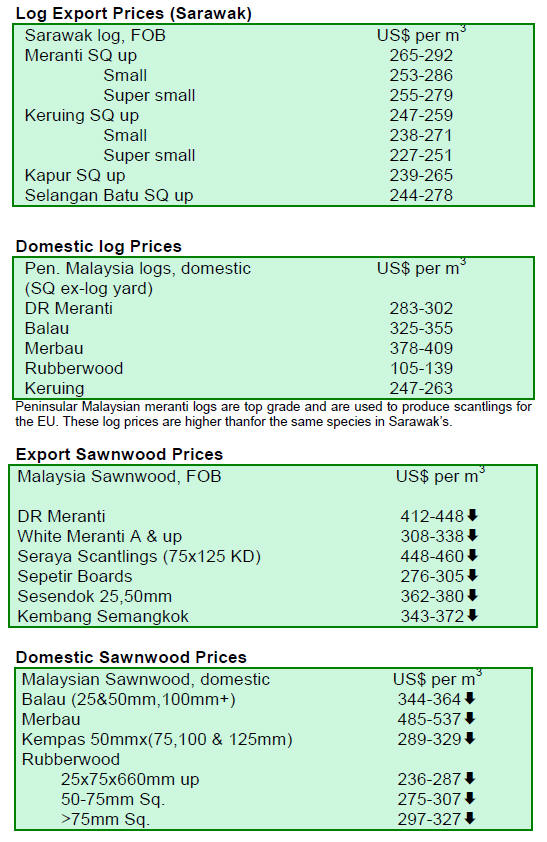

Export prices for logs and sawnwood remain stable. The

doubts expressed by exporters in August and September

this year that the prices being obtained for certain species

were likely to fall back to the previously established levels

did not materialise.

2.

GHANA

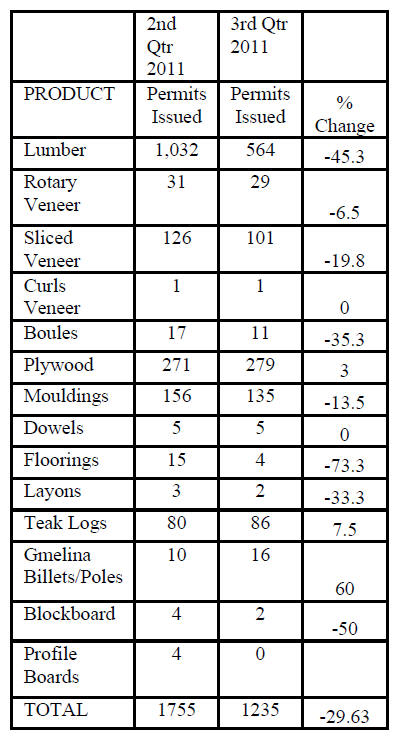

Export permits drop by a third in July-September period

A total of 1,235 export permits were processed, approved

and issued by the Timber Industry Development Division

(TIDD) during the third quarter, covering shipments of

timber and wood products through the ports of Takoradi

and Tema, as well as overland exports to neighbouring

ECOWAS countries.

The Table below summarises the number of export

permits issued by product during the second and third

quarter of 2011.

The number of permits issued in the third quarter declined

by almost 30% compared to the previous quarter.

The number of permits issued in Kumasi fell drastically

from the previous quarter figure of 622 to just 155. This,

say local analysts, could be due to the TIDD exercise of

eliminating chainsaw lumber exports which go mainly to

neighbouring countries.

The number of permits issued for Kumasi shipments to

neighbouring countries dropped from 519 in the second

quarter to 54 in the third quarter.

The highest number of export permits issued was for

sawnwood shipments which accounted for 45% of the

total number of export permits issued during the quarter

under review. Permits for plywood export were the second

highest.

Regional, Middle East and Asian markets sustain price levels

During the third quarter of this year the TIDD processed

and approved contracts for the exports of sliced veneer,

mouldings and celtis sawnwood meant for the West

African market.

Mouldings produced from species such as wawa, koto,

otie, utile, ofram and walnut were shipped to Nigeria.

Contracts for exports of sliced veneer to the Ivory Coast

and celtis sawnwood for Senegal were approved.

During the third quarter exporters were able to meet the

Minimum Guiding Selling Price (GSP) for plywood

destined for the West African market, especially Nigeria.

Most export contract prices were well above the GSP. The

TIDD data shows that prices for wawa sawnwood

contracts for Far and Middle East countries improved from

levels recorded recently.

Firm demand at low prices an issue in the US market

In contrast, exporters of mahogany sawnwood to the US

market were, with a few exceptions, unable to satisfy the

GSP. The gap between the contract price and the GSP in

the second quarter was around 3-7%. However, in the third

quarter the difference between the price being offered by

US buyers and the Ghana GSP widened to 7-11%.

Ghana¡¯s under utilised species such as celtis, yaya and

denya continued to find markets in the Middle and Far

East countries. Shorts of denya sawnwood continue to

attract buyers for the Chinese market.

Ghana¡¯s exports to the US boosted by African Growth

and Opportunity Act

Ghana¡¯s exports of all products to the US doubled during

the period September 2010 to September 2011 according

to the US International Trade Commission (USITC) which

uses statistics data provided by the US Department of

Commerce to compile country reports.

This performance was aided by the US ¡®African Growth

and Opportunity Act¡¯ (AGOA). The data show that

Ghana¡¯s export under the AGOA (including the GSP)

increased from US$31.1 mil. September 2009- 2010 to

US$195.7 mil. over the same period up to September

2011.

Ghana¡¯s main exports to the US market comprised

agricultural products, forest products, textiles and apparel.

3.

MALAYSIA

Investment in furniture production will bring

substantial benefits to Sarawak

The Ministry of International Trade and Industry is urging

the timber sector in Sarawak, as the state with the largest

timber resource, to consider expanding investment in the

furniture industry. This, says the Ministry, could lead to a

higher return on investments.

The Ministry added that, while Malaysia exported RM8

billion worth of furniture in 2010, Sarawak¡¯s share was a

mere RM20 million of the total.

The Sarawak Timber Industry Development Corporation

(STIDC) hoped that its planned establishment of extensive

plantations will provide resources for the furniture

industry in Sarawak to take off.

Risk of credit squeeze looms in Malaysia and across Asia

According to Nomura International (Hong Kong) Ltd, the

Malaysian economy is expected to recover in the second

half of 2012 and fourth quarter 2012 growth of up to 7.3%.

Growth in the third quarter 2011 is projected at 5.8% and

fall to around 4% in the final quarter of the year.

The exposure of Malaysian banks to European banks

reportedly stood at US$50 billion in June 2011 excluding

investments by HSBC and Standard Chartered baks, both

of which have significant operations in Malaysia.

European banks with large overseas exposure may tighten

credit lines and lessen their exposure in Asia which could

lead to tighter credit conditions and net capital outflows

from Asian countries.

Government spending led growth may be

unsustainable in the long term

The current GDP growth achieved in Malaysia was driven

by public sector investment with one-third of this coming

from direct government spending. This, say analysts is

unsustainable in the long term.

As a result there is not much room for expansionary fiscal

policy in Malaysia for 2012 due to the relatively high

public-debt-to-GDP ratio of 55%, the second highest in

Asia.

The outlook for the Malaysian timber industry in 2012

remains uncertain as prices of timber and wood products

remain weak mainly because of poor housing starts in

major export markets.

4.

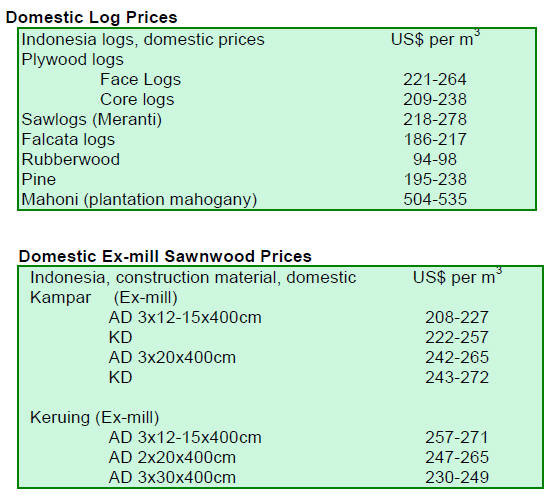

INDONESIA

Risk of dispute looms peatland boundaries are

adjusted

Indonesia is revising the boundaries of the peatland

defined in the moratorium agreed with Norway. Reports

suggest that some 4.8 million ha. of peatland will be

removed from the area of 10.7 million ha. previously

defined as protected in the original moratorium.

Compounding the chances of a dispute on areas covered

by the moratorium is the decision by the Governor of

Aceh province to allow an oil palm plantation to be

established in an area which, say opponents, is a protected

peatland.

Weak global demand for Indonesian products will

eventually affect Indonesian domestic economy

The housing markets in major timber importing countries

continue to weaken and the EU debt crises continues to

bear upon international trade opportunities. These factors,

amongst others, are causing export prices for Indonesian

timber products to spiral downwards reaching their lowest

in 2011.

While the Indonesian domestic economy has remained

stable, analysts are of the opinion that it will not be long

before the weak global demand for Indonesian products

begins to affect the local economy.

Exporters call for aggressive timber export

promotion

Indonesian timber exporters have expressed the view that

there is a need for the timber industry and Indonesian

government to formulate strategic programmes to boost

the export of timber products.

Some timber exporters added that, while there are

ongoing

efforts, more aggressive programmes and planning are

needed to cushion and safeguard the Indonesian timber

industry in the short-term while solutions to the US and

EU debt crises are negotiated.

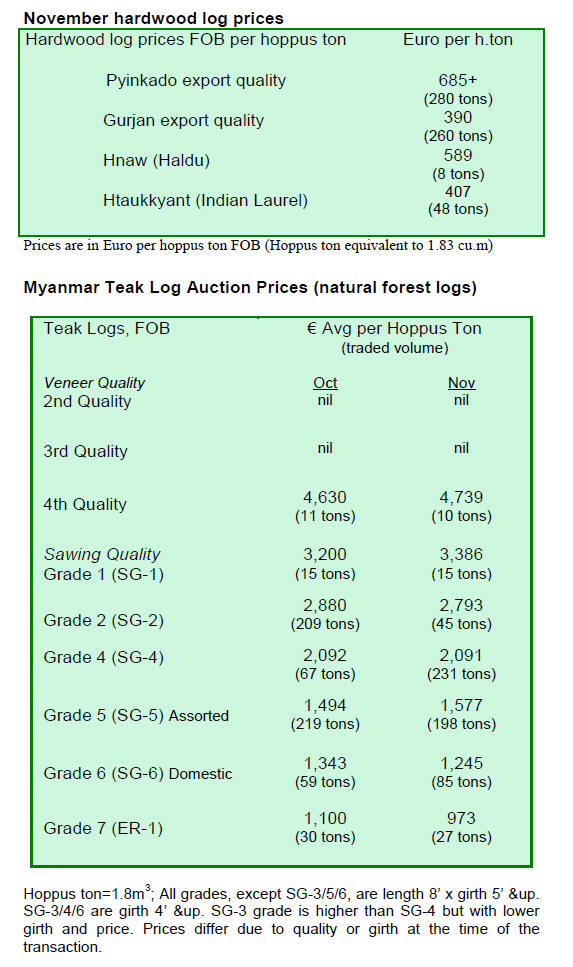

5. MYANMAR

2011 has not been a very good year for the

Myanmar

timber industry

In reviewing the year analysts say, compared to 2010,

2011 was not a very good year for the timber trade.

While demand for teak held up reasonably well,

demand

for pyinkado was very weak throughout the year.

Prices for pyinkado started to show signs of

weakness in

late 2010 and this continued throughout 2011.

Analysts say the price levels for pyinkado are set

too high

and do not reflect current interest in this timber or the

economic realities in the importing countries.

Another factor which disrupted trade was the

weather.

Early rains in April this year made transportation of logs

difficult and caused a supply shortage in the Yangon log

yards.

The market for lower priced gurjan (kanyin) logs,

which

was not active during 2010, made a slight recovery in the

second quarter only to weaken again in September and

October.

The slowdown in western economies has had a negative

impact on the demand from countries importing timber

from Myanmar.

Few prospects for a quick market turn-round

Demand in India, a major buyer of timber from Myanmar,

has been affected largely by the rapid depreciation of the

Indian rupee.

India is a main market for teak from Myanmar and in

this

market demand for teak began to weaken during the

second half of the year. As the year is about to come to an

end there are few prospects for an early recovery in

demand for teak, pyinkado and gurjan.

CIFOR statistics illustrate strength of demand

for logs in India

Myanmar¡¯s Central Statistical Organisation data reports

the export of logs from January to December in 2010 as

237,100 cubic tons of teak and 681,500 cubic tons of

hardwoods. The figures for the period January to

September 2011 are 185,400 tons of teak and 572,400 tons

of hardwoods.

Figures compiled by CIFOR for the year 2010 showed

China bought 0.4 million cu.m of logs valued at US$ 0.14

billion CIF and 0.1 million cu.m of sawnwood valued at

US$0.05 billion CIF from Myanmar. India¡¯s imports were

stated at 0.8 million cu.m of logs valued at US$0.31

billion CIF.

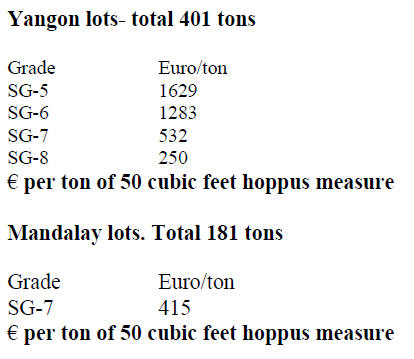

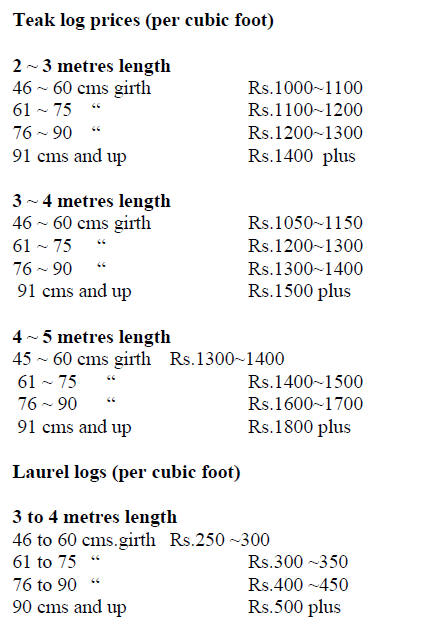

December teak log sales for local millers

concluded

The following are the results for tender sales of teak logs

for the local industries held on 9 December 2011.

Dates for December open tender for teak

The Myanmar Timber Enterprise open tender teak log

sales for December will be held on the 16th and the 19th of

this month.

6.

INDIA

Global economic downturn affecting

the Indian economy

India¡¯s GDP fell to a two year low of 6.9 percent in the

second quarter of this financial year, slipping below 8%

for the third straight quarter. The economy grew 8.4%

during the corresponding quarter of last year.

Simultaneously, the Indian rupee suffered its worst

decline

against the US dollar in 16 years. In November the

currency plunged almost 7 percent, pushing the

downward trend to over 14 percent for the year to date.

Dollar demand from importers and financial outflows,

as

investors reacted to growing risks, caused the slide. The

government and the Bank of India are acting to arrest this

situation and stabilise the rupee exchange rate.

Real estate sector performance slows

Analysts suggest that the shadow of the global economic

weakness will dent India¡¯s growth figures for a while.

The focus of domestic manufacturers will shift from

consumer demand in the mega cities such as Mumbai and

New Delhi to other newly developed cities.

Government investment in rural development projects

holds a better promise for industry than the weakening

demand in the traditional urban domestic markets.

Boom and bust swings in demand are a common

phenomenon and this provides an opportunity for the

industry to attend to production and distribution

weaknesses and to improve performance by delivering

higher quality products and better services.

The emerging so-called ¡®integrated townships¡¯ are

where

the future of India¡¯s manufacturing sector will be in the

future say analysts. The global economic weakness and the

undermining of consumer confidence have put a brake on

consumption by consumers in the high-end domestic

market.

The timber industry has to turn to the affordable

home

segment which was not given much attention while the

overall real estate market was booming. Housing demand

from middle and lower income groups will probably be the

driving force for the manufacturing industry from 2012

onwards.

Smugglers of Red Sanders become violent

Forest officials and wardens are facing increased violence

from timber smugglers.

The unresolved case of the death of a forest officer

in

Andhra Pradesh, the main producing area for red sanders,

is thought to be caused by the action of gangs stealing this

timber. This is the first time that a forest officer has been

killed pursuing thieves.

It is estimated that approximately 2,000 tons of

this

precious wood is being smuggled to other Asian countries

for the manufacture of herbal medicines, special musical

instruments and cosmetics.

In 2010-2011, 1,591 persons were arrested and a

total of

1,290 tons of red sanders was seized.

First hardwood auction in the Central Province

fetches

good prices

Harda, Jabalpur, Hoshangabad and Betul Forest Division

depots have just completed the first post Deewali auctions

for the current season and the dates for sales during

December have been set.

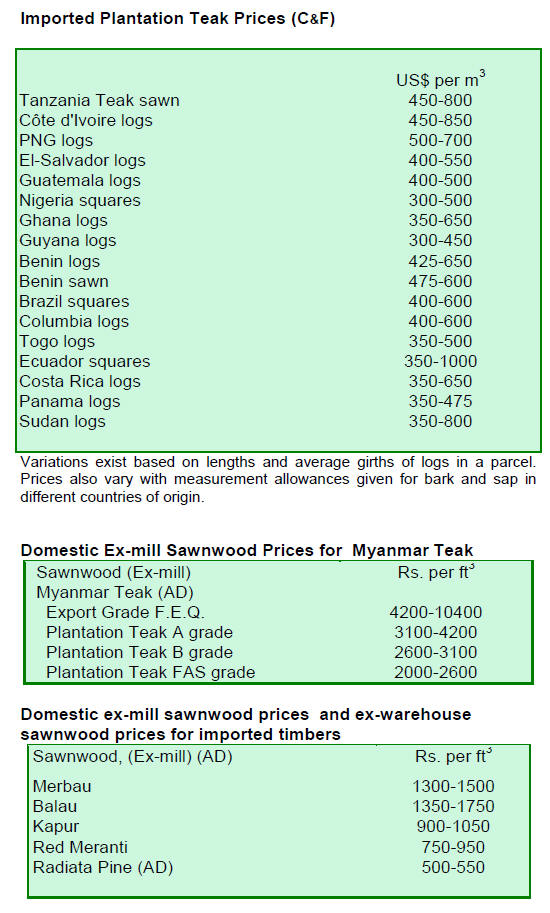

Approximately 20,000 cu.m of teak logs and 14,500

cu.m

of other hardwoods as well as bamboo and teak poles will

be sold at the upcoming auction.

At the recently concluded auction good demand

resulted in

high average prices for teak logs as shown below.

7. BRAZIL

Furniture hub in Cruzeiro do Sul attracts

investors

The establishment of an industrial hub in Cruzeiro do Sul

in the Amazon State of Acre is almost complete. The Acre

State government has invested about R$3 million in the

development of this industrial centre.

This investment, specifically for the wood

processing

sector, has attracted the attention of entrepreneurs from

other States.

Many industrialists are keen on this initiative in

Acre as

the state has two strategic road connections, one is

highway BR-364, which helped inter-state integration and

another is the convenient connection to ports on the

Pacific coast via the Trans-oceanic highway.

This new development makes Acre an attractive

location

for industrial development and new wood processing

operations are expected to open at the industrial hub.

The timber industry in Acre benefits from support

for its

operations, with its raw material supply is guaranteed legal

since it comes from community and publicly managed

forests or from private land covered by management plans.

Representatives of manufacturers in the hub are

appreciative of the investment by the state government and

the efforts of the government to invest in an industrial

sector.

Bright long term prospects for wood product manufacturers

Despite the current global economic downturn, countries

with primary raw material production capability have a

secured future. This has prompted the Brazilian Senate to

review the country¡¯s long term export strategy.

Analysts suggest that, taking account of global

trends, the

forestry and timber industries will have a bright future in

the coming years.

In September, Brazilian exports of wood products

were

valued at US$155 million, representing a 6.7% decline on

the previous month. Imports of wood products were

US$17 million, a sharp drop of 14.4% from the previous

month.

In order to be well prepared for the eventual

improvement

in global demand parliamentary initiatives, aimed at

creating the conditions for investment in added value

production, are said to offer prospects for a sound future

for the sector in the medium to long-term.

There is a proposal being considered by the

Brazilian

senate for a ban on the export of unprocessed wood. This

measure, if adopted, should encourage greater investment

in wood processing which, in turn would create more jobs

and increase export earnings.

Furniture output grows despite uncertainties in

global economy

The Brazilian furniture industries are worried that the

uncertainties in the global economy, mainly caused by the

crisis in the euro-zone countries, will continue to depress

demand. In addition exchange rate fluctuations have

resulted in Brazilian wood products loosing international

competitiveness.

Despite the international crisis, the furniture

sector

achieved positive growth in August mirroring trends in the

overall Brazilian processing industries. Furniture output in

August increased 12% compared to levels in August 2010.

However, furniture exports have been falling. For

the year

to-date Brazil¡¯s furniture exports were around US$337

mil., 12% lower than in the same period in 2010.

In contrast furniture imports have been growing due

mainly to the strength of the real. From January to August

2011, imports climbed 97% higher than in the same period

in 2010. However, in September there was a significant

drop in the level of imports reflecting the sharp

depreciation of the Brazilian real against the US dollar.

Measures by the federal government to assist the

furniture

sector such as investment in promotion, lowering interest

rates, and other measures to boost domestic demand

helped the furniture sector.

Wood Identification System could raise tax

revenues to state

The Mato Grosso Institute of Agricultural Protection

(Indea) participated in the First Wood Anatomy and

Identification Seminar in the Amazon, in Bel¨¦m, Par¨¢. The

main objective was to exchange experiences on the

establishment of wood anatomy and identification systems

and log scaling in the Amazon region.

In 2009, when the latest survey was conducted,

there were

71 wood processing centres in the Amazon region. These

centres were logging approximately 14.2 million cubic

metres annually. The states of Par¨¢, Mato Grosso and

Rondônia were the largest producers. Estimates of the

gross revenue generated by the Amazon timber industry in

that year were around R$4.9 billion.

Cost effective systems for anatomical

identification of

species is considered the most reliable means to ensure

that consumers receive the species they require. Correct

specie identification is also a tool to value products an

element in the process to secure certification from state

agencies.

If an easy to use wood identification system can be

developed it could, say analysts, result in higher state

timber tax revenues and help in protecting controlled

species as well as improving consumer protection.

¡¡

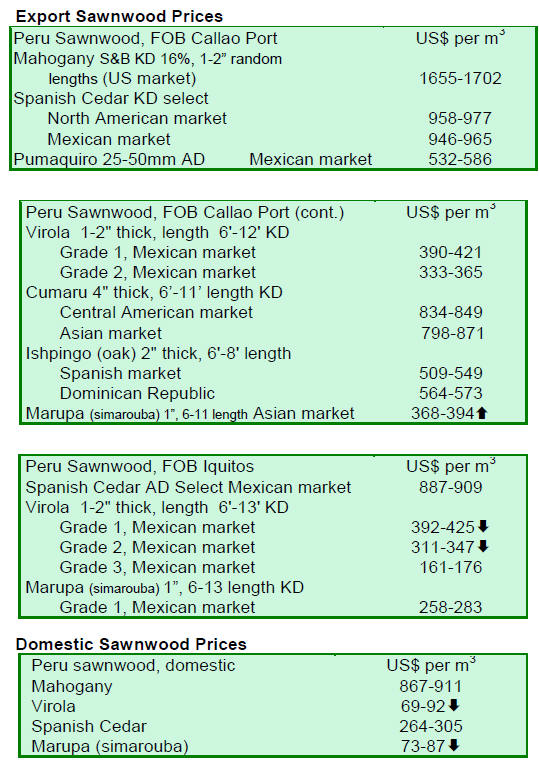

8. PERU

Peru¡¯s GDP growth may exceed

forecasts

Official data from the national authority, SUNAT, reveals

that the value of Peru¡¯s exports in the first 10 months of

the year rose by more than a third compared to levels in

the same period in 2010.

Analysts report that exports of traditional

products grew

by 75% while the so-called non-traditional exports grew

over 20%.

Foreign exchange earnings were derived mainly from

agricultural products, the oil and gas industries, the mining

sector (copper and gold) and the fisheries sector.

Economists are painting a rosy picture of prospects

for the

country¡¯s GDP growth suggesting that growth in 2011

could exceed government forecasts.

Peru stands to gain from Economic Partnership

Agreement with Jjapan

The Economic Partnership Agreement with Japan, which

was signed earlier this year, has been ratified and analysts

point out that this will benefit the textile and clothing

sectors as well as the forestry, agriculture and fishing

sectors.

This agreement provides for reduced tariffs on

Peruvian

products. Similarly, Peru will also benefit from

competitive Japanese products. From 2012 Peru will have

operational trade agreements with two of worlds the

largest economies namely Japan and China.

For more see www.andina.com.pe

¡¡

9.

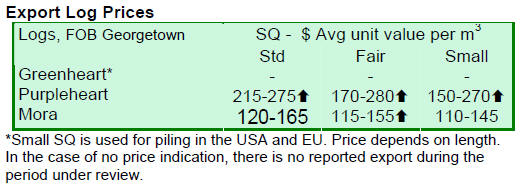

GUYANA

Mora and purpleheart logs

are the current favourites in

export markets

The weakness in demand for greenheart logs continues

and there were no exports of this product during the period

under review. Demand in the local market is stable and

there is continued processing of greenheart logs into added

value products to satisfy the housing market.

On the other hand, purpleheart logs are in demand

in

export markets and prices are favourable for all log

categories. The current price levels are higher than those

in the previous period of review.

Mora logs are also in demand and this translated

into

attractive and improved prices for all log categories

compared with levels in the previous period.

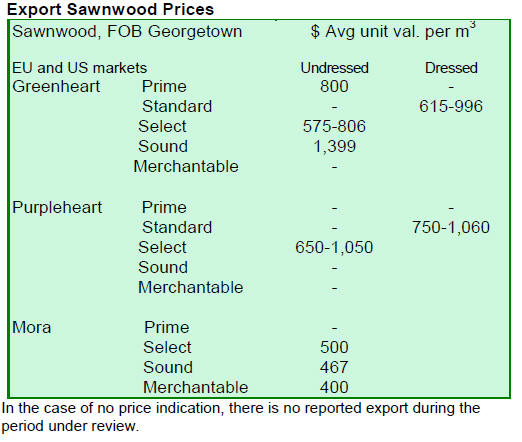

Firm European demand for sawn greenheart

surprises the trade

While demand for greenheart logs is weak the situation is

different for greenheart sawnwood. Undressed greenheart

sawnwood attracted good prices and rather surprisingly,

there was firm demand from major buyers in Europe,

Guyana¡¯s main market for greenheart.

Overall, prices for undressed greenheart sawnwood

are

holding for all categories except merchantable.

After a quiet period, undressed greenheart prime

quality

was in demand again on the export market and good prices

of US$ 800 per cubic metre were secured.

Select quality undressed greenheart was exported at

prices

from US$636 to US$806 per cubic metre, up on levels in

the previous period. On the other hand, exporters report

that prices for undressed greenheart sound quality fell

from US$1,509 to US$1,399 per cubic metre.

Prices for undressed purpleheart select quality

remain

unchanged while undressed Mora sawnwood prices were

favourable during this fortnight period with export demand

for all categories except prime quality.

During the period under review dressed sawn prices

were

mixed. Dressed greenheart prices fell at the top of the

range from US$1,350 to US$996 per cubic metre.

Dressed purpleheart prices, on the other hand, rose

significantly from US$912 to US$1,060 per cubic metre

for this period in comparison to the previous period.

Guyana washiba (ipe) in the form of dressed

sawnwood

attracted a remarkable price average of USD 2,500 per

cubic metre.

Guyana plywood was shipped to destinations in the

Caribbean and South America at prices as much as

US$600 per cubic metre.

Guyana¡¯s forestry sector falls under New

Ministry of Government

Following the 2011 elections in Guyana the Ministry of

Natural Resources and Environment responsible for the

forestry and mining sectors in the country has been

established.

The new ministry is currently headed by the former

Minister of Agriculture Mr. Robert Persaud and seeks to

harmonise policies in key areas of environment and

natural resources so as to increase development within the

natural resources sector.

This new ministry will be addressing a number of

issues

related to mining, environment, climate change and

forestry. Guyana has been actively engaged in

international dialogue to ensure and promote legal timber

production and sustainable forest management and work

on this will be enhanced.

Progress on the implementation of the Guyana

Legality Assurance System

The Guyana Legality Assurance System framework falls

within the mandate of the new ministry in maintaining the

legality aspect within forestry.

The Guyana Legality Assurance System has recently

undergone rigorous review/audit by international bodies to

assure its transparency and acceptance internationally.

A progress report on the implementation of the

system was

recently handed to the then Minister of Agriculture (now

the new Minister of Natural Resources and the

Environment). Implementation of this system is expected

to make further progress in 2012.

Related News: