|

Report

from

Europe

Slow recovery in EU imports of tropical hardwood logs

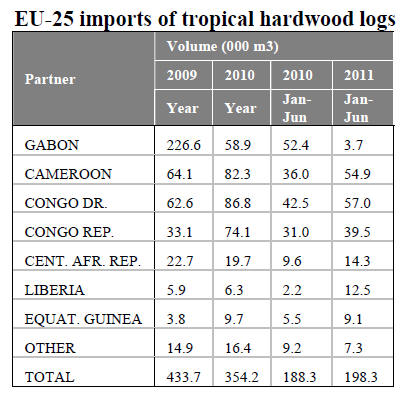

During the first half of 2011, the EU imported 198,300

cu.m of hardwood logs from tropical countries, a 5%

increase compared to the same period in 2010.

As natural forest logs can no longer be exported from

Gabon, EU imports from all the other main producing

countries in the Congo region increased dramatically

during the first 6 months of the year.

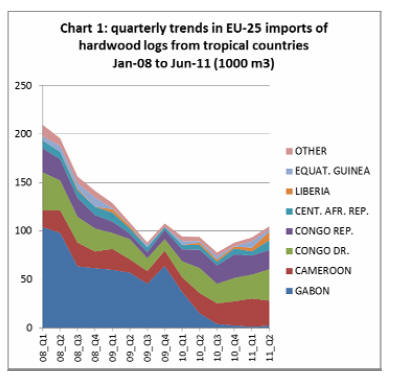

EU imports of tropical hardwood logs in the second

quarter of 2011 reached 105,000 cu.m. Quarterly imports

have risen now for three consecutive quarters, recovering

from a low of only 78,000 cu.m imported in the third

quarter of 2010.

However as shown below EU quarterly imports of tropical

hardwood logs over the last three years that imports of this

commodity are only 50% of levels recorded in early 2008.

There are various reasons for this including the economic

recession in Europe, Gabon’s log export ban from May

2010 and the significant recent decline in okoume

plywood manufacturing in France.

Shipments of tropical hardwood logs to Europe during the

second half of 2011 are unlikely to show any significant

improvement. Buying was slow to pick up at the end of

the European holiday season in September.

Consumption is so slow that there are few reports of

significant delays in deliver to end-users despite

continuing reports of delayed shipments from African

suppliers.

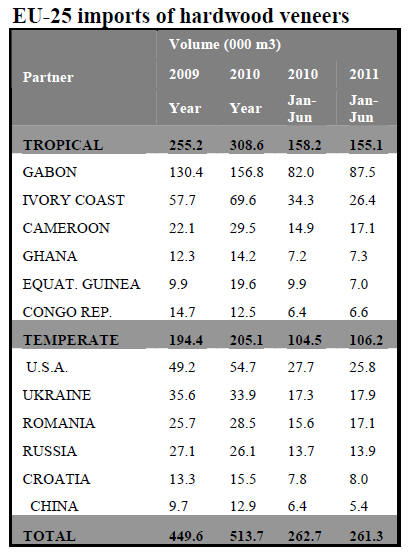

Decline in log imports not off-set by increased veneer imports

The following table shows recent trends in EU-25 imports

of hardwood veneer and indicates that the decline in EU

imports of tropical hardwood logs has not yet been offset

by an increase in imports of tropical hardwood veneer.

EU imports of this commodity reached 155,100 cu.m in

the first six months of 2011, down 1.9% compared to the

same period in 2010. A slight increase in imports from

Gabon and Cameroon was more than offset by a large

decline in imports from Ivory Coast and Equatorial

Guinea.

On a more positive note EU imports of tropical hardwood

veneer, particularly from Gabon, rose sharply in the April

to June 2011 period after a very slow start to the year.

It remains to be seen whether recent efforts to increase

investment in Gabon’s wood processing sector will lead to

this becoming a sustained trend.

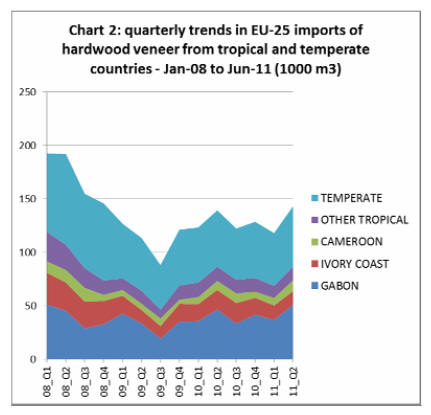

The relative stability of EU imports of hardwood veneer

during 2011 masks deeper processes of on-going structural

change in the sector. The reality is that there is

considerable uncertainty about longer term market

prospects which is encouraging a conservative approach to

purchasing.

The European market for rotary veneers of tropical

hardwood appears to be in long-term decline as okoume

plywood manufacturing operations in Europe have closed

and okoume plywood has come under intense pressure

from cheaper products (particularly combi-products) from

China comprising a poplar core and decorative hardwood

face veneer.

Meanwhile, demand for high quality tropical hardwood

sliced veneers has been hit by a combination of factors.

European manufacturers are increasingly switching to

domestic hardwoods to reduce costs and supply chain risks

in a market where nobody wants to be caught holding too

much stock.

This trend has gone hand-in-hand with improvements in

treatment technologies allowing even the blandest of

temperate hardwoods to produce a diversity of looks and

finishes.

The most recent data from Germany, traditionally the

centre of the European veneer trade, gives some indication

of how far this trend has progressed. The latest survey of

the German veneer industry by GD-Holz suggests that

European hardwoods now account for 63% of veneer

manufacturing, up from 56% last year.

This year oak (both European and American) makes up

38% of total production, with beech, maple and walnut

contributing a further 23%, 9%, and 8% respectively.

Tropical hardwood currently accounts for around 15% of

German veneer production.

At the same time, all sliced wood veneers continue to

come under pressure from non-wood substitutes and from

weak consumption in major end-using sectors. Despite

concerted marketing efforts by the European veneer

sector, European furniture and door producers are still

shifting to non-wood alternatives.

These losses have only been partly off-set by gains made

in sales to the interior fittings market (floors and

edges/borders) and higher value niche markets such as

yachts, cars, and airplanes.

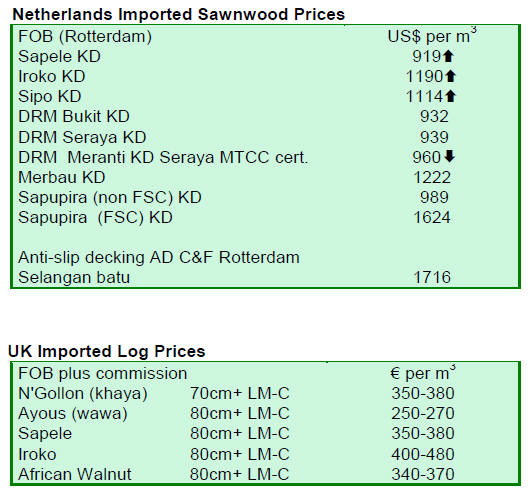

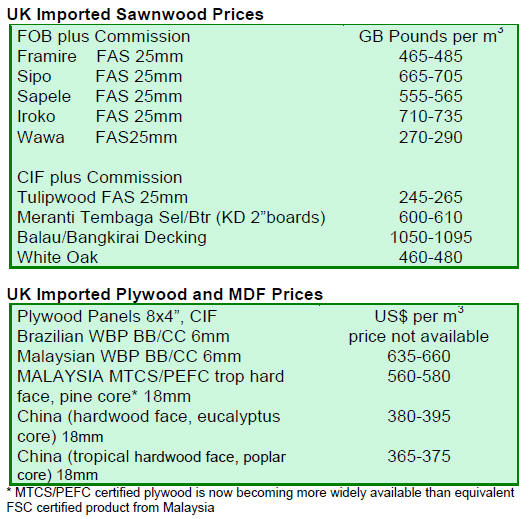

Hardwood plywood prices weaken as supply pressures ease

Availability of South East Asian plywood for forward

shipment to Europe has improved in recent weeks. The

supply problems that arose for European importers early in

the year following the Japanese Tsunami have now eased.

Although the log supplies to mills in Indonesia and

Malaysia remains at relatively low levels, they are now

reportedly sufficient to meet current subdued levels of

demand. The slight improvement in log supply has

coincided with slower consumption in Japan and

continuing weak demand in Europe and North America.

Some mills in Malaysia are now offering BB/CC grade

plywood to European buyers at lower prices than in

September. However quality is now quite variable

between Malaysian mills.

Prices for Indonesian plywood have remained more stable,

but supply pressures are now less pronounced and lead

times for some Indonesian products for delivery to Europe

have fallen to around 5 weeks.

Demand for Chinese plywood in Europe remains slow.

The UK is quite heavily stocked relative to current levels

of subdued consumption so that forward buying has been

slow in the autumn months.

The German trade journal EUWID reports that

consumption of Chinese hardwood plywood in Germany is

so slow that some merchants have introduced promotional

offers on their existing stocks.

EUWID reports that Chinese exporters have pushed up

FOB prices for hardwood plywood in response to rising

labour and raw material costs. However, this has been

offset for European buyers by falling freight rates.

Related News:

|