2.

GHANA

More sawnwood export permits issued in second quarter

According to a Timber Industry Development Division

(TIDD) report, 1,755 export permits were processed,

approved and issued to exporters during the second quarter

of 2011 for the shipment of timber and wood products

through the ports of Takoradi and Tema as well as via

overland routes to neighbouring ECOWAS countries.

Compared to approval levels during the previous quarter

the second quarter results were up almost 12%.

Sawnwood continues to account for the highest number of

export permits issued at almost 60% during the quarter

under review. Plywood export approvals were the second

highest accounting for around 15% of the total permits

issued.

A total of 778 permits were approved for the exports of

sawnwood, plywood and blockboard by road to Nigeria,

Niger, Benin, Mali and Togo during the quarter under

review. The total permits issued for overland export

showed an increase of 31% when compared to the figure

achieved during the previous quarter.

Permits issued for overland export totalled 43,021cu.m (up

10.5%) and these exports generated earnings of Euro 9.30

million compared to the previous quarter.

10,000 hectares targeted for 2011 plantation programme

Reports show that in 2010 a total of 20,200 hectares was

planted with various species of trees under the National

Forest Plantation Programme. In total some 67,000

hectares have been planted since 2002.

Nana Poku Bosompim, the Assistant District Manager of

the Forest Services Division, said this at Attakrom during

a visit to the Sui River Forest Reserve by members of the

Parliamentary Select Committee on Lands and Forestry.

He said the target for 2011 is a further 10,000 hectares to

ensure the continued expansion of plantation forests in the

country.

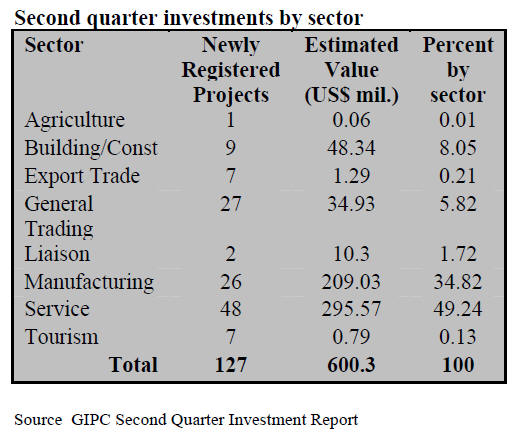

GIPC targets US$1.5 bil. non-oil investments

The Ghana Investment Promotion Centre (GIPC) has said

its target for 2011 investments is US$1.5 billion.

Investment promotion by GIPC continues to yield positive

results as reflected in its performance for the 2nd quarter.

In the quarter, 127 new non-oil projects were registered;

an increase of 21% compared to the same quarter of 2010.

The estimated total value of the registered projects for the

quarter was just over US$600 million.

Total initial capital transfers for newly registered projects

during the quarter amounted to US$97.03 million.

The FDI component of the value of the projects in the

quarter was US$552 million, or 92% of the total.

The total number of jobs expected to be created for

Ghanaians from the projects registered in the second

quarter is around 6,700 while expatriate employment is

expected to total 735.

China, with 23 projects, topped the list of countries with

the highest number of registered projects. However, with

US$128 million in estimated value of investments, the

Netherlands topped the list in terms of value of

investment.

Ghana¡¯s timber manufacturers are currently seeking

business ventures with international partners in order to

upgrade manufacturing in the country, to improve

management practices and increase the range of products

offered. Opportunities for investment exist in the

following product areas:

• Finished and semi-finished furniture and

components;

• Mouldings and machined wood;

• Floor and deck blanks, strips and blocks;

• Door, window, and cabinet frames and panels;

• Dowels and tool handles;

• Peeled and sliced veneers;

• Kiln dried rough or machined lumber.

It is estimated that there are 400,000 hectares of land

currently available within Ghana¡¯s degraded forest

reserves that can be converted to commercial forest

plantations.

In addition, there exist a large number of over mature

cocoa farms and degraded areas outside reserve areas that

are also suitable for plantation development.

http://www.gipc.org.gh/pages.aspx?id=84

3.

MALAYSIA

Malaysia aims to maintain furniture exports at 2010

levels

Malaysia¡¯s exports of wooden furniture in 2011 are

expected be no higher than the RM6.5 billion achieved in

2010 as continued uncertainty in the global economy

weighs on the timber manufacturing and export sectors.

The appreciation of the Malaysian currency against the US

dollar and competition from new players such as Vietnam

are also affecting the confidence on the part of wooden

furniture exporters.

Cutting costs by means of more advanced machining technologies

The Ministry of Plantation Industries and Commodities

voiced the opinion that the adoption of more advanced

machining methodologies would help cut production cost

while maintaining a leading edge for the Malaysian

wooden furniture industry.

The Malaysian government has indicated its commitment

to continue providing soft loans for investors in the forest

plantation sector and will continue to vigorously support

the Malaysian Timber Certification Scheme so that it

becomes even more widely accepted internationally.

MTIB reassesses 2011 timber sector forecasts

The Malaysian Timber Industry Board is reviewing its

forecast for 2011 timber exports. Malaysia¡¯s exports of

timber and timber products amounted to RM20.52 billion

in 2010 but analysts report the likelihood is that total

exports for 2011 may be lower than those in 2010.

In contrast, demand in the domestic market remains

buoyant for the time being. Domestic consumption of

wood products is estimated to be worth around RM20

billion, out of which sawn timber accounts for just over

RM10 billion, furniture RM4 billion, plywood and other

panels RM4 billion, joinery products RM1 billion and

other timber products the remainder.

MTC to hold International timber marketing conference

The Malaysian Timber Council (MTC) will organize an

International Timber Marketing Conference in conjunction

with the fourth Malaysia International Commodities,

Conference and Showcase 2011 due to be held at the

Malaysian Agro Exposition Park Serdang on October 28th

this year.

Speakers from the USA, Europe, India, Hong Kong and

the UAE will be present to provide insights into the global

timber industry and trade. A consultation and marketing

¡®clinic¡¯ will also be held for the Malaysian industry on

October 31 with regional directors and market

correspondents and consultants in attendance. For more

information see

http://www.mtc.com.my/trade/

4.

INDONESIA

Counterfeit furniture deceiving

Indonesian consumers

says ASMINDO

The Indonesian domestic furniture market is worth around

USS$700 million according to the Indonesian Furniture

Entrepreneurs Association (ASMINDO). In a recent

statement ASMINDO has suggested that the domestic

market is being undermined by imports of fraudulently

labelled furniture.

To address this ASMINDO has urged the government to

tighten rules and regulations governing furniture imports

in order to offer some protection to the local furniture

industry especially from mislabelled imported furniture.

ASMINDO says it has uncovered instances of falsified

labelling and mislabelling of imported furniture after

investigating the origin of some products and the business

practices of some importers.

The government has been asked to take the necessary

steps

to make it mandatory for imported furniture be supported

by an authentic certificate of origin.

ASMINDO cited a few cases where European style

furniture with a ¡°Made in Europe¡± label was actually

manufactured in an Asian country.

The counterfeit furniture can be sold at a high price on the

domestic market, thereby deceiving the consumers.

Options mulled to detect counterfeit furniture

The head of the business unit at the Directorate of Wood

and Plantation-based Industries at the Indonesian Industry

Ministry added that it will act to put a stop to counterfeit

furniture imports.

However, the Ministry is yet to implement inspection

procedures for imported furniture. The ministry proposed

that imports of furniture be limited only to certain ports, as

is the case with the imports of food and beverages as this

will facilitate inspection.

Other options include the use of certificates of origin

to

verify the origins of products.

UK welcomes Indonesia¡¯s signing of VPA

In a press release the UK¡¯s Defra (Department for

Environment, Food and Rural Affairs) has praised the

work to tackle illegal logging with the news that Indonesia

has become the fifth country to sign a voluntary

partnership agreement (VPA) with the EU.

The press release says Indonesia is leading the way in

Asia

and has one of the biggest areas of forest in the world. Six

countries have now signed agreements with the EU, and

another four are in negotiations.

The UK Government is helping developing countries to

prevent the loss of forests as part of wider efforts to help

them both adapt to the impacts of climate change whilst

continuing their economic development.

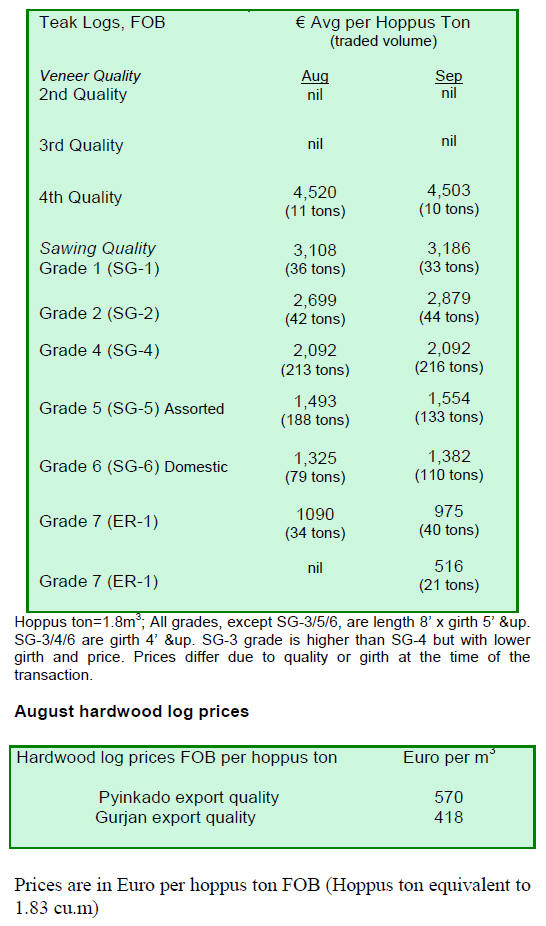

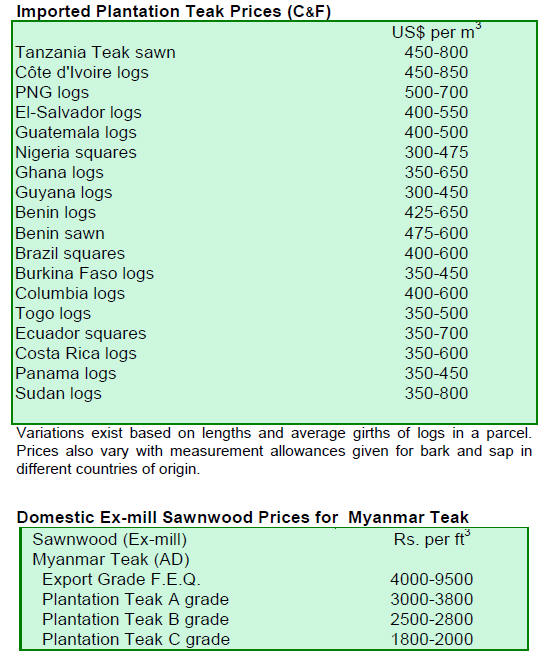

5. MYANMAR

Sale of old stock Teak logs in September

In mid September there was a further ¡®Special Open

Tender¡¯ for 920 h.tons of old stock teak logs of various

grades (SG7, SG8 and SG9) as well as some teak

thinnings held by the Myanma Timber Enterprise.

In total 904 h.tons were sold. Teak logs of SG7

grade were

sold at an average of Euro 552 per h.ton while grade SG8

logs fetched Euro 215 per h.ton. Thinning Posts, as the

thinnings are termed locally, were sold at Euro 108 per

h.ton.

Teak prices ease on news of high stocks in India

Over the past weeks analysts have noticed a weakening of

the market for teak logs. Reports suggest that stocks of

Myanmar teak logs in India are rather high and has led to a

decline in orders.

Also, the Indian Rupee has weakened from Rupees 44

in

April to almost 50 to the US dollar at present and some log

dealers reported that buyers are reluctant to open new

letters of credit fearing further currency fluctuations.

Demand for Pyinkado remains weak as in previous

months

and analysts report that demand for Kanyin (Gurjan) has

also weakened. Kanyin sales normally drop after the

Myanmar New Year in April but demand was sustained

this year as early monsoon rains hampered the transport of

logs to Yangon and this created firm demand for a longer

period than usual.

Planning for more added value production

The Yangon Times has reported that the Myanma Timber

Enterprise has decided to reduce log extraction by 50%

prior to the establishment of the ASEAN Free Trade Area

in 2015. But this has not been officially announced.

A reduction of 20% is projected to start in 2012

followed

by a further 30% reduction in 2013 to reach the target of a

50% reduction by 2015.

According to the Chairman of the Timber Merchants¡¯

Association, during the years up to 2015 the wood

industry must be reorganised for production of more

value-added products to make up for the shortfall in export

earnings.

The Yangon Times also reported that in order to

ensure

the flow of logs to domestic industry a monthly open

tender will be held by MTE. Reports suggest that Teak,

Pyinkado, and Gurjan logs will be included in the tender.

In addition, to reduce pressure on natural forests,

80,000

acres (32,375 ha) of teak plantations have been established

within the country the journal mentioned.

Myanmar Teak Log Auction Prices (natural forest

logs)

Purchases were made by competitive bidding in

September 2011.

¡®Save the Ayeyarwady¡¯ campaign a challenging task

for MOECAF

The controversial Myitsone Hydroelectric Power Project

in Northern Myanmar, was in the news again recently. A

host of people from all walks of life doubt the merit of

building this dam saying the cost to the environment will

be too high and they have started a ¡®Save the Ayeyarwady¡¯

campaign.

The media in Myanmar has suggested that the

government

is re-examining this plan and that the Ministry of

Environment Conservation and Forestry will review the

environmental impact assessment.

Analysts in Myanmar say that considering the new

government¡¯s commitment to preserving the environment,

these current events may help strengthen MOECAF¡¯s role

in re-aligning the country¡¯s forest and timber trade

policies.

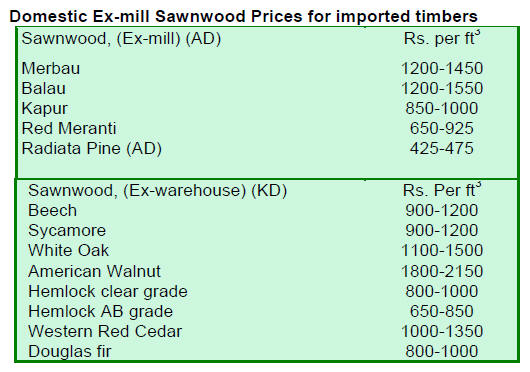

6. INDIA

Gandhidham emerges as a wood

manufacturing hub

Gandhidham is a city and a municipality in the Kutch

District of Gujarat State and home to India's largest port

Kandla which is around 11 km from the city. Kutch is a

growing economic and industrial hub in one of India's

fastest growing states. Its growth as a major industrial

centre on the western side of India has helped the

development of two major ports, Kandla and Mundra.

When Kutch was declared a wood industry hub it

opened

an opportunity for entrepreneurs to expand wood based

industries drawing on imported raw materials.

Today the region has one of the fastest growing wood

based industries. There are around 500 sawmills, some 70

plywood and veneer mills, 2 fibreboard plants and one

paper laminate plant in the area.

Timber imports into the area in fiscal 2010-11

reached 3.7

million cubic metres, of which just 1.23 million cubic

metres was of coniferous species. Analysts point out that

almost half the timber imports by Indian companies pass

through these facilities.

Growth of particleboard industry limited by raw

material supply

The growth in demand for particleboard in the country has

been around 30% annually in recent years making it one of

the fastest growing panel products in the market.

The commissioning of 5 to 6 new plants every year is

keeping up this momentum. Analysts say that the only

thing holding back further expansion of the particleboard

industry is the lack of raw materials.

The shortfall in domestic supplies is being made up

by

imports but local efforts to raise plantations of eucalyptus

and poplar are being made by various State Forest

Departments and by private investors. However, the

demand for raw materials is outstripping the supply.

Further interest rate increases anticipated

The Bank of India has indicated that it will continue its

aggressive monetary policy in support of the government¡¯s

continued push for growth. The Bank has been trying to

address high inflation for the past 2 years by reining in

demand through interest rate increases but many say this

has had the effect of seriously slowing economic growth.

The Bank has indicated that it will only consider

lowering

interest rates when the economy is showing signs of

cooling. On September 17, the Bank announced its twelfth

interest rate increase in eighteen months and it is expected

to raise rates again in October.

Raising plantations of endangered species

While industrial plantations are the priority for industry

analysts are calling for more attention to be given to

raising plantations of Sandalwood and Red Sanders as the

demand for these two timbers is unabated.

Newspaper reports indicate that illegal trade in

these two

precious woods continues. If new plantations are not

established, a day will come when they may become

extinct says an analyst.

7. BRAZIL

August data shows broad based

decline in exports

In August 2011, the total value of wood product exports

(except pulp and paper) fell 2.7% compared to values in

August 2010, from US$217.4 million to US$211.5

million.

Pine sawnwood exports increased 0.7% in value in

August

2011 compared to the same month in 2010, from US$14.3

million to US$14.4 million. In terms of volume, exports

increased 6.1%, from 61,800 cu.m to 65,600 cu.m year on

year.

Exports of tropical sawnwood fell both in volume

and in

value, from 42,300 cu.m in August 2010 to 35,600 cu.m in

August 2011 and from US$19.9 million to US$18.7

million, respectively, over the same period.

This performance represents an overall 6.0% decline

in

value and 16% decline in export volumes.

Pine plywood exports dropped 23% in value in August

2011 compared to levels in August 2010, from US$32.2

million to US$24.7 million. The decline in volume

amounted to 29% over the same period, from 87,800 cu.m

to 62,600 cu.m.

Exports of tropical plywood also dropped going from

9,800 cu.m in August 2010 to 7,300 cu.m in August 2011,

representing a 25.5% decline. In terms of value, a 17% fall

was recorded, from US$5.4 million to US$4.5 million.

Exports of wooden furniture also suffered as the

value of

exports fell from US$48.1 million in August 2010 to

US$45 million in August 2011, a 6.4% decrease.

Hardwood product exports boosted by strong

performance of mills in northern Mato Grosso

Exports of wood products from mills in Alta Floresta

earned some US$22.4 million between January and

August this year according to the Ministry of

Development, Industry and Foreign Trade (MDIC). This

represents a staggering doubling of trade over the same

period last year, when exports totaled US$11.3 million.

Exports of non-coniferous wood products lead the

way at

US$11.2 million (50.3%). The United States was the main

importers of wood products from Alta Floresta, accounting

for around 37% of the year¡¯s total exports. Hong Kong

followed with 21% of the total exports. Other export

destinations included Egypt (12%), Iraq (6%) and Spain

(4%) as well as about 19 other destinations.

Plans to raise competitiveness of furniture

manufacturers in Santa Catarina

In September this year an agreement to improve the

manufacturing and trade in wooden furniture was signed

by the Wood and Furniture Producers Association of

Western Santa Catarina (Amoesc) and the Furniture and

Woodworking Industry Union of Uruguay Valley

(Simovale), and the Industry Federation of State of Santa

Catarina (Fiesc).

The purpose of this agreement is to raise the

competitiveness of participating companies, provide

support and encouragement to furniture exporters in

Western Santa Catarina and expand international

marketing activities.

A preliminary assessment made of the furniture

companies

in the Western Wood Products cluster reveals that most

are not oriented towards export markets and have little

experience in managing export marketing.

The agreement is part of an ¡®Exporting Industrial

Extension¡¯ (PEIEX) project created by the Ministry of

Development, Industry and Foreign Trade and Apex

Brazil.

The agreement will expand industry access to

support

services available from government institutions and the

private sector, provide means for technical and

management improvements and technological change.

Approximately 140 major companies of Western of Santa

Catarina are involved.

Timber prices in domestic market continue upward

trend

Prices of wood products in the domestic market in BRL

increased on average by almost 2% over the past month

but when compared in terms of US dollars the increase

was much larger being on average 3.5%.

Demand for sustainable timber could outstrip

supply

in Para says IMAZON

In a study prepared by IMAZON, (Amazon Institute of

People and the Environment), a non-profit research

institution, an assessment of the availability of forest areas

for forest management was made considering current and

future demand for timber by the wood processing industry

in Para State.

Production and consumption of wood products in Para

State is the highest in Brazil and the state currently

produces around 6.5 mil. cu.m of wood products from the

natural forest.

To ensure sustainable production it has been

estimated

that, at the current rate of harvesting, the timber sector in

Para needs approximately 100 square km of forests

assuming a cutting cycle of 30 years.

The IMAZON study suggests that the forest area

available

is insufficient to support sustainable harvesting to meet

projected increase in demand for raw material and that

some 210,000 sq. km will be required.

The report recommends policies for more effective

and

transparent preparation, approval and implementation of

forest management plans in the State with emphasis on

sustainable forest concession management planning.

Amazonas considers law on payments for

environmental services

The Northern Amazonian state of Amazonas could be the

third state in Brazil to enact laws defining payments for

environmental services aimed at encouraging the

protection of natural resources. Currently, only Acre and

Esp¨ªrito Santo have approved state laws and have actually

implemented payments for environmental services.

A commission formed by representatives from the

Forum

on Climate Change and other institutions have prepared a

draft law which is currently under discussion in

Amazonas. This is a significant issue in the State and the

broad based discussions planned will involve civil society

and the mainly forest and rural communities across the

state.

Despite ¡®hot¡¯ economy interest rates cut by half

a percent

The National Consumer Price Index (IPCA) was 0.37% in

August, after rising by 0.16% in July, according to the

Brazilian Institute of Geography and Statistics (IBGE).

The cumulative rate over the last 12 months up to August

2011 is 7.23%, the highest since June 2005 and well above

the 6.5% target set by the government.

The average exchange rate in August was BRL

1.60/US$

compared to BRL 1.76 in the same month of last year. The

appreciation of the Brazilian currency against the US

dollar continues to be of concern to exporters.

The Monetary Policy Committee (Copom) reduced the

prime interest rate (Selic) from 12.50% to 12.00% at its

meeting in the end of August. The next Copom meeting is

scheduled for mid-October.

8. PERU

Growth forecasts revised

downward

Peru¡¯s Central Bank has lowered its forecast for the

country¡¯s economic growth for this year and in 2012

because of uncertainty in the economies of the United

States and Europe.

Peru¡¯s GDP is forecast to grow by 6.3% this year,

down

from a previously expected 6.5%. The Central Bank has

indicated that they expect the economy to slow in the

second half of the year to 5% and that in 2012 a growth of

only between 5-6% will be achieved.

Amazonian Ucayali Wood Technology Fair

Promotion of the Amazonian Ucayali Wood Technology ¨C

FAMATEC fair has started.

The objective of the fair, say organizers, is to

reduce the

negative impacts of the current economic crisis on the

forestry sector by developing the flow of wood products

and by diversifying markets.

According to organizers, this event is aimed at

forest

concession holders, exporters, traders, manufacturers and

all private, state and nongovernmental bodies in the

forestry and timber sectors.

Ministry of Development and Social Inclusion

established

Peru¡¯s Congress has approved the creation of a new

Ministry of Development and Social Inclusion.

This ministry will be responsible for implementing

the

government¡¯s main social programmes to improve social

inclusion for marginalized sectors of Peru that are yet to

feel the benefits of the country¡¯s economic growth.

9.

GUYANA

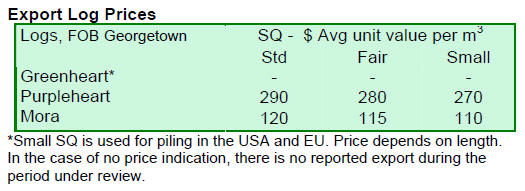

Activity in the market

suggests a slowing of demand

During the period under review there was a reduction in

Greenheart log exports compared to levels recorded

recently. Only standard and fair sawmill quality logs were

exported.

At the same time Pupleheart log export prices

dipped for

standard and small sawmill qualities, whilst Purpleheart

fair sawmill quality log price held onto gains made

recently. In contrast, export shipments of Mora logs were

up and prices were favourable for all sawmill qualities.

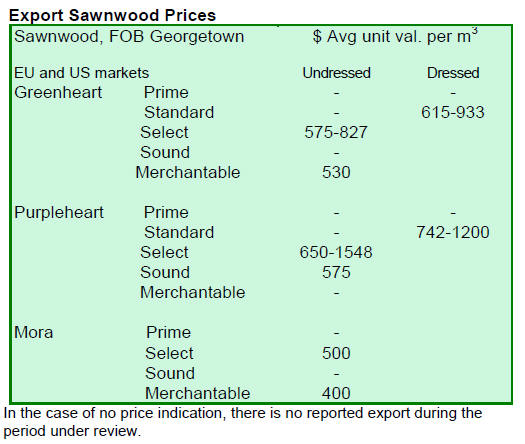

Lack of direction in market for Guyana¡¯s

sawnwood

The trade in sawnwood for this fortnight showed no

particular direction. Undressed Greenheart (Select) prices

dropped at the top end of the range from US$827 to

US$615 per cubic metre. Undressed Purpleheart

sawnwood prices also declined at the top of its range from

US$1,548 to US$1,050 per cubic metre. Undressed Mora

prices remained unchanged.

Dressed Greenheart prices remained firm compared to

levels in the recent past while dressed Purpleheart prices

slid from US$1,200 to US$1,060 per cubic metre.

Plywood exports to neighbouring countries resume

Plywood exports to markets in the Caribbean and in

neighbouring countries resumed in September and prices

were reported as favourable moving to US$588 per cubic

metre.

The contribution of value added product exports for

this

period were encouraging making a noteworthy

contribution towards the total export earnings. The

Caribbean was the main destination for exports from

Guyana.

Countrywide survey to assist sawmillers and

timber producers

Following recent meetings of stakeholders on the

unavailability of sawnwood in the local market and due to

the need to encourage more utilization of Lesser Used

Species of timber, the Forest Products Development and

Marketing Council of Guyana (FPDMC) is undertaking a

country wide survey aimed at assisting sawmillers and

timber producers in the forest industry.

The main objective of this survey is to determine

the

issues affecting stakeholders and what can be done to

increase performance in their business operations.

This survey will also help identify whether Guyana

is

actually widening its species utilisation and if sawmillers

are supplying what is demanded by consumers.

LUS promotion underway in Guyana

The FPDMC is currently engaged in creating awareness of

the lesser used species locally by way of promotional

activities which include newspapers and television

advertisements.

This promotion is aimed at increasing the awareness

of

contractors, architects and home-owners of the lesser used

species timber in Guyana and helping to alleviate the

pressure on the popular commercialised species such as

Greenheart and Purpleheart.

The FPDMC, Guyana Forestry Commission (GFC) and

the Forest Producers Association (FPA) are working with

the forest stakeholders to increase the awareness of the

lesser used species selection to lessen dependency on the

popular species of timber.

Related News: