|

Report

from

Europe

Mixed signals for tropical hardwood

Overall 2010 was a slightly better year for the European

trade in tropical hardwood than 2009, although purchasing

remained at levels well below those before the recession

and there were unsettling signs of declining market share

in some sectors.

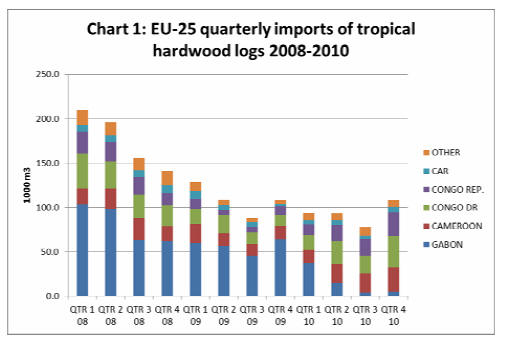

The latest EU-wide trade data indicates that imports of

tropical hardwood logs into the region reached 354,000

cu.m (down 18% on 2009) valued at €133 million (down

7%). The big decline in imports from Gabon following

that country��s log export ban imposed from May 2010

onwards was only partially offset by rising imports from

other countries in the Congo basin.

Nevertheless, quarterly data indicates that after reaching

an all time low in the third quarter of 2010, the pace of

imports of tropical hardwood logs picked up significantly

in the closing months of the year. EU-25 imports of

tropical hardwood logs during the October to December

period reached 108,000 cu.m, up from only 78,000 cu.m in

the previous quarter.

Interestingly, EU imports of tropical logs in the last

quarter of 2010 were almost exactly the same volume as

the same period in 2009, before introduction of Gabon��s

log export ban. Three countries are now filling the void

created by Gabon��s withdrawal as a supplier - Congo

Democratic Republic, Cameroon and the Congo Republic

- each now contributing between 25% and 30% of total

EU imports.

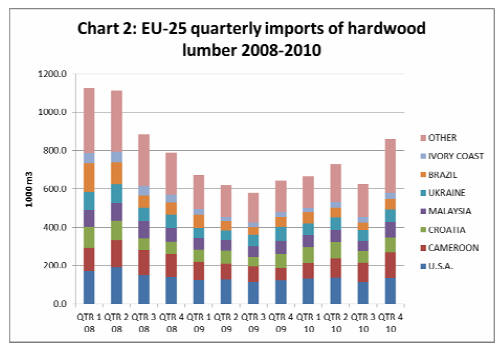

EU hardwood imports up 7percent

EU imports of hardwood lumber (tropical and temperate)

reached 2.69 million cu.m valued at €1435 million, up 7%

and 12.4% respectively. Despite the gains, imports were

still down 42% on levels prevailing before the recession.

This is due both to lower consumption and much reduced

supply as harvesting levels fell dramatically and large

swathes of the hardwood industry were effectively forced

to close during 2008 and 2009.

Lack of credit coupled with a desire to keep lower

inventories during times of uncertainty has also fed a

strong trend towards just-in-time ordering which has

tended to favour more readily available hardwoods.

Temperate hardwood lumber producers have benefited

most from this trend, and last year there was significant

growth in EU imports from several Eastern European

supply countries, notably Croatia, Bosnia, Serbia and

Romania.

Of leading tropical hardwood lumber suppliers to the EU,

imports from Malaysia and Brazil fell last year. In

contrast, there was a reasonable recovery in the level of

EU imports from Cameroon. Lumber exports from Gabon

also rose significantly last year, one effect of the log

export ban.

Signs of sustained market improvement in the last

quarter of 2010

The quarterly hardwood lumber import data provides

some cause for optimism that the recovery in Europe��s

sawn hardwood markets will be maintained. There was a

robust rebound in the level of EU hardwood lumber

imports in the last quarter of 2010. During that period, EU

hardwood lumber imports reached 861,000 cu.m, the

highest quarterly figure for over two years. This suggests

that the big decline in imports during the third quarter of

2010 was seasonal and due to short-term stocking issues

rather than a long-term reversal in underlying consumption

trends.

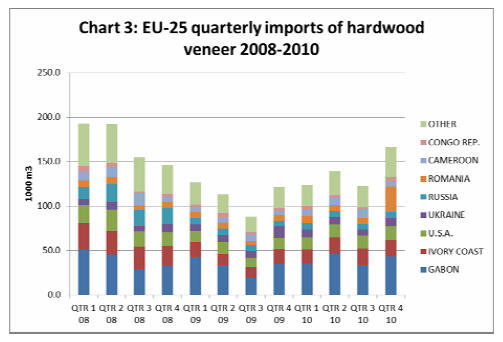

EU imports of hardwood veneer have followed a similar

pattern. Overall EU hardwood veneer imports reached

514,000 cu.m in 2010 valued at €455 million, up 14% and

13% respectively. This is partly the result of a switch to

hardwood rotary veneer imports by European plywood

manufacturers in place of logs from Gabon following the

log export ban in May. In addition to Gabonese exporters,

those in various other African countries are benefiting

from this trend including Cameroon, Ghana and Equatorial

Guinea. Rising levels of veneer imports from countries

better known for supply of sliced veneer �C such as Ivory

Coast, USA, and Romania - suggests this component of

the veneer market has also seen some recovery this year.

Strong recovery in veneer imports in October to

December period

As in the hardwood lumber trade, the quarterly data

indicates strong recovery in EU imports of hardwood

veneer in the last quarter of 2010 after a disappointing

performance in the June-September period. The sharp

downturn in EU veneer imports during the third quarter of

2010 seems to have been due to short term over-stocking

of okoume rotary veneer destined for the European

okoume plywood trade, a sector which in recent times has

been struggling to compete with cheap Chinese

substitutes.

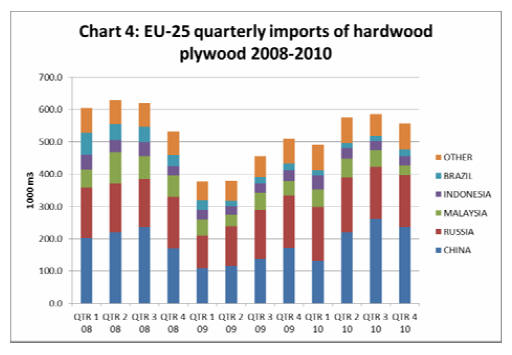

Imports of hardwood plywood into the EU-25 group of

countries during 2010 reached 2.21 million cu.m valued at

€798 million, up 28% and 40% respectively on the

previous year. The particularly sharp rise in the unit value

of imports must be welcome news for a sector that has had

to deal with narrow and ever declining margins over recent

years.

However the data doesn��t bode well for all hardwood

plywood producers. A notable trend in the EU market

during 2010 was growth in the share of China, Russia,

Ukraine, and Uruguay, largely at the expense of Malaysia,

Brazil and Gabon. Tropical hardwood plywood grades

continue to be substituted by cheaper more readily

available combi-products, plantation-grown eucalypt

products, and birch plywood.

The quarterly data is also disappointing, revealing a

significant downturn in EU hardwood plywood imports

during the October to December period last year. This is in

line with market reports indicating a downturn in

European demand for raw grades of tropical and Chinese

hardwood plywood at the end of last year. Following

significant imports of plywood in the second and third

quarters of 2010, many importers were carrying excess

stocks into 2011 relative to limited demand. Demand for

more specialist film-faced products was performing rather

better, continuing to benefit from higher prices and low

availability of birch plywood due to the forest fires in

Russia during 2010 and the Russian export tax on birch

logs.

Certification central to marketing tropical hardwood in Europe

The role of independent certification as an increasingly

essential requirement for marketing of tropical hardwood

in the European market was a central theme of

commentary in the annual Tropical Timber Supplement

published by the Timber Trades Journal (TTJ).

Requirements for certification in the tropical hardwood

sector are currently being driven by Corporate Social

Responsibility policies of larger retailers and

manufacturers and are expected to receive a major boost

with introduction of the ITL. Large housebuilders, retail,

public sector, and merchant customers all demand chain of

custody certification for most products, regardless of

whether they��re tropical or temperate forest-sourced.

Several commentators quoted in the TTJ emphasised the

power of forest certification to overcome existing

prejudices against tropical hardwood in the European

market. Representatives of several large and high profile

wood consuming companies all made the case for

continued use of certified tropical hardwoods as a way of

adding value to sustainably managed tropical forests,

providing incentives for good practice and reducing

pressure to convert forests.

Certification not an easy option

While it is increasingly obvious that certification is a large

part of the answer to tropical wood��s image problem in the

European market, the TTJ supplement also highlights that

this is not an easy option. While an investment in

certification may run into millions of dollars, many

commentators note the continuing lack of willingness to

pay on the part of final consumers. Certification is

required simply to protect existing market share for

tropical hardwood and can��t be expected, in isolation, to

generate a big increase in market demand. In these

circumstances, it seems likely that the largest operators in

the tropical timber sector will be the major beneficiaries

from the shift to certification.

Nevertheless, while there a few positive examples of

progress towards certification in the tropics, many

commentators in the TTJ supplement were seriously

concerned that the pace of uptake is likely to fall behind

the level of demand in the future. There is a widespread

expectation in Europe that demand for certified tropical

wood will pick up strongly over the next two years as the

EU moves towards full implementation of the ITL. This is

raising concerns that the ITL may have negative

consequences in a world where the balance of wood

consumption is shifting inexorably away from western to

emerging markets.

Commentators in the TTJ supplement gave some

consideration to measures that might help overcome these

obstacles. Representatives of European manufacturers and

retailers note their continuing willingness to pay premium

prices for certified tropical wood even when their own

customers are unwilling to pay extra. Others note the

importance of leaving the door open to a range of

certification systems, not just demanding FSC as a default

position, to help keep options open and costs down.

Need to increase EU demand for lesse rused species

The TTJ supplement highlights that there is also a

continuing concern in some quarters to increase the range

of tropical timbers used in the European market so as to

boost availability and the income that may be derived from

certification of tropical forests. The MD of Ecochoice

notes that they recently conducted a study with TRADA

for the UK Environment Agency looking at the

appropriateness of different tropical species for sea

defence works. It��s noted ��we had some very positive

findings with angelimvermelho, cupiuba, eveuss, okan and

tali��the challenge is now fostering demand for these

tested, yet relatively new species. It seems to be all in the

name. Even though we demonstrated that these species do

a great job, customers still want ekki or greenheart. We

need to educate clients to think performance, not species.��

Market impact of modified wood products

There were mixed views expressed in the TTJ supplement

on the question of whether ��modified�� softwoods and

temperate hardwoods are having a significant impact on

European markets for tropical timbers. A representative of

UK-based importer UCM suggests the impact is ��small��

and that it remains unclear how long-lasting it will be. It��s

noted that ��tropical timbers are known for durability,

appearance and strength and some modified timbers don��t

replicate all those properties��.

In contrast representatives of Lathams and Ecochoiceare

very upbeat about prospects for modified woods,

suggesting that existing technical limitations are being

gradually overcome through further research and testing.

However, in both cases, the suggestion is that modified

wood products are more likely to ��supplement�� than

replace tropical hardwoods.

Related News:

��

|