2.

GHANA

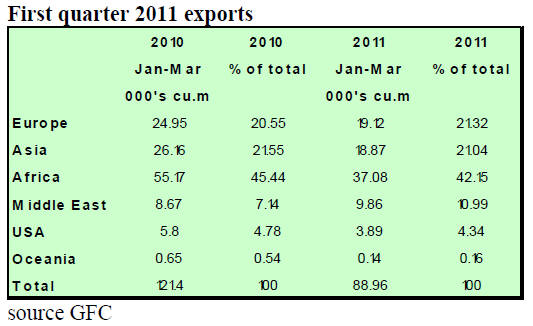

Exports to the EU half of those to African countries

Exports of primary products (poles and billet) were worth

Euro 30,175,011 in the period January-March 2011 as

compared to Euro 39,525,381 in January-March 2010

while trade in tertiary products totalled Euro 2,508,036

compared to Euro 2,995,959 in January-March 2010.

Secondary products contributed 88% or Euro 26,748,889

to earnings for the first quarter as compared to 85% in the

first quarter 2010.

Markets in Africa accounted for around 43% of the total

trade and in the first quarter and were worth Euro

13,024,276. The main African importers were the

ECOWAS countries, especially Nigeria, Senegal, Niger,

Gambia, Mali, Benin, Burkina Faso and Togo.

Exports to the EU are now around half the level of those to

African countries and for the first quarter 2011 were Euro

7,562,190. Key EU markets included Italy, France,

Germany, the United Kingdom, Belgium, Spain, Ireland

and Holland.

Markets in Asia such as India, Malaysia, Taiwan P.o.C,

China, Singapore and Thailand together contributed Euro

3,924,077 to total export earnings in the first quarter 2011.

The US market now accounts around 10 of Ghana¡¯s export

earnings and in the first quarter earnings were down on

those fro the first quarter 2010.

3.

MALAYSIA

Industry cautioned against expectations of

Japanese market demand

Analysts believe that Malaysian log and plywood prices

are set to rise substantially in response to demand for

reconstruction projects after the tragic earthquake and

subsequent tsunami in Japan.

In some cases just after the earthquake, plywood prices in

Japan rose between 30% to 50% especially among

plywood stockists and traders. Price increases among

plywood millers were more conservative.

However, some quarters have cautioned the timber

industry in Malaysia against speculating on the immediate

potential demand for logs and plywood from Japan.

Escalating fuel costs in Malaysia have made Malaysian

timber and timber products become the most expensive in

SE Asia.

Japanese government officials are still working on drafting

the first comprehensive blue-print for the reconstruction of

infrastructures and housing in Japan. It is likely that the

blue-print may only be released as late as October this

year. It is anticipated that Japan may source much of its

plywood needs from China and Indonesia.

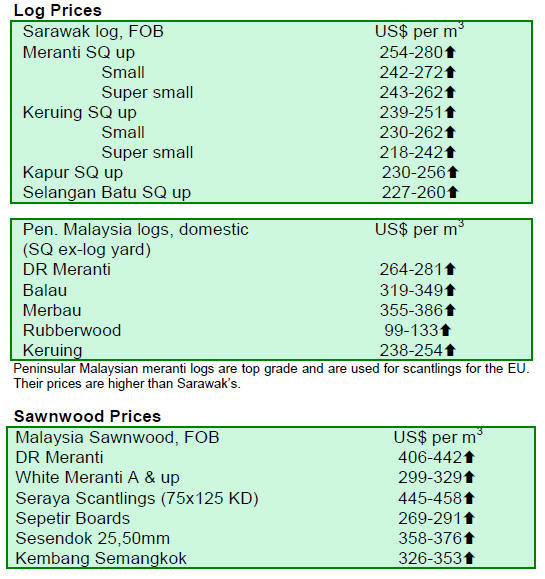

Log availability affected by filling of Bakun dam

Log prices in Sarawak continue to rise as availability has

been affected by the ongoing flooding of the Bakun

hydroelectric dam.

Log production in Sarawak has fallen 23%, from 2.35

million cu.m in the first quarter 2010. Log export prices

are up by around 15% year on year.

In addition, exports of logs from Sarawak have also fallen

27%, from 1.07 million cu.m in the first quarter 2010 to

783,800 cu.m this year.

Sarawak shipped more than 51,800 cu.m of logs, valued at

RM28.7 million to Japan in the first quarter 2011, a drop

from the 81,400 cu.m shipped in the same period last

year. However, India remains Sarawak¡¯s largest log

importer, taking some 506,000 cu.m in the first quarter of

this year. This constitutes almost 65% of Sarawak¡¯s total

log exports.

Malaysia set to launch another international furniture show

Malaysia is set to launch another international furniture

show in September this year to draw visitors who may be

visiting other furniture shows around the Asian region

during that time, such as the ones in Shanghai and

Guangzhou.

The International Furniture Market exhibition is scheduled

to be held from September 6 to September 10, 2011, at the

Malaysian Agro Exposition Park.

4.

INDONESIA

Indonesia to aid Japan at its time of need

Japan has sought help from Indonesia and other plywood

producing countries to meet its requirements for some 2

million sheets of plywood for reconstruction work in the

disaster hit areas.

It is reported that the Indonesian government is to

work

out a plan for shipping plywood at concessionary rates to

Japan. Japan is also seeking logs, sawnwood, laminated

timber products and other panel-products.

Indonesia is currently the second largest exporter of

timber

products to Japan after Malaysia. The other major exporter

is China. Indonesia¡¯s plywood exports to Japan in 2010

reached almost 932,000 cu.m.

The Indonesian government has a close relationship with

the Japanese government and is expected to assist the

country in its time of need. The Indonesian government

will reportedly meet to discuss the Japanese requirements

and is thought to be considering waiving any plywood

export taxes and tariffs.

5.

MYANMAR

Market demand for teak and other hardwoods has

picked

up and overall the market is said to be good for round logs.

Logs versus processed wood exports discussed

A seminar on ¡°Emerging Market Requirements-

Challenges and Opportunities for Myanmar¡¯s Timber

Industry¡± was held recently in Myanmar, the key speaker

was Dato Dr. B.C.Y. Freezailah who spoke on the world

timber situation, illegal logging and emerging market

requirements.

He also spoke on legality and sustainability of timber,

EU

regulation, the US Lacey Act, and Pan ASEAN timber

certification initiative and various topics of interest to the

Myanmar wood industry.

U Barber Cho, Joint Secretary of the Myanmar Timber

Merchants Association also presented a paper on the

development of the Myanmar wood industry. He reported

on the state of the Myanmar timber industry, where he

discussed the availability of raw material and the pros and

cons of selling less in log form and more processed wood

products.

He made the point that neighbouring countries with

fewer

timber resources, such Malaysia and Vietnam, are earning

more revenue from wood products than Myanmar. He said

that Myanmar is rich in forest resources and stressed the

need for the country to learn from its neighbours.

6. INDIA

Foreign investment directed to the

furniture sector

Foreign investment in the timber and furniture sectors has

been encouraged by the Indian government to meet the

growing demand for furniture and other timber products.

Initiatives have been taken to increase investment flows

into timber manufacturing.

The furniture sector in India makes a marginal

contribution to GDP, representing just a small percentage

(about 0.5%). In terms of size and technological

innovation, the office furniture segment has the more

important companies. The government of India has

specifically directed foreign investment in the timber

sector towards meeting the huge demand for office

furniture in the country.

Timber product manufacturing is one of the oldest

industries in India. Although traditionally a rural industry,

in recent years, the manufacturing of timber products has

developed to an industrial scale. The furniture industry in

India is considered as a "non organized" sector, with

handicraft production accounting for about 85% of the

furniture production in India.

Ambitious investment programme for Kolkata Port

The Kolkata Port, located on the banks of Hoogly river is

unique because most other ports in India are sea ports. The

Kolkata Port Trust manages two ports, Haldia's deep water

port and the oil piers of Baj Baj. Kolkata Port Trust,

formerly the Calcutta Port Trust oversees the shipping

system in Kolkata.

The Port Trust has embarked on an ambitious

investment

programme for development and expansion of the port in

order to handle increased trade. The plan is construct

multipurpose berths and jetties and improve support

facilities as well as the development of infrastructure to

augment existing road and rail connections. For more

information see

http://www.kolkataporttrust.gov.in/

Timber importers have drawn attention to the port

charges

at Kolkata port which they say are high compared to other

ports.

They point out that Kolkata Port is geographically

best

placed to handle timber imports from SE Asian countries

but that port charges discourage them from using this port.

In recent years Kolkata port handled only an amount

equal

to 20% of the timber imports through Kandla port.

7. BRAZIL

First production of

sustainable timber

The first harvest of some 7,000 cu.m. of certified

sustainably produced wood has been made from a

concession in the Jamari National Forest, state of

Rondonia. This has generated close to BRL 700.000 (US$

422,120) according to the Brazilian Forest Service (SFB).

The SFB says this is the beginning of a process to

ensure

wood for the final consumer is from a forest managed in a

manner to guarantee land tenure security, legal security

and compliance with SFB environmental criteria.

The harvested timbers include about 30 species of

which

Astronium lecointei (trade name tiger wood) accounted for

28% of the harvest.

This timber is largely used in furniture

manufacturing and

flooring. Other timbers included tauari (Brazilian oak) and

angelim-pedra used in furniture manufacturing and for

construction.

The forest concession totals 96,000 hectares and is

managed by three companies, Amata, Sakura and

Madeflona. The concessionaires have been encouraged to

explore a range of different species so as to benefit from a

reduction in taxes paid to the government. The tax relief

only applies if a minimum volume ofspecific species are

harvested.

The Forest Service is making efforts to promote the

introduction of less familiar timber species in the market.

Timber sector expands formal employment levels

The timber industry in Par¨¢ State is a major sector and has

been generating both permanent and part-time

employment opportunities mainly, say analysts, due to an

increase in the number of companies that have adopted

sustainable forest management operations.

Employment growth in the timber industry has, for

some

years now, been below government expectations even

though the sector has expanded output. In 2010, formal

employment in Para¡¯s timber industry grew significantly

according to the Inter-Union Department of Statistics and

Socio-Economic Studies.

During the year the sawmilling sector generated 444

permanent jobs while the veneer manufacturing sector

created some 144 fulltime jobs. Other industries, such as

joinery/carpentry manufacturers, wooden artifact

manufacturers and cork and straw artifacts producers

generated another 80 jobs.

Par¨¢ only state to expand exports in 2010

Par¨¢ state, in the Amazon, is the main producer of tropical

timber in Brazil. Timber exports from the state grew in

2010 in sharp contrast to the export levels from other

states in the Amazon.

According to the Association of Timber Exporters of

Par¨¢

State (AIMEX), there was a rise of almost 12% in the

export of industrial timber products in 2010 compared to

2009. This was due, says AIMEX, to the economic turnaround

in the United States and European Union.

However, AIMEX warns that the prospects for 2011

are

not as positive since the growth rates seen in 2010 were

not maintained in the first 4 months of this year. From

January to April 2011, there was a 15% decline in the

value of exports and 19% drop in export volumes.

SINDUSMAD seeks waterway to facilitate exports

The Timber Industry Union of Northern Mato Grosso

(SINDUSMAD) is lobbying hard to have the hydroelectric

power plant planned for the Teles Pires river build locks to

allow timber to be transported by river. The timber

industry as a whole supports the establishment of a

waterway linking the northern region to the Port in Par¨¢.

The strength of the Northern Mato Grosso regional

economy is forest and timber based and in 2010 over 5

million cu.m of logs from sustainable forest management

operations were traded.

The timber industry in the region accounts for 38%

of the

Transport and Housing Fund (FETHAB) revenues in the

state. At the national level, state output corresponds to 4%

of GDP.

8. PERU

Timber exports fall 11% in first

quarter

Due to subdued demand for timber from Peru in

international markets and the lack of effective policies on

forest concessions, Peruvian wood product exports fell

11% in the first quarter of 2011 says the Association of

Exporters (Adex).

According to preliminary figures from Adex, timber

sales

were valued at US$31.7 million in the first quarter of 2011

compared to US$35.4 million the same period last year.

But, the situation is even worse when 2011 first quarter

exports are compared with those in the same period in

2008 (US$54.9 million). The main products affected were

semi-manufactured goods, lumber and minor product

exports.

Exports of semi-manufactured products were valued

at

US$12.8 million compared to the US$16.8 million level

for the first quarter in 2010. Lumber exports fell from

11.1 million in 2010 to 8.7 million between January and

March 2011.

On the other hand, fibreboard and particleboard

exports

grew significantly from the US$355,000 in the first quarter

2010 to US$1 million in the same period this year.

Adex, reports that the export figures reflect the

status of

some markets for Peruvian timbers such as China which,

up until March, had not resumed purchasing after the

Chinese New Year holiday. Despite having reduced its

purchases by 41 percent, China remains the largest

importer of Peruvian wood followed by Mexico and the

US.

Legal framework required for industry revival

Adex has pointed out that since last year some production

capacity had been lost due to, what the industry considers

as, constraints imposed on concession holders and

producers by regional governments.

This, says Adex, is mainly because the authorities

have not

approved submitted management plans.

Adex also identified the lack of a supportive

infrastructure

in regional administrations to the point that entrepreneurs

decide to no longer pursue timber related businesses. Adex

indicated that for the industry to operate effectively an

adequate legal framework is required and urged that the

Congress approve the Forestry Law.

The United States is reportedly anxious to see the

Congress of Peru adopt the new forest law as soon as

possible so that the free trade agreement between the two

countries can come into force. It has been reported that the

Congress will continue debate of the forest law during the

first week of June.

Gold rush damages Peruvian Amazon

Deforestation in the Peruvian Amazon has increased in

recent years due to incursions by informal miners driven

by high gold prices.

This information came from a study released in May

by

Duke University. The study reports that in the eastern

department of Madre de Dios, some 7,000 hectares of

virgin forest and wetlands have been destroyed by mining.

The research combines NASA satellite imagery of

Madre

de Dios between 2003 and 2009, economic analysis of the

gold price and imports of mercury which is used in

separating gold. The head of the research team apparently

reported that mining areas in Peru are now clearly visible

from space. For more information see

http://today.duke.edu/2011/04/goldperu

9.

GUYANA

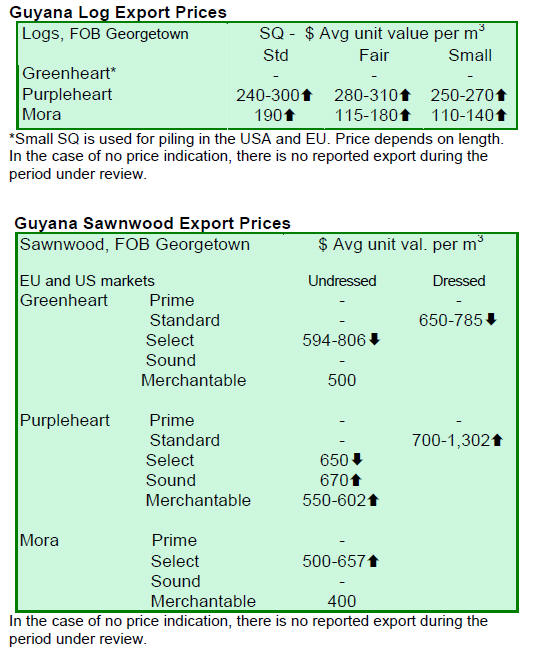

General upswing in prices

During the period under review there were no exports of

greenheart logs. Purpleheart logs continued to attract

increased prices for all sawmill log grades. Mora log

prices increased for standard and fair sawmill quality,

while prices for small sawmill quality remained

unchanged.

Undressed greenheart (select) prices have decline,

notably

at the top of the range and are now at US$806 in

comparison to prices two weeks earlier. For undressed

purpleheart there were some exports and accompanying

price changes for three of the sawmill qualities namely

select, sound and merchantable, these qualities fetched

higher prices. Undressed mora (select) also attracted

moderately higher prices.

Top end prices for dressed greenheart prices fell

from

US$1,011 to US$785 for this fortnight period as compared

to the previous period. However dressed purpleheart

continues to attract good export prices, with a strong

upswing in prices at the top of the range from US$1,060 to

US$1,302.

Some of Guyana¡¯s lesser used species have made

headway

in the Caribbean, European and USA sawnwood markets

and secured better prices than seen recently.

Prices for Guyana¡¯s ipe (washiba) rose reaching

US$2,350

per cubic metre. Demand for ipe is high in the North

American market. For roundwood, (greenheart Piles) were

well received in the European and North American market

attracting good prices along with (wallaba poles) for

which prices also improved.

The leading added value product exported recently

was

outdoor garden furniture for the UK market. Prices

increased for sustainably sourced outdoor furniture

utilizing Guyana¡¯s locust (jotaba). Other value added

product exports included doors and window frames.

Guyana launches UN ¡®Year of Forests¡¯

Guyana recently held a commemorative launch for the

United Nations¡¯ International Year of Forests.

In keeping with the long term goals of the Low

Carbon

Development Strategy, the Government of Guyana,

through its entities the Ministry of Agriculture and the

Guyana Forestry Commission, recognizes the importance

of reinforcing established policies on the use of forests

with particular reference to sustainable forest management

and its contribution to economic development and poverty

eradication.

Related News:

¡¡