2.

GHANA

Timber exports improved in January

According to the Timber Industry Development Division

(TIDD) of the Forestry Commission, wood and timber

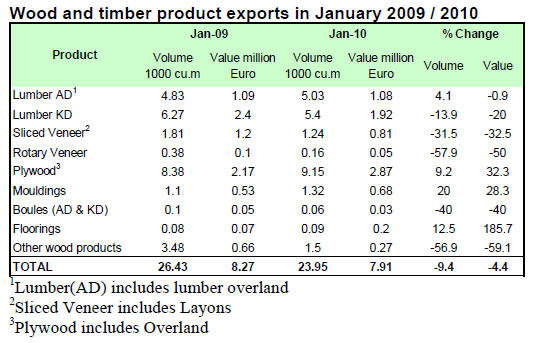

product exports from Ghana in January 2011 totalled

23,948 cu.m valued at Euro 7.9 million, compared to

26,430 cu.m and Euro 8.27 million in January 2010. This

represents a decline of 9.4% and 4.4% in volume and

value respectively.

In January 2011, exports of all timber products declined

except for plywood, moulding and parquet/flooring.

Exports of primary products, including poles and billets,

were valued at Euro 3 million in January compared to

Euro 3.6 million in January 2010. Similarly, the value of

exports of secondary timber products declined 3.5%, from

Euro 7 million in January 2010 to Euro 6.8 million

January 2011. However, exports of tertiary products were

valued at US$902,209 in Janaury 2010, up steeply by 32%

from US$681,275 in January 2010. Primary products,

secondary products and tertiary products accounted for

3%, 86% and 11% of the total export value respectively.

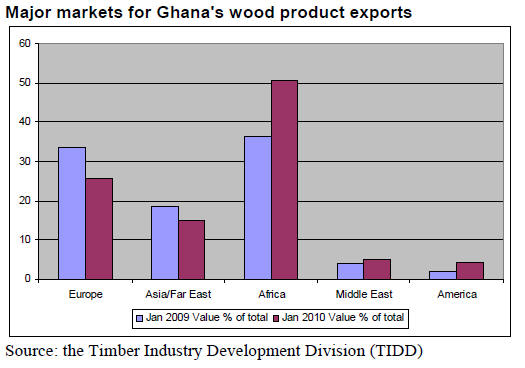

In January 2011, the share of Ghana¡¯s exports of wood and

timber products to other countries in Africa was 51% of

the total export value, compared to 36% in January 2010.

Exports to other destinations included Europe (26% of the

total export value), Asia/Far East (15%) and the Middle

East (5%). The main importing countries in Europe were

Italy, France, Germany, the UK, Belgium, Spain, Ireland

and the Netherlands.

Plywood accounted for 38% of the total exports of wood

and timber products exports from Ghana in January 2011.

Compared to January 2010, plywood exports rose 9.2% in

volume and 32% in value. The main importing countries

for Ghana plywood were Nigeria, Niger and Togo. Ceiba,

Mahogany and Ofram were the principal species utilised

for plywood production.

Reduced tariffs for electricity and water announced

Ghana's Public Utility Regulatory Commission (PURC)

announced reductions in utility tariffs for electricity and

water. The reductions range from 0 to 6.58% for

residential electricity consumers and from 0 to 13.38% for

non-residential consumers. Non-residential consumers will

also enjoy a 6.86% tariff reduction for water. These

revisions on tariffs were made on the back of lower

production costs resulting from the completion of the West

Africa Gas Pipeline.

Analysts were pessimistic over the impact of the revised

tariffs on total operating costs which are dependent on

several other factors.

Lending rate maintained to rein in inflation

The Monetary Policy Committee decided to keep its Prime

Rate at 13.5%, unchanged since July 2010 due to potential

risks in the fiscal outlook and inflation which climbed in

January 2011 for the first time in 19 months.

In addition, authorities will continue to intervene in order to

prevent the Cedi from a further freefall.

3.

MALAYSIA

Bulk of Malaysian furniture destined for exports

In terms of consumer spending on furniture, Europeans

and Americans spent an average of US$540 and US$300

per year respectively. However, Malaysians spent only an

average of US$40 per year. Although Malaysian furniture

is of international standards, most Malaysians prefer

imported furniture over domestic products.

Consequently, some 85% of furniture manufactured in

Malaysia are for exports. According to trade statistics, the

US remained the largest market accounting for RM1.98

billion of Malaysian furniture exports from January to

October 2010, followed by Japan (RM573 million),

Singapore (RM477 million) and the UK (RM407 million).

Other important export destinations include Australia,

Canada, Germany, India, the UAE and Saudi Arabia.

Asian is emerging as an important market for Malaysian

furniture exports on account of population reaching 1.3

billion in China, 1 billion in India and 550 million in the

ASEAN economic zone.

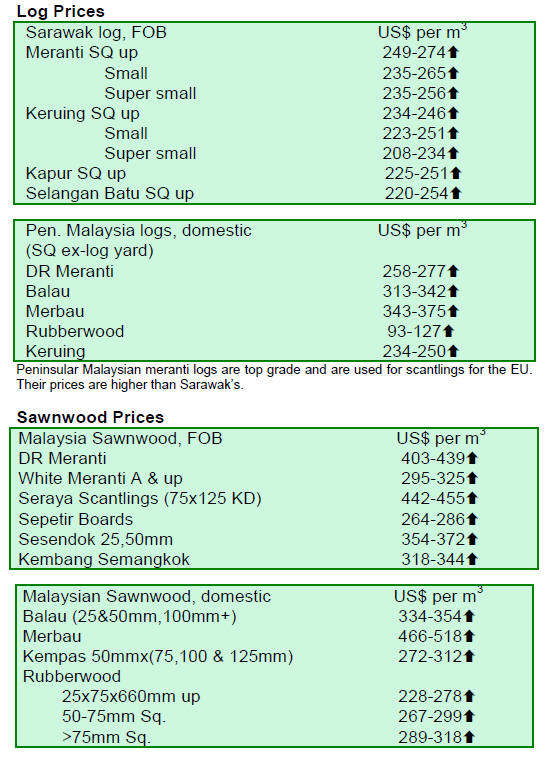

Tight supplies of rubberwood and palm fibres

Prices of Malaysian timber products continue to climb

across the board in line with other commodity prices.

Rubberwood prices remain buoyant as natural rubber

futures prices breached US$6.44 per kg in the Tokyo

commodity exchange TOCOM.

Similarly, with crude palm oil futures prices within the

range of RM3,600 per tonne, the supply of palm fibres, an

important component of most panel products, has become

tighter.

According to an analyst, supplies of rubberwood and palm

fibres will remain tight if high price levels of natural

rubber and palm oil are maintained in the international

markets.

4.

INDONESIA

Agreement on key points of moratorium reached

The Indonesian president is expected to sign a presidential

decree, laying the legal framework for the 2-year

moratorium on new permits to convert natural forests and

peatlands.

The Indonesian Presidential Delivery Unit working on

two

alternative drafts, has reached an agreement on the key

points of the moratorium. Secondary forests already

converted are excluded from the moratorium, but the

decree will incorporate mechanisms to protect pristine

forests and rehabilitate degraded forests.

Indonesia to sign VPA within 3 months

The Jakarta Post reports that Indonesia is hoping to sign

the Voluntary Partnership Agreement (VPA) under

FLEGT Action Plan with the EU within the next 3 months.

If this materialises, Indonesia would become the first

country in Asia to conclude such an agreement which

would require that only legally verified timber and timber

products from Indonesia be can supplied to the EU market.

The Jakarta Post quotes Iman Santoso, Director General

for Forest Business Management at the Ministry of

Forestry, Indonesia:

¡°We're nearly there. This agreement is crucial for

Indonesia as it enables Indonesian timber exporters to

expand their market for timber and timber products in the

EU¡.This is especially important because the EU has just

enacted a timber regulation prohibiting the sale of illegally

harvested timber in the EU market by March 2013¡±. The

value of Indonesia's timber trade with the EU stands at an

estimated US$1 billion per year.

Indonesia and Finland ink deal on renewable energy

sources

Indonesia and Finland signed a bilateral agreement to

promote wood-based biomass and agricultural residue as

renewable energy sources in the provinces of Central

Kalimantan and Riau.

The bilateral agreement will form the basis for the

Energy

and Environment Partnership (EEP) programme, designed

to reduce greenhouse gas emissions and combat climate

change.

The Finnish Ministry for Foreign Affairs had earmarked

Euro 4 millions for Indonesia to implement the

programme from 2011 to 2014. The programme will

enable Indonesia to access modern technologies in

renewable energy production.

Plywood in demand

Indonesian plywood manufacturers are hoping to benefit

from the current high prices of plywood. This will enable

them to upgrade machines and purchase spare parts.

Plywood manufacturers are also beginning to hire more

workers to cope with export demand.

Furniture manufacturers are also more optimistic as

more

orders are coming in from the Middle-East despite the ongoing

political unrest.

5.

MYANMAR

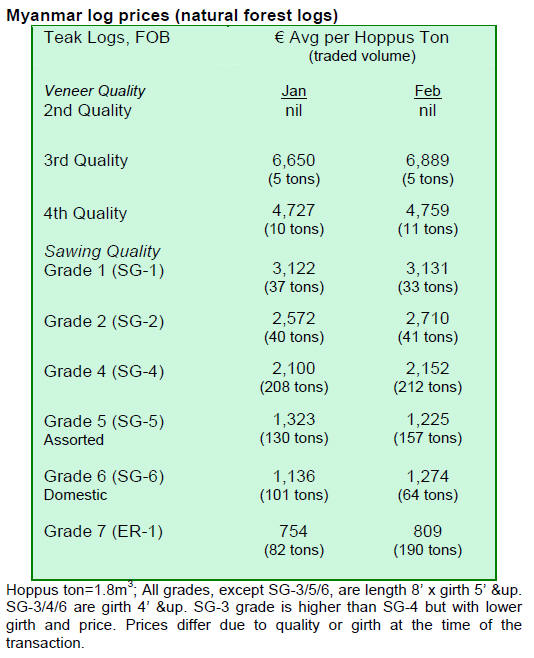

Market outlook remains favourable

The favourable market situation for teak and other

hardwoods remains unchanged from the previous month,

with marginal gains in prices. Market prospect for kanyin

logs has also improved particularly for veneer production.

At Myanmar Timber Enterprise (MTE) tender sales, the

higher grade teak SG5 logs fetched lower prices than the

lower grade teak SG6 logs. According to an analyst, this

was due mainly to forest area preference and grading.

All teak SG6 logs came from special and first class

areas,

while 42% of SG5 logs originated from second and third

class areas. An analyst says that besides the origin, prices

are determined by other factors including buyers¡¯

preference.

Other hardwood tender sales in February were done at

favourable prices indicating improving markets. Some 265

tonnes of export quality pyinkadoe logs fetched US$561 -

US$762 per Hoppus tonnes (MTE list price US$678). In

addition, some 500 tonnes of export quality kanyin logs

fetched US$424 - US$434 per Hoppus tonnes (MTE list

price US$390).

6. INDIA

India maintains robust growth in

trade

According to the Ministry of Commerce and Industry,

exports in January 2011 reached US$20.6 billion, 33%

higher than in January 2010.

Imports also rose to US$28.6 billion in January

2011, up

13% from the same month in 2010.

Declining exports to North America and Europe are

being

offset by increasing exports to Latin America, Africa and

Asia.

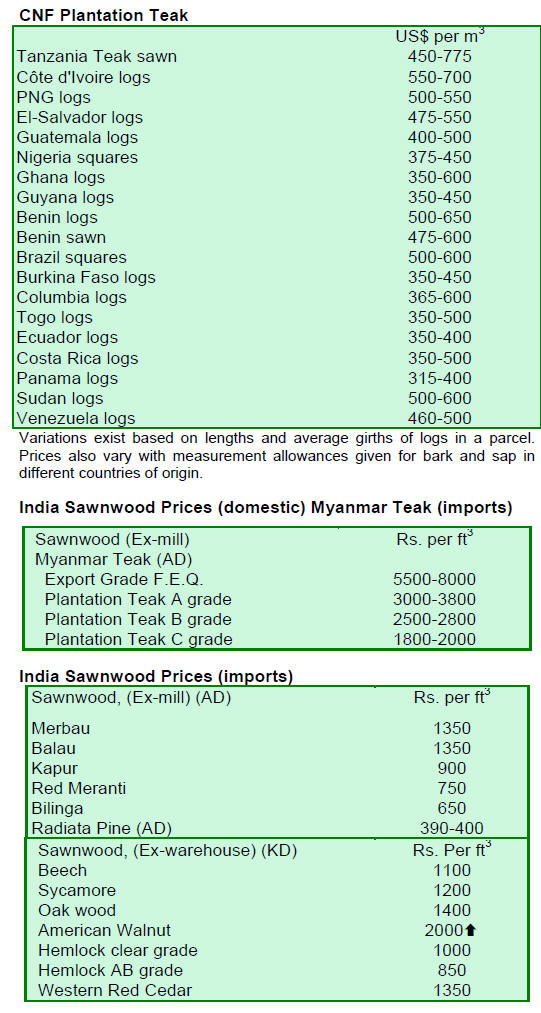

Plywood in good demand

According to an analyst, domestic demand for processed

timber products is on the rise.

Demand for plywood is good with imports from China

increasing. However, the quality of the plywood imported

has gone down.

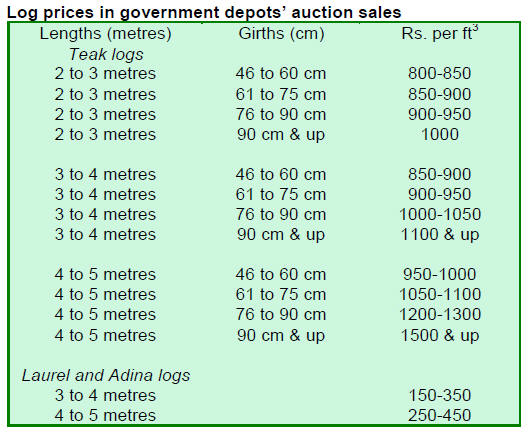

Teak prices trending upwards

Timber auction sales in government depots were brisk in

January with arrivals of fresh teak logs. As prices for

imported teak climb, auction sale prices are also up.

In addition to fresh logs, remaining logs from

earlier

auctions as well as logs harvested during previous season

were sold in February auction sales.

There have been less arrivals of teak in depots of

Maharashtra. Gujarat auctions sales ground to a halt as

bidders objected to the electric auction sales system

introduced by the local government to be launched in

March 2011. In contrast, sales in Madhya Pradesh were

more active. Teak supply remained good in Central Indian

depots with arrivals from Hoshangabad, Jabalpur, Harda

and Baitul.

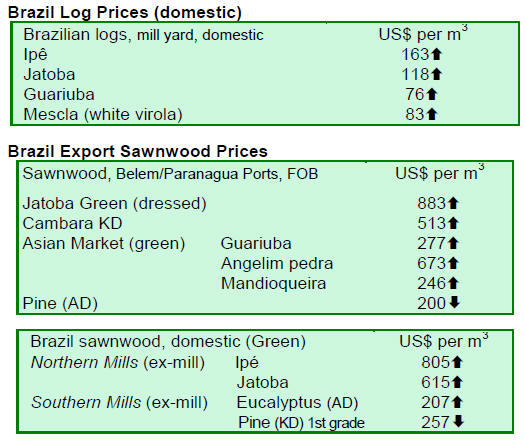

7. BRAZIL

Prices of timber products on an

upward trend

The average price of timber products in Brazil in BRL

increased by 1.24% from the previous fortnight. Prices in

US dollars also gained 2.73% due to the slight

appreciation of the Brazilian currency against the US

dollar.

Exports of tropical timber products continue to

decline

In January 2011, exports of timber products (excluding

pulp and paper) jumped 13.7% to US$170 million

compared to US$149 million in January 2010.

However, exports of tropical sawnwood declined in

terms

of both volume and value, from 39,000 cu.m worth US$20

million in January 2010 to 36,100 cu.m valued at US$17.8

million in January 2011, representing 7.4% decline in

volume and 11% in value.

Exports of tropical plywood also dipped, plummeting

19%

from 6,300 cu.m in January 2010 to 5,100 cu.m in January

2011. In value terms, the drop was 17%, from US$3.5

million to US$2.9 million.

For wooden furniture too, the value of exports

declined

10% compared to the level in January 2010 to US$30.8

million in January 2011.

In contrast, pine sawnwood exports jumped 38% in

January 2011 compared to January 2010, from US$8.1

million to US$11.3 million. In terms of volume, exports

rose 27% from 39,100 cu.m to 49,600 cu.m over the

period.

The value of pine plywood exports also surged 26%

in

January 2011 compared to the level in January 2010, from

US$21.6 million to US$27.3 million. In terms of volume,

exports rose 15% from 66,200 cu.m to 76,100 cu.m over

the period.

First hike in prime interest rate since July 2010

According to the Brazilian Institute of Geography and

Statistics (IBGE), the Consumer Price Index (IPCA) in

January 2011 increased 0.83% over the level recorded in

January last year, up 0.20 percentage points compared to

December 2010.

In January 2011, the average exchange rate to the

US

dollar was BRL1.67/US$ compared to BRL 1.78/US$

during the same month of 2010, showing further

strengthening of the Brazilian Real against the US dollar

over the period.

For the first time since July 2010, the Copom

(Economic

Policy Committee) raised the prime interest rate (Selic) by

0.5 percentage points to 11.25% per year in January 2011.

Economic assessment of forest concessions in

Par¨¢

The Brazilian Forest Service (SFB) and the Timber

Exporters Association of the State of Par¨¢ (AIMEX) will

organise a meeting on economic aspects of forest

concessions. The meeting is to assess prospects and

opportunities for trade and financing of forestry activities

in Par¨¢. The strategy for the forestry sector in Par¨¢ is to

increase its share in the domestic and foreign markets by

expanding forest concession areas under sustainable

management and attracting more financing.

SFB opened a bidding process for forest concessions

of

210,000 hectares in the Aman¨¢ National Forest. SFB plans

to launch three other bidding processes for forest

concessions covering 700,000 hectares in the context of

the management of national forests in the state of Par¨¢. In

addition, a forest concession of 48,800 hectares in the

Sarac¨¢-Taquera National Forest is expected to become

operational this year.

The national forests of Altamira, Aman¨¢ and Crepori

in

the regions of Itaituba and Jacareacanga of the state of

Par¨¢ cover altogether an area of over two million hectares.

It is estimated that 300,000 hectares of forests are required

under concession management per year in order to meet

the current demand for tropical timber in the state of Par¨¢.

Concessions are usually granted for period of 40 years to

facilitate effective combating of illegal forest activities and

promoting legal timber operations, commercialisation and

processing.

The volume of timber production in Par¨¢ was 6.6

million

cu.m in 2009, accounting for 47% of the total domestic

timber production. Par¨¢ was also the largest producer of

processed timber in Brazil at 2.5 million cu.m and

generated the highest gross revenue from logging with

BRL 2.17 billion in 2009, according to SFB.

Par¨¢ timber product exports on the mend

The value of manufactured and industrial timber product

exports from Par¨¢ in 2010 rose 11.7% to US$387 million

compared to 2009. In terms of volume, exports rose only

0.33% to 360,952 tonnes, still far below the record level of

exports of 1,016,678 tonnes worth US$793 million in

2007.

The total exports of Par¨¢ in 2010 were valued at

US$ 12.8

billion, up sharply by 54% over 2009. The timber sector

was the third largest exporter in the state.

The US continues to be the main export destination

for

timber products from Par¨¢ accounting for US$120 million

of the value of exports in 2010, up 9.7% compared to

2009.

In Brazil, the state of Parana is the largest wood

and

timber product exporter with a value of exports of US$647

million in 2010, followed by Santa Catarina (US$410

million) and Par¨¢.

Timber industry calls for cost sharing

The timber industry has called for sharing of maintenance

and infrastructure costs of public forests by the public and

private sectors.

According to the Timber Exporters Association of

the

State of Par¨¢ (AIMEX), forest concessions generate social

and environmental benefits for the states in the Amazon

and, as such the cost of a Forest Management Unit (FMU)

should be lower. Currently, the minimum price of a FMU

may be as high as BRL 2 million.

Restricting logging during the rainy season

The federal rule restricting logging, skidding and

transportation of timber in Mato Grosso was implemented

for the first time in 2010. For this year, the federal rule is

effective during the rainy season from 1 February to 1

April. However, forest engineers responsible for forest

management areas can extend the period in accordance

with the prevailing conditions in each area.

Log trade and transportation is only allowed from

timber

yards with forest roads built according to forest

management plans.

The aim of the rule is to address the problems of

soil

degradation and damage caused by logging undertaken

during the rainy season.

8. PERU

Congress debate on draft law deferred

As reported earlier, the Congressional debate on the draft

Forestry and Wildlife law was deferred to the next term

from March to June 2011. The consultations with

indigenous people were extended by 60 days to the end of

February. During that extended consultation period, the

minimum requirements and an agreement on the next draft

are expected to be completed.

The new Forestry and Wildlife law is needed to

fulfil the

conditions of the Free Trade Agreement (FTA) with the

United States.

Growth in exports to China

The China¨CPeru Free Trade Agreement (FTA) came into

effect on 1 March 2010. Following the FTA, Peruvian

exports to China have registered robust growth. The total

value of Peruvian exports to China in 2010 soared 33% to

US$5.4 billion from US$4.1 billion in 2009. Wooden

flooring were among the non-traditional timber products

which were able to make significant gains in sales to

China.

China is the main destination for Peru timber

exports,

accounting for 43% of the total value of Peruvian timber

exports.

9.

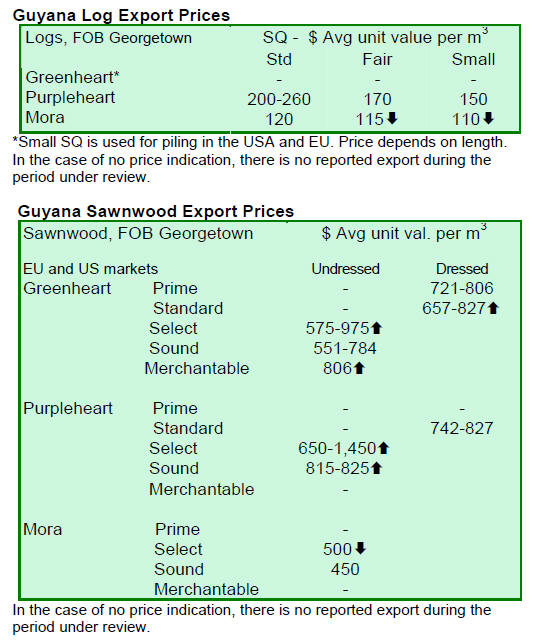

GUYANA

Timber prices trending upwards

During the period under review, there were again no

exports of greenheart logs which was one of the main

species used in domestic value-added production. Export

sales of purpleheart logs were brisk at favourable prices

especially for standard and fair sawmill qualities, while

mora prices retreated marginally during this fortnight

period.

For sawnwood, prices for undressed greenheart

(select

quality) increased from US$806 per cu.m in last fortnight

to US$975 per cu.m in the period under review. Undressed

greenheart (sound quality) attracted a high average price

of US$784 per cu.m, while prices for undressed greenheart

(merchantable) reached US$806 per cu.m. For undressed

purpleheart (select quality) prices shot up to US$1,450 per

cu.m, from US$650 recorded a fortnight ago, while upper

bound prices for undressed purpleheart (sound quality)

advanced to US$825 per cu.m from US$615 per cu.m.

However, the volume of exports was small.

Similarly, dressed greenheart attracted favourable

prices

for both prime and standard qualities. Guyana¡¯s Washiba

(Ipe) continued to be in demand in the North American

markets, fetching a high average price of US$US2,050 per

cu.m for this fortnight period. Splitwood prices also

climbed to US$1,182 per cu.m with the main export

destination being the Caribbean.

For the period under review, exports of value-added

products including wooden doors, indoor furniture,

mouldings, wooden utensils and ornaments also

contributed to total export earnings.

Booming housing sector drives domestic demand up

The government of Guyana is encouraging forest

concessionaires to optimise timber production under the

state¡¯s sustainable management plan in order to meet

increasing domestic demand for sawnwood driven by the

booming housing sector in the country.

Due to a projected increase in public spending on

housing

in 2011, domestic consumption of sawnwood is expected

to grow sharply by 40% from the level in 2010, to 300,000

cu.m in 2011.

In 2010, total production of logs production was

420,000

cu.m of which around half was exported. In order to meet

projected domestic and export demand for 2011, a

benchmark of 60% of the annual allowable cut has been

set for log harvest in forest concessions. At this level, the

rate of deforestation in Guyana can be kept at the current

low level.

The Guyana Forestry Commission is currently

granting

new concessions for the management of state forests to

designated communities in an attempt to improve the

livelihoods of forest communities and increase timber

production. In addition, with the establishment of three

kiln drying facilities across the country, Guyana¡¯s focus

remains on reducing log exports and increasing domestic

production of value-added products.

10.

BOLIVIA

Business Round Table in Bolivia

The 7th Business Round Table of the Timber Industry will

be held on 24-25 March 2011 in Santa Cruz, Bolivia.

Participants will include local and international timber

industry companies, as well as machinery and equipment

providers and consultants.

http://www.cfb.org.bo/CFBInicio/

Related News: