| Home: Global Wood | Industry News & Markets |

| Home: Global Wood | Industry News & Markets |

|

International Log

& Sawnwood Prices

|

|

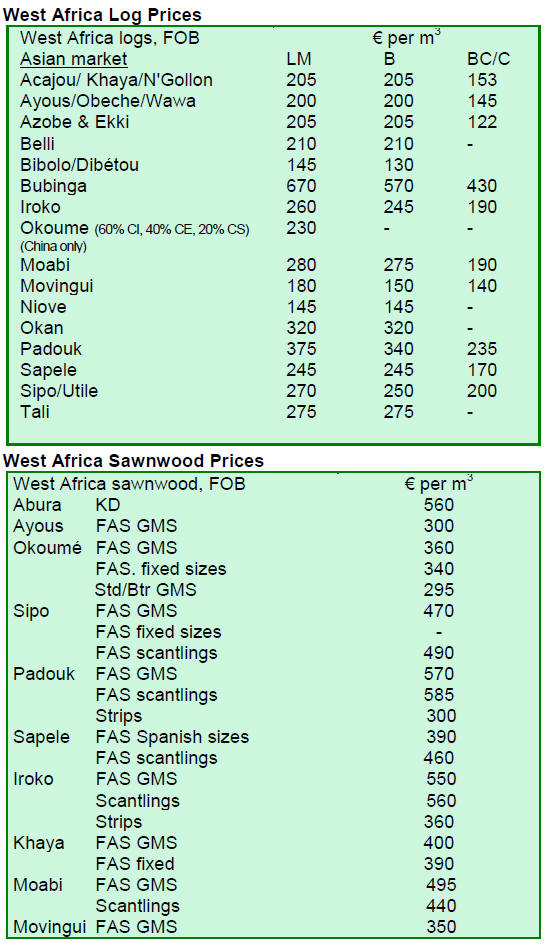

1. CENTRAL/ WEST AFRICA Sustained log demand from India and China For the West and Central African producers, sustained log demand from India and China is expected to maintain the stability in price through the first quarter. No price changes for logs and sawnwood are reported during the period under review, although, some producers are of the opinion that log prices for the prime species may firm up in the next few weeks. Prospects for sawnwood dependent on recovery in Europe Sawnwood prices will continue to be responsive to sudden fluctuations in demand as well as to how quickly producers are able to match supply with demand. For example, it is reported that the price of sapele sawnwood is once again weakening following expansion in its production despite falling demand. Generally, sawnwood prices have remained unchanged during the past four weeks. Cameroon to re-impose log export quota Meanwhile, there are continued rumours that Gabon may relax the total log export ban imposed since April 2010. Some observers were expecting an announcement of the relaxation last month but to date there is no indication of an imminent change. There is speculation that Congo Brazzaville may follow Cameroon in re-imposing the log export quota which has been relaxed to assist producers through the global recession in 2008/09. Buyers are observing the situation keenly as any changes may affect log supply and prices which have remained stable in the second half of 2010.

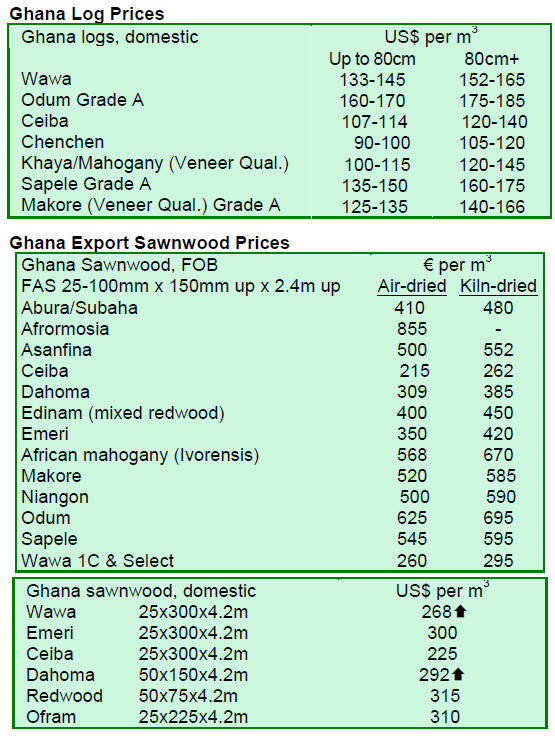

2. GHANA Higher costs pushing up timber prices Under the prevailing situation, timber operators are facing difficulties in stabilising their business and meeting market demand. Faced with a shortage of raw material, a hike in fuel prices and higher operational costs due to higher electricity and water tariffs imposed by the Public Utility Regulatory Commission (PURC) last year, producers are likely to pass on these costs to the consumers, thereby pushing prices of timber products up. Inflation eased in December In terms of economic growth, the World Bank has projected that Ghana will be the fastest growing economy in Sub-Saharan Africa, with a growth rate of 13.4% in 2011 and 10% in 2012. According to the World Bank, Ghana is in position to register strong economic growth particularly in the construction sector as large infrastructure projects are being implemented.

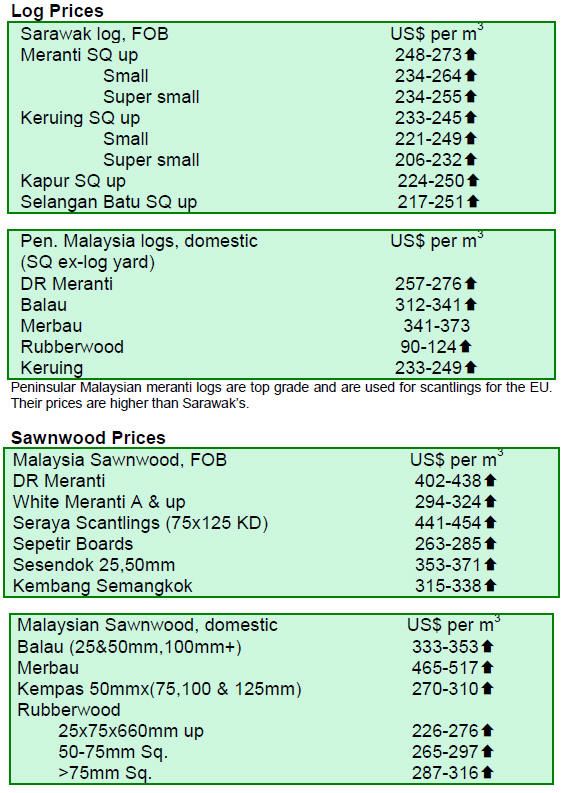

3. MALAYSIA Korea imposes anti-dumping duties on Malaysian plywood Anti-dumping duties have been imposed on eight Sarawak plywood suppliers including Subur Tiasa Plywood Sdn Bhd with the anti-dumping duty of 5.12%, while the duty of 6.43% was imposed on Jaya Tiasa Timber Products Sdn Bhd, Hwa Sen Veneer and Plywood Industry Sdn Bhd. An anti-dumping duty of 9.75% has been imposed on 5 companies of the Shin Yang group: Shin Yang Plywood Sdn Bhd, Forescom Plywood Bhd, Menawan Wood Sdn Bhd, Shin Yang Plywood Bintulu Sdn Bhd and Zedtee Plywood Sdn Bhd. The highest anti-dumping duty of 38.1% has been imposed on Sabah-based Sinora Sdn Bhd while the duty on all other Malaysian plywood manufacturers and exporters has been set at 8.76%. The variation in the imposition of the anti-dumping duties is due to the different selling prices and types of wood used. This is the first time anti-dumping duties have been imposed on Malaysian plywood in the international markets. Republic of Korea imported 530,000 cu.m of panel products from Sarawak in 2010, worth RM570 million. High price levels retained The other factor pushing prices higher is the continuing strong demand from China and India. China¡¯s demand for logs has increased worldwide since Russia, China¡¯s largest log supplier, imposed an export tariff on log exports. India¡¯s demand may be attributed to a steady rise in corporate capital expenditure for most part of 2010. This rise in corporate capital expenditure is expected to continue into 2011. Prices of plywood from Sarawak surged 8% to 14% in 2010 on the back of sustained demand from Japan which increased 12.1% in the first 10 months of 2010 compared to the same period in 2009. Plywood manufacturers are also optimistic that 2011 will be a profitable year if the current price levels are maintained or improved. Plywood manufacturers are optimistic that the housing starts in 2011 in Japan will be strong enough to support current price levels. The Japan housing starts in 2010 rose 20.4% in August, 17.7% in September and 6.4% in October, vis-¨¤-vis the same months in 2009. Building permits for October 2010 increased by 3.4% compared to the same month in the previous year. However, the housing starts and building permits in 2010 in Japan remained far behind the levels recorded in 2008. In support of the local timber industry, the Sarawak Forestry Department is likely to extend the 50% log export quota which is expiring in mid-2011. Malaysian exporters seek market opportunities in India Malaysian timber producers are planning new ventures and investments in India to increase their market share in the Indian market.

4.

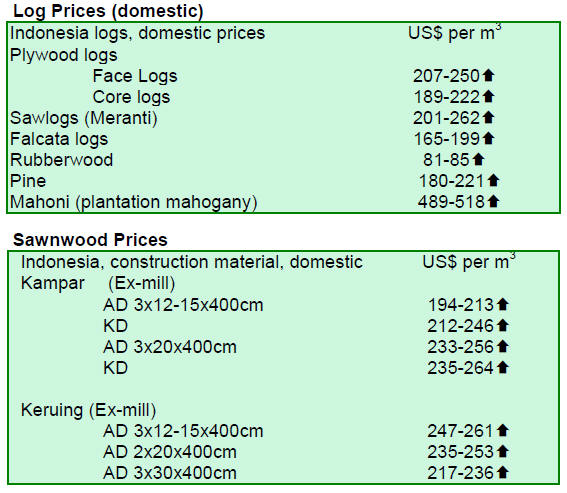

INDONESIA Implementation of 2-year moratorium postponed Two contrasting drafts for the moratorium have been submitted to the Indonesian president for approval. While the Ministry of Forestry seeks to enforce only a ban on new permits to clear primary forests and peatlands, the Indonesian Presidential Delivery Unit calls for the inclusion of secondary forests, the review of existing permits and the extension of the moratorium beyond 2 years. The Presidential Delivery Unit also proposed incentives and land swaps to be included as a form of compensation to existing permit holders. The Ministry of Forestry has identified 35 million hectares of land for business development. To date, 9 forest plantation companies have submitted proposals to develop 320,000 hectares of plantation forests. Any permit to develop these land areas depend on the formalisation of the moratorium. The proposed moratorium will protect up to 43.8 million hectares of natural forests and up to half of the 20 million hectares of peatlands in the country. Indonesia aims at reducing greenhouse gas emissions by 26% before 2020. Forestry project budget for 2011 The project budget proposed for 2011 comprises 402 programmes and activities to be executed by 46 central working units, 185 technical working units and 171 working units in the provincial and regency levels. Higher timber prices on the back of robust growth in

property demand Housing demand in Indonesia has reached 8 million new units per year as the Indonesian economy continues to recover and purchasing power improves. The interest rates for housing loans, known as housing credits (KPR), have dropped to 10% ¨C 11% and this has boosted housing activity in the country.

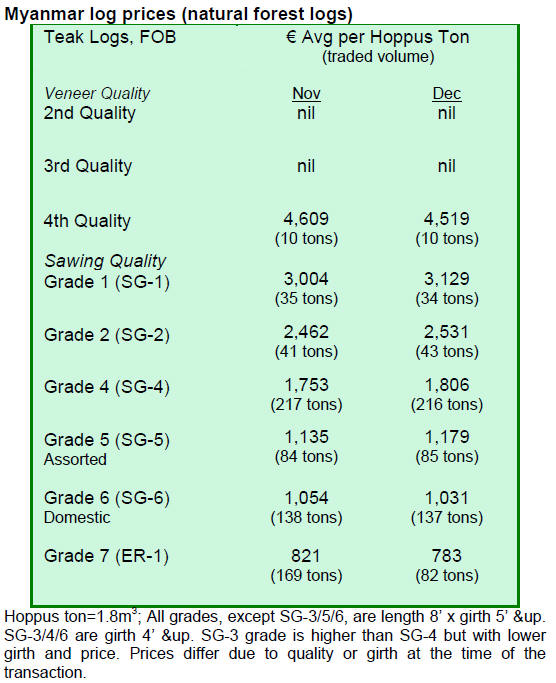

5. MYANMAR Markets

remain slow

Purchases of Myanmar teak by country in December

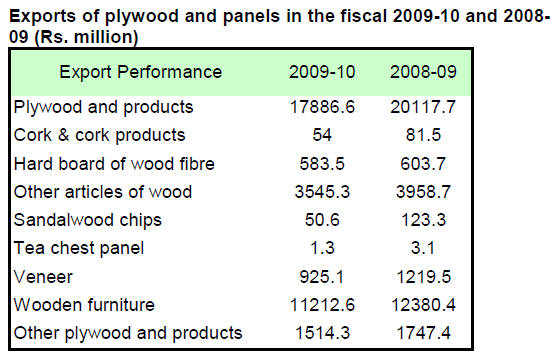

6. INDIA Industrial growth eases GDP growth from the beginning of the fiscal year to date was 8.9%. Exports of plywood and panels

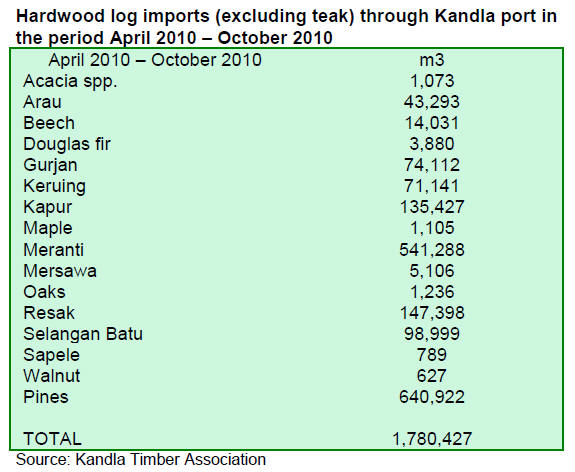

Imports of hardwoods

Plywood imports from China pose stiff competition

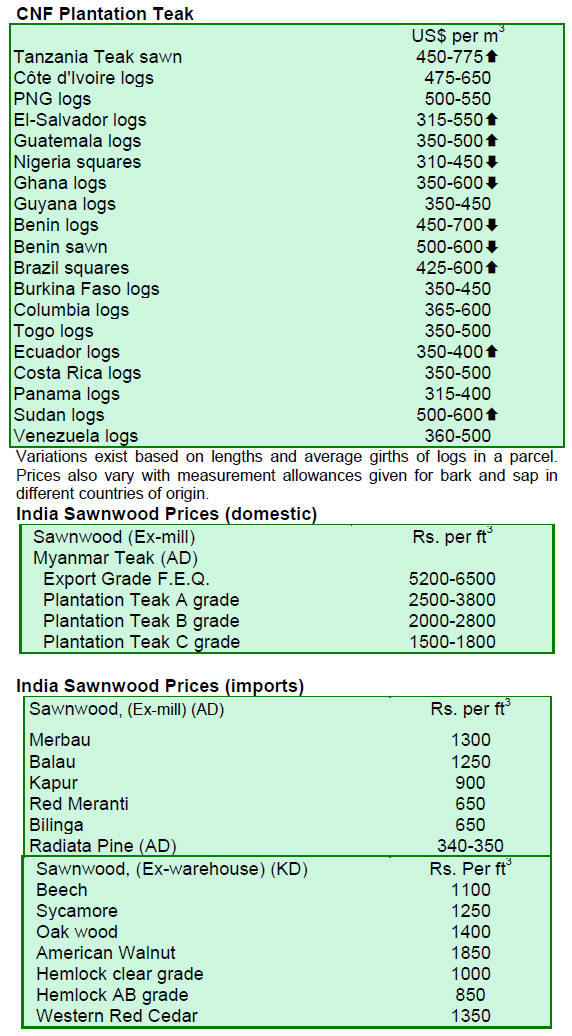

to local manufacturers Active auction sales in government depots Since prices of imported teak are increasing, the impact on depot sales is also apparent. Prices were up by 15% to 20% compared to previous auctions. Long length teak logs fetched Rs.2000-2200 per cu.m, medium quality Rs.1500-1700 per cu.m and lower grades were priced at Rs.900-1000 per cu.m. The hardwoods like Adina, Laurel and Pterocarpus marsupium (kinowood) fetched Rs.800-850 for select qualities and Rs.325-400 for lower grades. Demand is good for these species, but supplies are very limited due to conservation and effective control by the Forest department. Kerala afforestation programmes receive UN

recognition As part of the programmes, a total of 18.7 million saplings have been distributed and planted across the state, contributing to the 'Plant for the Planet: Billion Tree Campaign' of the UNEP.

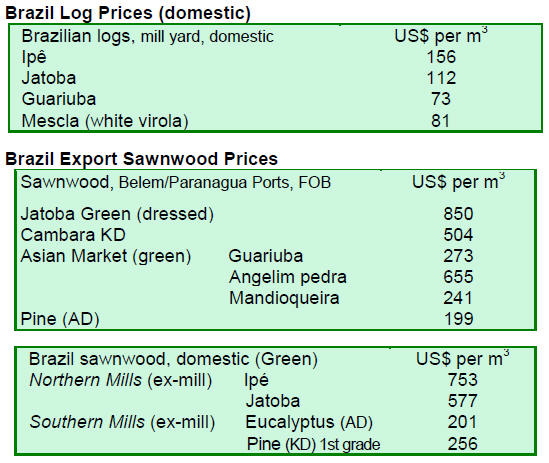

7. BRAZIL Brazilian furniture exports on the mend According to the Ministry of Development, Industry and Foreign Trade (MDIC), Brazilian furniture exports declined between 2006 and 2008. However, exports increased in 2010 in line with Brazil¡¯s robust economic growth. In the first half of 2010, Brazilian furniture exports amounted to US$367 million, up 16.9% from the same period in 2009, according to the Secretary of Foreign Trade (Secex). However, Rio Grande do Sul registered the lowest rate of growth in exports of only 5.5% compared to the first half in 2009. Santa Catarina is the leading state in furniture exports followed by Rio Grande do Sul. Timber production declining in the Amazon The depreciation of the US dollar has had a negative impact on exports and commodity prices. In addition, stricter governmental control, monitoring and efforts in combating illegal forest activities are the factors contributing to the decline in timber production. In 2010, revenue from logging in the Amazon was US$2.5 billion. The number of sawmills decreased by one third and jobs in the forest sector dropped from 344,000 to 203,000. Logging in the Amazon is mainly conducted using tractors and cables causing damages to the remaining forests. One fifth of sawnwood in the Amazon is produced at low quality by small-size sawmills which lack proper tools and training. As a result, timber yield is only at 28% to 45% of the logs processed and the rest is waste. Most of the logs (72%) are processed into rough sawnwood, from which only 22% is exported mainly to the US. In the domestic market, the state of Sao Paulo is the main consumer, accounting for 17% of the demand. Deforestation monitoring system for the Amazon The model shows that till July 2011, some 3,700 square kilometers of forested area will be threatened by deforestation, 67% of which will be located in Par¨¢, which has the highest rate of deforestation in the country. Some 13% of the threatened area is located in the state of Mato Grosso. According to the study, roads are the major factor causing deforestation. Regions close to BR-163 highway, linking Cuiab¨¢ (MT) to Santarem (PA) in the Amazon, are the areas most threatened by deforestation. The study also assessed the existence of roads constructed illegally by loggers and land speculators. According to Imazon, thousands of miles of these roads have been constructed in the forests. Most of the threatened forests (59%) are on private land or under some kind of land use. This is followed by the agrarian reform settlements which account for 25% of the threatened forests. On the other hand, the risk is lower on indigenous lands, which represent 4% of the total threatened areas. EU funding for reducing deforestation in Par¨¢ The three year project will be implemented by the MMA, with technical support from FAO in partnership with the Environment Secretariat of Par¨¢ State and the Municipal Environment and Tourism Secretariat of São Felix do Xingu. 8. PERU

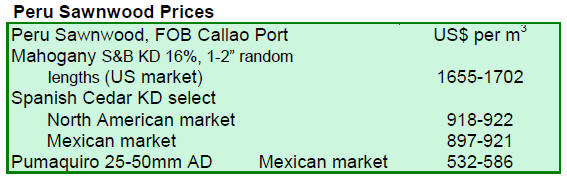

Determining the national export quota for mahogany The general forest management plans (PGMF), annual operating plans (POA), timber harvesting permits and annual performance reports shall be submitted by the concession holders or native communities to the Regional Forestry and Wildlife Authority for approval. After the approval, the information will be forwarded to the CITES Management Authority of Peru. The national export quota for mahogany is revised by the CITES Management Authority of Peru every year after 31 May, the expiry date of each annual quota.

OSINFOR steps up supervision on concessions, permits and authorisations The progress is attributed to the strategic alliances with indigenous communities, forest concessionaires and government agencies. In addition, 11 OSINFOR offices have been established in various regions of the country: Loreto (3 offices), Madre de Dios (2 offices), Ucayali (2 offices), San Mart¨ªn, Lambayeque, Huanuco and Junin.

Congress debate on draft law deferred

9. GUYANA

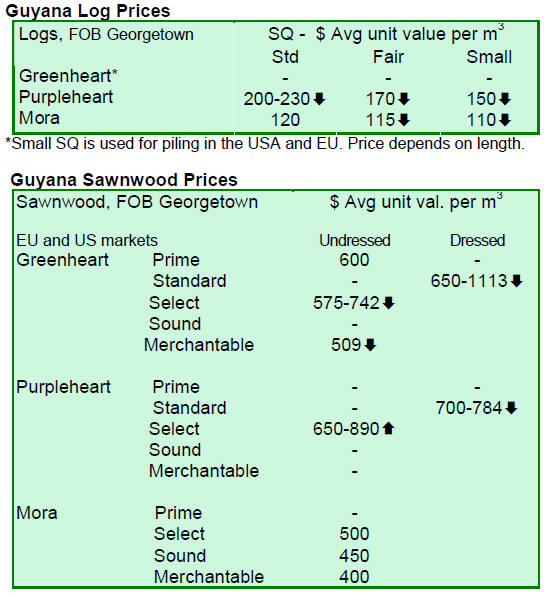

Timber trade remains quiet following holidays For sawnwood, undressed greenheart fetched favourable prices for all qualities except sound quality. Undressed purpleheart prices hit US$890 per cu.m in select quality while undressed mora prices continued to hold. However, prices for dressed greenheart and purpleheart were slightly down in the period under review. Guyana¡¯s Washiba (Ipe) attracted an average price of $US1,150 per cu.m. Dressed bulletwood (Macaranduba) reached US$954 per cu.m, dressed kabukalli (Cupiuba) US$975 per cu.m and undressed locust (Courbaril) US$1,166 per cu.m with the Asian, Caribbean and North American markets being the main destinations. Roundwood and fuelwood made notable contributions to the total export earnings with favourable prices in this fortnight period. Splitwood prices also held on a high level of US$956 per cu.m. For the period under review, exports of value-added products were limited. Some products such as doors and mouldings made from crabwood (Andiroba), locust (Courbaril), kabukalli (Cupiuba), purpleheart (amarante) and tauroniro (Cumaru) contributed to total export earnings.

Related News:

|

||||||||||||||||||||||||||||||

|

Abbreviations

|

||||||||||||||||||||||||||||||

|

Source:ITTO'

Tropical Timber Market Report

|

CopyRight(C) Global Wood Trade Network. All

rights reserved.