| Home: Global Wood | Industry News & Markets |

| Home: Global Wood | Industry News & Markets |

|

International Log

& Sawnwood Prices

|

|

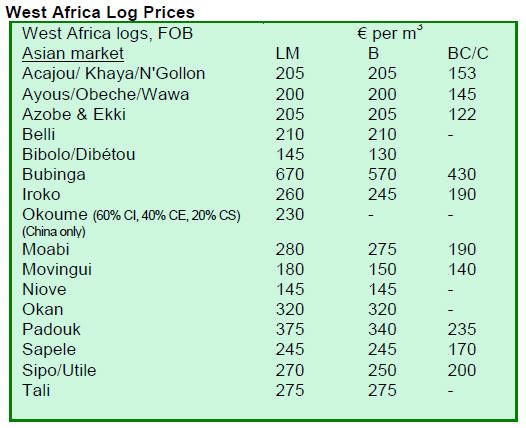

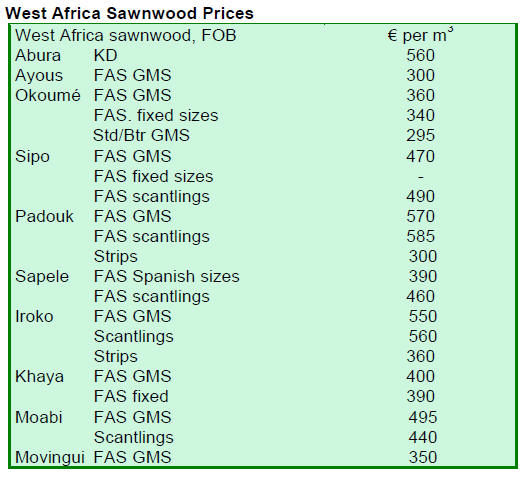

1. CENTRAL/ WEST AFRICA Log market sustained by strong demand from China and India Adverse weather conditions are expected to impact on the economic situation in UK. Portugal and Spain continue to face severe financial difficulties and prospects for the timber based industries in these countries remain dull. Nevertheless, China and India continue active buying of West and Central African logs. Overall, log traders and exporters have had a relatively good year; with steady market situation and level of prices due to the Gabon log export ban and the log export relaxation by Cameroon and Congo Brazzaville. Better markets for some processed products Currently, sawnwood producers are worried that any over-production could affect prices. According to analysts, producers in the region have to accelerate efforts in achieving full certification for their products, in order to keep market shares in Europe and benefit from the recent greater interest in premier red species of sawnwood from the US market. Markets for veneer have reportedly improved, but the trade in other value-added products has yet to show any sign of full recovery to pre-recession volumes and diversification. West and Central African manufacturers are slowly re-activating processing facilities, but as the current market is still dull, any increase in production is expected to have an adverse impact on price levels. In addition, as the winter season is slowing down business in Europe, there is little incentive for West and Central African producers to increase production.

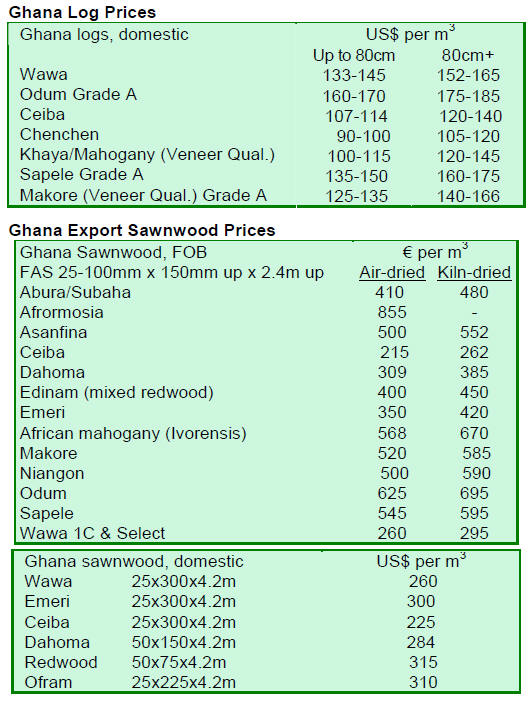

2. GHANA

Second JMRM meeting on VPA convened The parties discussed the progress in the implementation of the Agreement. Ghana provided an update of progress in respect of the various envisaged components for the Legality Assurance System (LAS). LAS establishes institutional and procedural arrangements to verify the legal origin of timber through a verification and licensing scheme for all commercial timber products destined for the international and domestic markets. The update indicated Ghana¡¯s progress in developing institutional arrangements to manage the LAS effectively. In this regard, the establishment of the Timber Validation Division at the Forestry Commission and the Multi-Stakeholder Implementation Committee were proposed. The Minister of Lands and Natural Resources noted that the VPA will have an impact on livelihoods, particularly among local communities. Both the EU and Ghana have initiated studies to address these impacts and challenges. In addition, Ghana will take concrete actions to link together the Plantation Development Programme, sustainable supply of legal timber, and the Forest Law Enforcement Governance and Trade (FLEGT). According to Ambassador Maerten representing the EU, the recent adoption of the EU legislation on illegal timber provided a significant push for Ghana and other countries negotiating the VPAs towards their full commitment. The legislation provides justification and reward to countries with VPAs and constitutes an incentive to initiate negotiations on the VPA. Ghana became the first timber producing country to sign a VPA with the EU in November 2009. Since then, the Republic of the Congo and Cameroon have also signed VPAs, while seven other countries are currently in the negotiation process. The next series of meetings of the JMRM will be held in Accra in June 2011.

3.

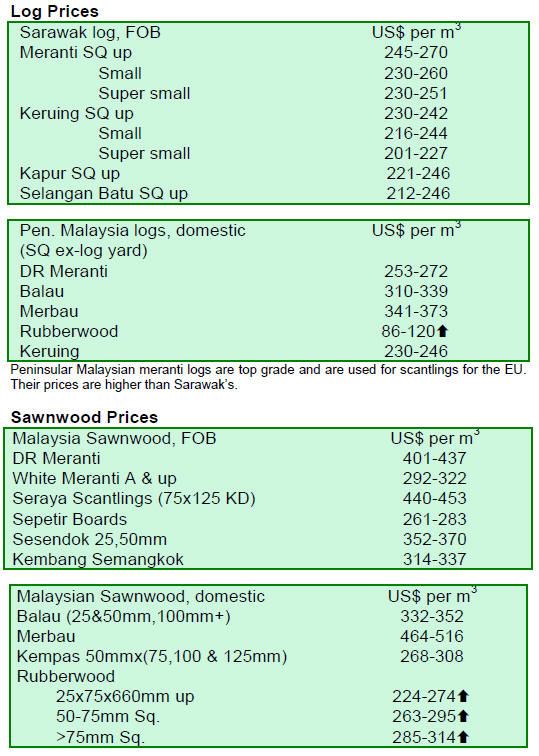

MALAYSIA Sarawak plywood manufacturers seek certification to expand

market share The Sarawak Timber Industry Development Corporation (STIDC) reported that out of 42 plywood mills operating in the state, 24 have already been certified under the Japanese Agricultural Standard (JAS), 15 under the California Air Resources Board of the California Environmental Protection Agency, and 12 under European Union standards. In the first half of 2010, Sarawak exported 1.46 million cu.m of plywood worth RM2 billion, compared to 1.7 million cu.m valued at RM1.45 billion in the same period of 2009. In the first half of 2010, plywood exports from Sarawak to Japan amounted to 663,710 cu.m, valued at RM939 million. The Republic of Korea was the second largest export destination for Sarawak plywood with 283,493 cu.m worth RM316 million, followed by the Middle East countries with exports totalling 174,887 cu.m worth RM224.4 million. Other major export destinations for Sarawak plywood include Taiwan P.o.C, the US, China, Hong Kong, the Philippines, Vietnam and the EU. In 2009, the plywood industry in Sarawak employed 9,000 workers, both foreign and local, representing 20% of the total of 45,100 workers employed by the Sarawak timber industry. The plywood sector is thus the main employer within the timber industry in Sarawak.

4.

INDONESIA Improved demand for Indonesian furniture in

Europe and US According to the Surakarta branch of the Indonesian Furniture Association (Asmindo), improvement in orders began in October this year for deliveries to be made before December 2010. It is estimated that orders for the period from October to November 2010 increased by 20% over the period from January to September 2010. In the past, some 50 furniture manufacturers in Surakarta shipped an average of 400 containers of furniture to the EU and US annually. Sri Mulyani, the major furniture manufacturer in Surakarta noted that orders for desks and tables are also coming from Australia and Italy. Orders have been increasing since September this year.

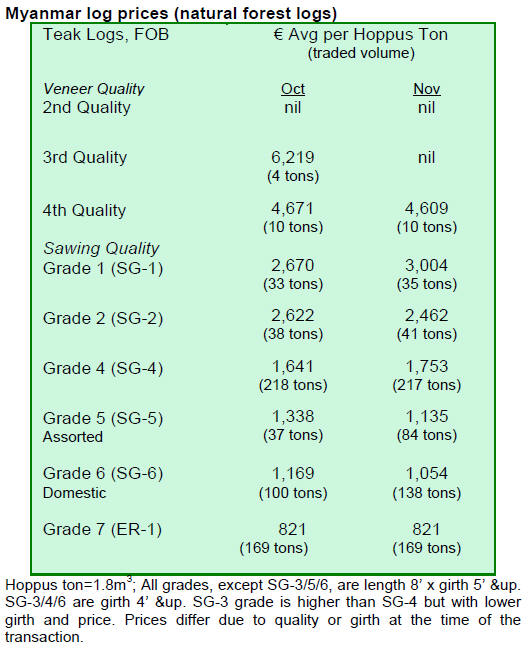

5. MYANMAR Pyinkado

prices trending downward Pyinkado log prices reached as high as US$1000 per Hoppus ton for large girths, but towards the end of the year prices retreated to US$850 per Hoppus ton. Buyers complain that sizes of pyinkado logs are getting smaller and supply is short.

Teak from plantations on the rise Myanmar teak is of superior quality as it is sourced from natural forests. This is an advantage that keeps it in demand. However, teak grades and girths have declined over the years. Experts are worried that the situation for teak will be the same as those for padauk and tamalan. The Timber Merchants Association has suggested that timber extraction might be reduced in the coming year. However, the Myanmar Timber Enterprise (MTE) has yet to confirm this and the harvest quota for the next year is still pending. Some experts suggest that the harvest quota will remain more or less unchanged. Teak plantations are expected to expand but plantation teak is of no comparison to naturally grown teak in terms of hardness, beauty, durability and stability.

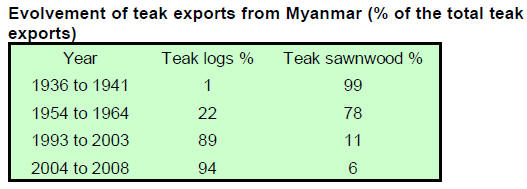

Myanmar urged to reduce log production and export more value-added

products From 1936 to 1941, exports of teak logs accounted for only 1% of the total teak exports. The average annual of teak log exports was 2,397 cubic tons during the period. Between 1955 and 1956, Europe and Japan began producing veneer resulting in the share of teak log exports increasing to 22% of the total, with the balance of exports accounted by sawn teak. Most of the exported teak logs were grade 4 and higher and mainly for veneer production. India as the largest importer ceased imports of teak from Myanmar from 1963 to 1983, but resumed purchasing after 1983. India that used to buy teak squares, has shifted to procuring more low grade teak logs.

Myanmar¡¯s forest policy is to reduce log exports and increase production of value-added wood products. According to experts, Myanmar should reduce log production to mitigate climate change and degradation and promote exports of more value-added products.

6. INDIA Robust economic growth sustained in

second quarter In the second quarter of the fiscal year 2010-2011, exports grew sharply by 21.6% compared to the same period last year. India targets forest cover of 33% of land area by

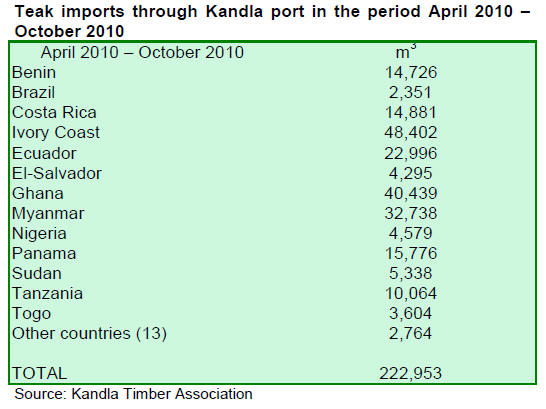

2020 The forest cover in India is currently 23% of the total land area and the plan is to expand it to 33% within the next ten years. Better soil and water conservation and afforestation efforts will result in expanding agriculture, less migration to cities and improved livelihoods. The efforts of the government of India are supplemented by plantations of poplar, eucalyptus, casuarinas, semul, gmelina among others species, in order to improve raw material supply for the paper, plywood and panel industries. NGOs are establishing plantations for fruit and medicinal plants including mango, tamarind and ebony. Established plantations of eugenia, mimusops, subabul, sissoo, neem and acacia provide timber for the construction and furniture industries. Teak log import statistics

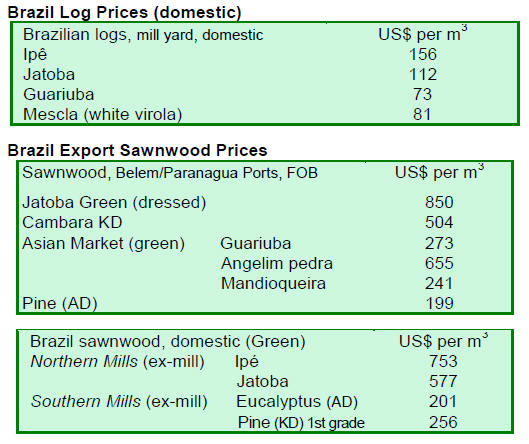

7. BRAZIL BAMA meets 2010 deforestation reduction

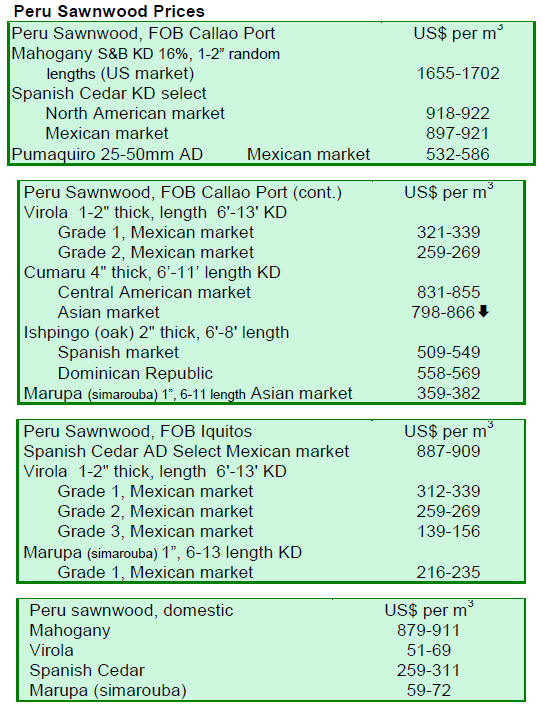

targets The main indicator for IBAMA¡¯s work on combating forest fires and illegal forest activities is the deforestation rate. It is estimated that the annual deforestation will be reduced to 6,450 square kilometers in 2010, a 14% decrease over the previous year and the lowest in the last 20 years. Brazilian forest production expanded in 2009 In 2009, the Brazilian roundwood production totalled 122.15 million cu.m. Out of the total 87.5% came from forest plantations and 12.5% from natural forests. Among the states, the largest timber producer is the state of Par¨¢ with annual production of 5.97 million cu.m of roundwood accounting for 39.2% of the national total, followed by Mato Grosso with 3.92 million cu.m (25.7%), and Rondônia with 1.35 million cu.m (8.9%). In 2009, the total production value of plantation forests and natural forests was BRL13.6 billion. A share of 66.4% came from plantation forests and 33.6% from natural forests, while in 2008 the shares were 69.3% and 30.7% respectively. Timber production from natural forests amounted to 15.2 million cu.m in 2009, up 7.9% from 2008. The production value of natural forests totalled BRL4.6 billion in 2009; BRL3.9 billion came from timber production and BRL685 million from non-timber production. Balsa wood production in Mato Grosso In the state of Mato Grosso, the planted balsa wood area totals 3,700 hectares which is managed by 105 producers. First harvests of balsa wood plantations are made at age of 3-4 years when trees reach the height of 20 meters and 35 cm in diameter. Currently, 20% of the total balsa wood plantation area is ready for harvests while the balance is less than 2 years old plantation trees. There is no processing industry for balsa wood in the state and thus it is sold as roundwood. The Corporation for Agricultural Research, Technical Assistance, and Rural Extension of Mato Grosso (EMPAER) has been carrying out research on balsa wood during the past five years analysing growth data and production costs for marketing purposes. EMPAER together with Embrapa (Brazilian Agricultural Research Corporation) are conducting research on characteristics of balsa wood to meet higher standards and commercial value. Timber production levels off in November In Par¨¢ state, November prices of timber products were also stable. Only maçaranduba panel average price declined 0.56%. In November 2010, the total Brazilian timber, pulp and paper export value amounted to US$729 million, down 1.9% from October 2010 with US$743 million. For Brazilian timber exports, the export value totalled US$156.9 million, decreasing 5% from US$165.3 million exported in October 2010. 8. PERU

October wood product exports dropped significantly Three biggest buyers were China, the US and Mexico, together accounting for 78% of the total export volume. In October, Sweden increased imports of sawnwood, plywood and decking materials compared to last year. Columbia increased imports while Venezuela and the US reduced their wood product imports significantly from last year, by 50% and 45% respectively.

Main items of wood product exports Semi-manufactured products were exported mainly to China which accounted for 78% of the total exports in the period. Swedish and Israeli importers substantially increased their purchases of semi-manufactured products in October. Sawnwood exports made up 35% of the total exports. In the period from January to October 2010, sawnwood exports totalled US$49 million, up 12% over the same period last year. The main destination was China with a 34% share of the total sawnwood exports. Veneer and plywood exports in January ¨C October valued at US$13.2 million, an increase of 9% over the same period last year. Veneer and plywood are exported mainly to Mexico which accounted for 93% of total exports. In the period from January to October 2010, exports of furniture and its parts were valued at US$5.5 million, representing a 8% decline compared to the same period last year. The US is the main market for furniture accounting for 52% of the total exports. During the period, exports to the US and Chile collapsed compared to last year, down 58% and 32% respectively.

Heavy fines imposed on illegal logging According to the General Directorate of Forestry and Wildlife Fauna (DGFFS), any timber products without required documentation will be seized, as well as tools and machinery used in illegal activities. If a concession holder is suspected of any violation of law, all activities, licences and permits will be suspended from the time of investigation till the final decision.

Peru¡¯s natural forest cover is second largest in South America The total reforested area stands at 0.9 million hectares in the country. The estimated total forest plantation area is 40,000 hectares, mainly located in La Libertad, Cajamarca, Cusco, Apurimac and Ancash. The potential area for reforestation in Peru is more than 10.5 million hectares which is a good opportunity to expand the forest plantation area, say an analyst.

Strategic Agenda for Amazonian Cooperation During the meeting, the Strategic Agenda for Amazonian Cooperation was designed, an effort to agree on guidelines for the short, medium and long term sustainable development and cooperation in the Amazon.

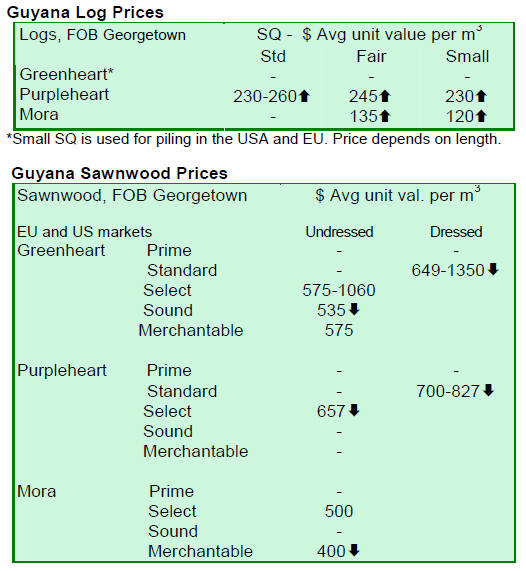

9. GUYANA

Demand from Asia drives timber prices up For sawnwood, undressed greenheart prices gained for the select quality. Undressed mora prices continued to hold, as well as prices for dressed greenheart. Prices for dressed purpleheart gained slightly in the period under review. In the period under review, Guyana¡¯s Washiba (Ipe) attracted a higher price average at $US1,800 per cu.m with the main export destination being the US market. Roundwood, including both piles and posts, showed favourable prices in this fortnight period with the main destinations being Europe and the Caribbean. Average prices for splitwood inched up to US$1,000 per cu.m. For the period under review, value-added products made notable contributions to total export earnings. The major exported products were handicrafts, mouldings, wooden utensils and ornaments with the main destination being the Caribbean. Crabwood (Andiroba) was one of the main species used for the production of these value-added products.

Second kiln drying facility commissioned in Guyana Export markets for lumber can attract a market price of US$1,000 per cu.m, compared to about US$600 per cu.m currently received by exporters. Kiln drying prevent stains and degradation of wood. In addition, the weight of dried wood is lower. Kiln dried sawnwood is mostly utilised by the furniture manufacturing sector.

Related News:

|

||||||||||||||||||||||||||||||

|

Abbreviations

|

||||||||||||||||||||||||||||||

|

Source:ITTO'

Tropical Timber Market Report

|

CopyRight(C) Global Wood Trade Network. All

rights reserved.