|

1.

CENTRAL/ WEST AFRICA

Log demand remains steady

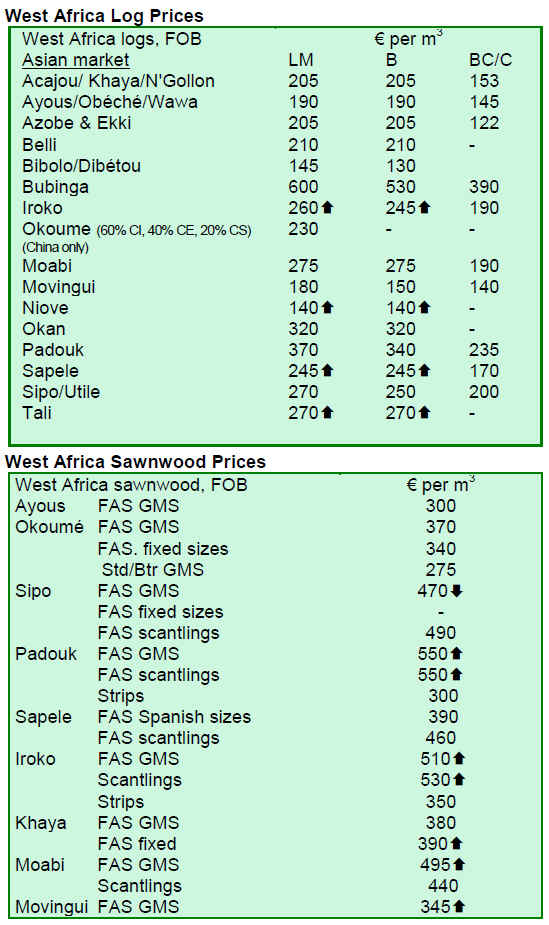

For the period under review, some price changes were experienced from September. Prices firmed as a result of good demand from China, India and Vietnam.

Iroko logs are still in good demand and sawnwood prices also gained due to increased demand from European and Asian buyers. Sapele log prices are a little higher and demand for niove logs for the Indian market remains steady lifting prices. Okoum¨¦ log prices also inched up, even though supply from Equatorial Guinea and Congo Brazzaville is now sufficient to meet demand in consumer countries, says an analyst.

Okoum¨¦ logs from Congo Brazzaville have been used to replace what was sourced from Gabon before the log export ban. However, there remains a possibility that Congo Brazzaville may at some point revert to the limits on log exports that were in force up to the early months of this year, says an analyst.

In Cameroon log exports are continuing and due to the high demand there are shortages of azobe and ayous logs for domestic processing industries.

European sawnwood demand still sluggish

Sawnwood demand has remained steady except from Continental Europe where most buyers are unsure about business prospects over the coming winter months. The market in Italy is more active with demand for ayous sawnwood but otherwise European trade is reportedly dull.

Demand from Middle East countries is moderate and African exporters have been making headway in competition against Malaysian exporters suffering from higher ocean freight costs and an appreciating Ringgit.

Gabon eyes employment through processing industry

Major industries in Gabon now have begun to adapt to the log export ban and are starting to seek new processing opportunities. Due to reduced harvest volumes, the sector currently employs fewer people.

Since processing is relatively more labour intensive, it is hoped that there will be more job opportunities as mills increase their capacities and outputs.

2. GHANA

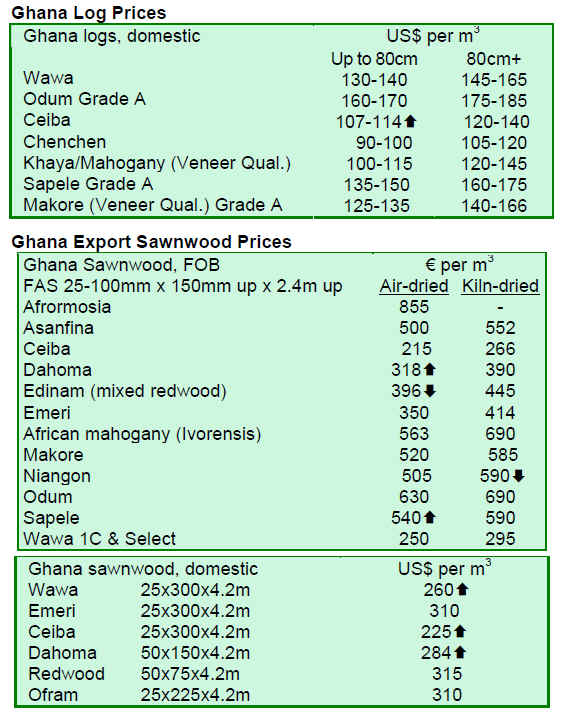

Ghana issues more permits in second quarter

The Timber Industry Development Division (TIDD) of the Forestry Commission vetted, processed, and approved 1,974 export permits during the second quarter of 2010 covering shipment of various timber and wood products through the ports of Takoradi and Tema as well as for overland exports to neighbouring ECOWAS countries (the Economic Community Of West African States).

The regional offices in Sunyani, Kumasi and Tema and the head office in Takoradi accounted for 3.6%, 5.3%, 25% and 66% of the total export permits issued during the second quarter respectively.

Compared to the first quarter of 2010, second quarter approvals increased sharply by 22.5%. The number of sawnwood export permits rose as did the number of export approvals for rotary veneer, sliced veneer, veneer layons, mouldings and block boards. However, the number of export permits for flooring, teak billets/poles/logs, gmelina billets/poles and rubberwood billets dropped considerably.

Sawnwood (both air dried and kiln dried) continues to account for the largest share (53%) of the total export permit applications followed by plywood (18.5%), sliced veneer (9.5%), mouldings (9.1%), rotary veneer (3.7%) teak billet/poles (2.9%)

The number of export permits approved for sawnwood (both air dried and kiln dried) for the months of April, May and June were 356, 351 and 339 respectively.

In the second quarter of 2010, a total of 694 export permits, covering about 43,380 cu.m of timber products, were granted to a number of timber companies to export sawnwood, block boards, sliced veneer and plywood by road to Burkina Faso, Nigeria, Niger, Benin, Mali and Togo.

Special permit exports

During the period under review, six special export permits were issued solely for Takoradi shipments including 84 cu.m of kiln dried okoum¨¦ mouldings and 59 cu.m of kiln dried iroko decking strips. These products were shipped by Machined Wood Ltd to their clients in Italy.

The mouldings were manufactured from okoum¨¦ sawnwood imported from Gabon while the decking strips were made of iroko sawnwood from Cameroon. The total value of these shipments was Euro 100,132.

3.

MALAYSIA

New tax incentives to promote forest plantations

A new tax incentive regime will soon be in place to promote the development of large-scale forest plantation projects in Malaysia. The incentive is planned to cover both planting and harvesting phases.

The new tax incentives are provided under the Income Tax Rules 2009 (Deduction for investment in an approved forest plantation project) and the Income Tax Order 2009 (Exemption) (No. 10), which are effective until the end of 2011.

The Tax Exemption Order will allow plantation companies to offset the costs during the planting period against the income from the harvest. The costs can be fully deducted from the aggregate income during the first 10 years of a new forest plantation project, and 5 years for an expanded forest plantation project. According to the Sarawak Timber Association (STA), investments into any approved forest plantation project of a subsidiary by a holding company may now be deducted at the beginning of the planting period for the purpose of determining the adjusted income of the holding company, resulting in lower income tax for the holding company.

In addition, forest plantation companies are allowed to claim a reinvestment allowance for approved plantation projects. The allowance will be credited through the Exempt Income Accounts for the purpose of declaring dividends. Dividends received by holding companies will not be subjected to taxation.

Six major timber groups in Sarawak including Rimbunan Hijau Group, Samling Global Ltd, WTK Holdings Bhd, Shin Yang Forestry Sdn Bhd, KTS Forest Plantations Sdn Bhd and Ta Ann Holdings Bhd have welcomed this new tax incentive regime. These groups have been given approval by the Sarawak state authorities to reforest more than 1 million hectares of logged-over areas. The six groups are also among 41 active forest plantation licence-holders in Sarawak.

With the targeted 1 million hectares of forest plantations to be developed, Sarawak could double its supply of raw materials for its timber processing industry. Currently, Sarawak produces about 10.4 million cu.m of logs per year. Some 60% of the logs harvested are reserved for local processing industries and the balance is for export. As of 2009, up to 255,000 hectares of forest plantations worth RM2 billion in investments (RM7,843 per hectare), have been developed in Sarawak against the set target of 500,000 hectares. Three main fast-growing commercial tree species favoured in forest plantation projects are acacia (Acacia hybrid), kelempayan (Neolamarckia cadamba) and binuang (Octomeles sumatrana). The average establishment cost of all these three species is about RM8,200 per hectare.

The Federal Government grants soft loans to fund forest plantation projects based on the forest plantation area. Applications for such a loan are restricted to 5,000 hectares per application. Earlier, the Ministry of Plantation Industries and Commodities had estimated that some RM1.1 billion was needed to develop 150,000 hectares of forest plantations (RM7,333 per hectare) nationwide from 2006 to 2013.

Intensified innovative R&D required to meet 2020 export target

The Ministry of Natural Resources and Environment Malaysia, stressed that innovative research and development initiatives have to be intensified in order to achieve the target of RM53 billion in wood and timber product exports by 2020, as outlined in the National Timber Industry Policy.

In order to achieve the target, at least 60% of export earnings must derive from downstream products and the balance 40% from primary processed products.

Exports of Malaysian wood and timber products generated RM19.5 billion in revenue and the industry employed around 300,000 people in 2009. The ministry stated that the industry must respond to the changes in global business environment promptly or risk losing its market share.

Financing for development of local FSC standards

The HSBC Bank Malaysia Bhd will provide financing facilities up to RM150,000 in its partnership with Forest Sustainability (M) Sdn Bhd (FSM), to help develop the Forest Stewardship Council (FSC) standards in the country.

HSBC added that by providing support for the development of local FSC standards, the bank is not only helping the industry at large but also reinforcing its strong commitment to the forestry sector. Local FSC standards are expected to help create more international markets for Malaysian timber products.

The local FSC standards are expected to be ready by the end of year 2011.

4.

INDONESIA

Lack of legally defined border status of forests in Indonesia

A report by the Supreme Audit Agency (BPK) revealed that less than 5% of forest areas in the five provinces implementing REDD Plus programme funded by Norway have legal border status. These five provinces are Riau, Jambi, Central Kalimantan, East Kalimantan and Papua. In terms of forest area, Central Kalimantan has an estimated 15 million hectares of forests, East Kalimantan 14 million hectares, Papua 40 million hectares, Riau 9 million hectares, and Jambi 2.17 million hectares.

The report noted that legally defined boundaries in Central Kalimantan province account for only less than 1% of the total forest area, while the coverage in East Kalimantan is 4%, Papua 5%, Riau 6% and Jambi 1%. Such a lack of legally defined forest boundaries will make it difficult for Indonesia to develop and operate the MRV (monitoring, reporting and verification) system. The MRV is a tool in the REDD Plus scheme to measure and report emission reductions in forests.

The Ministry of Forestry Indonesia noted that the lack of legally defined forest boundaries will not affect the implementation of the MRV system as the planned system will employ satellite images to monitor land cover changes. The ministry has plans to hire a third party to speed up the determination of forest borders in the country, including those between state forests and community forests. As of July 2010, the ministry has completed defining 219,606 km of border lines for 282,873 square kilometres of forests. Plans are ahead to define another 250,000 km of forest border lines over the next four years.

Indonesia calls for closer forestry cooperation with China

The Ministry of Forestry Indonesia is calling for closer collaboration with China in the area of forestry development, especially in the usage of non-timber forest products such as rattan and bamboo. China has the technology to produce paper from bamboo while Indonesia¡¯s utilisation of bamboo and rattan is still limited.

During a recent visit in Beijing, the Minister of Forestry Indonesia signed a five-year agreement on the sharing of forestry management information with the State Forestry Administration. In addition to the usage of non-timber forest products in paper production, the agreement addressed also the usage of biomass energy from sustainably managed forests, forest land rehabilitation, social forestry, cooperation on wildlife and plant protection, and the sustainable use of flora and fauna.

China has the fifth largest forest area in the world. A total of 1.25 million square kilometres of forests in China is equivalent to 75% of Indonesia¡¯s total land area. The Ministry of Forestry Indonesia noted that the Chinese administration has developed environmentally friendly economic activities such as community forest programmes, under which communities are able to lease land from the state for a period of 30 to 35 years for community forestry projects. The Chinese government stated that through these programmes there has been a significant increase in the volume of planted trees by local communities.

Bilateral cooperation on forestry development between Indonesia and China was initiated in 1992 following the signing of agreements on forest management and conservation, including research, training and extension work.

5.

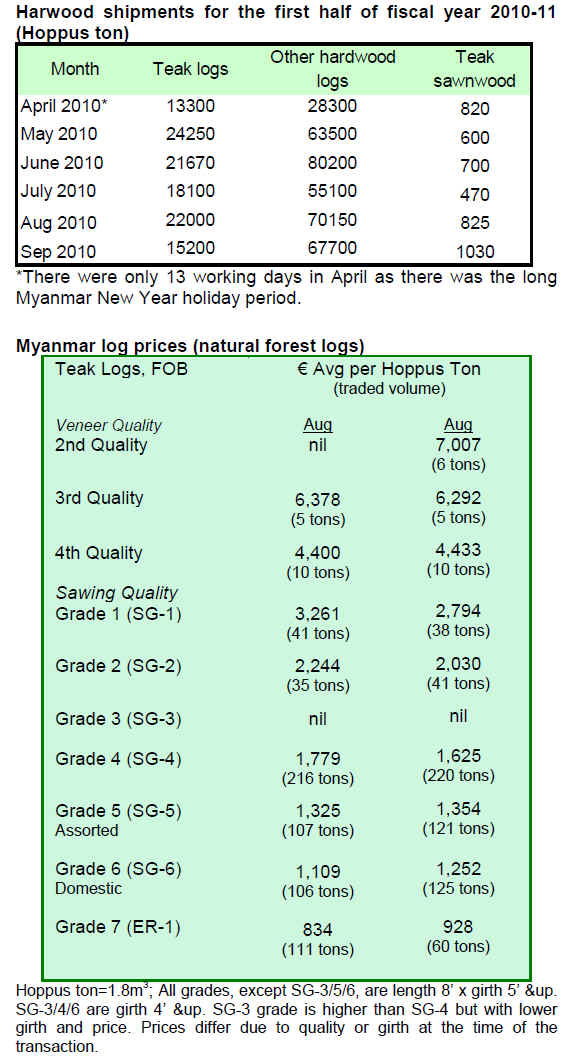

MYANMAR

Purchases of Myanmar hardwoods by country in September

Purchases of Myanmar hardwoods by country during September 2010 were as follows: Singapore (3 buyers, 88 Hoppus tons), Thailand (3 buyers, 274 Hoppus tons) and Hong Kong (1 buyer, 85 Hoppus tons). In the domestic markets there were three buyers, with timber sales totalling 177 Hoppus tons in volume.

Downward trend in shipments

Harwood shipments in the first half of fiscal year 2010-11 registered a downward trend. However, teak sawnwood exports exceeded the level of 1,000 Hoppus tons in September.

6. INDIA

Global furniture fair yields Rs.60,000 million sales

A global furniture exhibition, Index International Furniture Fair 2010, was held between 8 - 11 October in Mumbai. Altogether 700 domestic and international furniture brands were represented at the fair. During four days of exhibition, furniture sales yielded Rs.60,000 million.

Of the total brands represented, about 17% was wooden furniture. Imported furniture represented 11% of the total wooden furniture.

Large companies including Godrej & Boyce, Wipro, Zuari, Featherlite, Durian, N.R.Jasani & Co. have contributed substantially to the growth of furniture industry in India. The furniture sector in India is estimated to grow at an annual rate of 20% while that of furniture imports at a rate of 64% per year. The sector¡¯s strategy is to better meet domestic needs and also increase exports of Indian made furniture.

Domestic plywood prices revised upwards

Prices for domestically manufactured marine plywood were revised upwards again, as cost of labour, chemicals, phenolic resins and timber keeps rising. Continuing plywood shortage drives wholesalers to source plywood from overseas.

Prices of other grades of locally manufactured plywood gained as there have been less rubberwood logs for plywood production. The sharp rise in prices for natural rubber has led to a sharp drop in the supply of rubberwood logs.

7. BRAZIL

Brazilian furniture notches hefty export gains

In the period from January to July this year, Brazilian furniture exports increased 14.6% compared to the same period last year, reports Abim¨®vel. In value terms, furniture exports totalled US$434 million. The amount is close to the level recorded in the pre-crisis period in 2008.

The main export destination for Brazilian furniture during this period was Argentina, with exports valued at US$65 million, a 105% jump compared to the same period in 2009. Furniture sales to Argentina fell 42% in 2009, but exports seem to have recovered and exceeded the pre-crises level.

Furniture exports from Bento Gonçalves (RS), the largest furniture cluster in Brazil, lead the way. The region recorded a 20% increase in furniture export volume in the period from January to August this year, according to Sindm¨®veis (Bento Gonçalves Furniture Industry Association). The main destinations for furniture from Bento Gonçalves were Uruguay, the UK and Argentina.

Mato Grosso timber exports recover

According to analysts, Brazilian timber exports in 2010 are recovering. The export volume of squares from Mato Grosso state in the period from January to August 2010 was 4,286 cu.m, worth US$2.2 million. The main destination was Vietnam with a 73% share of the total square exports, followed by Indonesia (12%) and China (6.7%).

China stands out as the major destination for sawnwood with 18,275 cu.m of exports, accounting for a 37% share of the total sawnwood exports during the period. The second largest sawnwood export destination is India with a 16% share of the total, followed by the US, Hong Kong, Dominican Republic, Israel. In the period from January to August 2010, the total sawnwood export volume was 49,178 cu.m, valued at US$39 million.

During the period, the total exports of wood mouldings and plywood from Mato Grosso were 58,288 cu.m, worth US$41 million. Portugal was the major destination accounting for 35% of the total exports, followed by the US (17%), the UK (16%), Germany, Belgium, Spain, Italy and Israel.

Illegal timber seized in Mato Grosso

Since the beginning of the year, the Federal Highway Police has seized 1,519 cu.m of illegally harvested timber in Mato Grosso state. Fraudulent forest transport documents, false payment receipts, fraudulent timber volume documents and false reporting on timber species have been some of the illegal activities committed by violators involved in trade in illegal timber.

Seizures related to these violations have been increasing throughout the state. Since 2008, 5,632 cu.m of illegally harvested timber have been seized.

New forest concession in Par¨¢

The Brazilian Forest Service (SFB) initiated public hearings on the announcement of a forest concession of over 93,000 hectares in Sarac¨¢-Taquera National Forest (Flona) in Par¨¢ state. The public hearings will be conducted in municipalities in Sarac¨¢-Taquera Flona including Faro, Oriximin¨¢ and Terra Santa.

In 2009, 140,000 hectares of forest concessions in Sarac¨¢-Taquera Flona were auctioned. With the additional area, the total forest concession area in Sarac¨¢-Taquera Flona will be 770,000 hectares.

The concession area of 93,000 hectares is divided into two management units. In total, the area is estimated to produce 79,000 cu.m of timber per year. The forest concession contracts are for period of 40 years. The Brazilian nut tree areas are excluded from the concession area as these areas are for the local communities to continue their traditional use of nut trees.

The planned forest concessions are estimated to at least yield BRL4 million tax revenues annually. According to the Public Forest Management Law, the levied funds will be divided among the federal, state and local governments.

8.

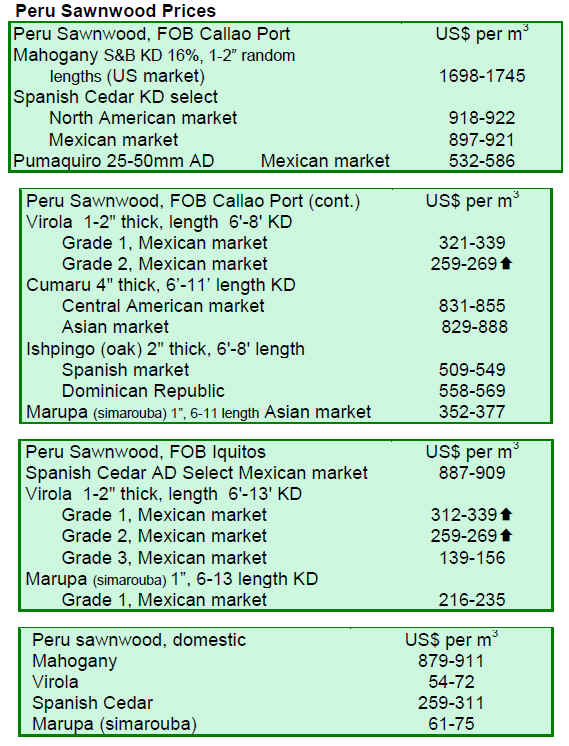

PERU

Consultations on draft forestry law conducted

The Interethnic Development Association of the Peruvian Rainforest (AIDESEP), the Confederation of Amazonian Nationalities of Peru (CONAP) and the Association of Exporters (ADEX) had a roundtable discussion on the draft Forestry Law.

At this meeting, representatives of CONAP and AIDESEP questioned some of the issues related to the territorial reorganisation, land user rights, community forest management, consultation process with indigenous people. The meeting reportedly succeeded to bring closer the views and aspirations of different stakeholders.

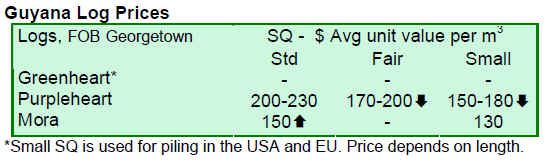

9. GUYANA

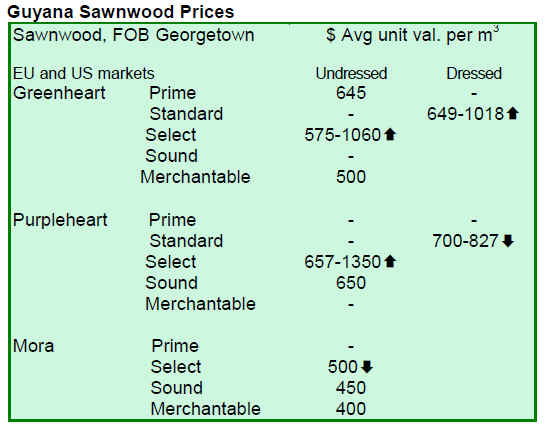

Sawnwood prices remain favourable

For the period under review, there were no greenheart log exports. Purpleheart log prices remained unchanged for standard sawmill quality, while prices for fair and small sawmill quality decreased. Mora log prices remained stable for this period.

For sawnwood, undressed greenheart (select) prices gained from US$933 per cu.m to US$1,060 per cu.m over the period under review, while prices for undressed greenheart (merchantable) remained stable. Undressed purpleheart (select) gained from US$1,000 per cu.m to US$1,350 per cu.m while mora sawnwood prices were steady.

Dressed greenheart prices inched up from US$975 per cu.m to US$1018 per cu.m. Dressed purpleheart prices were down in the period under review.

There were no baromalli plywood exports for the period under review while fair amounts of Lesser Used Species were exported to European and Asian markets as sawnwood.

Guyana¡¯s washiba (ipe) continues to be in demand attracting a price average of US$1,700 per cu.m for this fortnight period.

For roundwood, greenheart piles made a positive contribution to the total export earnings with favourable average price, with Europe and the US being the major destinations. Splitwood attracted a high price average of US$4,229 per cu.m and was exported to the Caribbean market.

For the period under review, exports of value-added products gained. The major product categories were doors (US$1,227 per piece), windows, spindles and mouldings.

Guyana mulls negotiating the VPA with EU

A workshop was held at the Guyana International Centre to address the EU Forest Law Enforcement, Governance and Trade initiative (EU-FLEGT). The workshop was a follow-up to the meeting between the European Union, the Government of Guyana, Amerindian leaders of the National Toshaos Council and several other stakeholders earlier this year on the EU-FLEGT Voluntary Partnership Agreement (VPA) between the EU and Guyana.

At the workshop, participants discussed implications of the EU measures to curb illegal logging and trade. The value of Guyana¡¯s forest product exports to the EU in 2009 was US$4.55 million. In the first half of 2010 forest products exports to the EU were valued at US$3.35 million, twice the value recorded in the same period in 2009 (US$1.5 million). Guyana¡¯s exports to the EU accounted for 14% of the total forest product exports. Exported products included dressed and undressed sawnwood, piles and splitwood but no logs were exported to the EU during the first half of 2010. The EU is the third largest market for Guyana¡¯s forest product exports after the Caribbean and Asian/Pacific markets.

According to the Minister of Agriculture, Robert Persaud, Guyana has not committed to sign any agreement with the EU since consultations are still being carried out with the indigenous people and other stakeholders. Consultations should be completed within the next three months. The Minister said that the workshop can be considered as a major stepping stone in the pathway of determining the next step in Guyana¡¯s engagement with the EU-FLEGT initiative.

The Minister added that the EU-FLEGT initiative benefits different groups of stakeholders in many ways, for example by stimulating markets, helping Guyana¡¯s exporters to retain markets, increasing reporting requirements, as well as developing chain-of-custody, forest management and monitoring at the company level.

According to the EU¡¯s representative on the EU-FLEGT initiative, John Bruneval, Guyana is on the right track but he recommended Guyana not to be rushed into any decision as there is still a need for intense debate and dialogues among all forestry stakeholders.

Related News:

|