|

1.

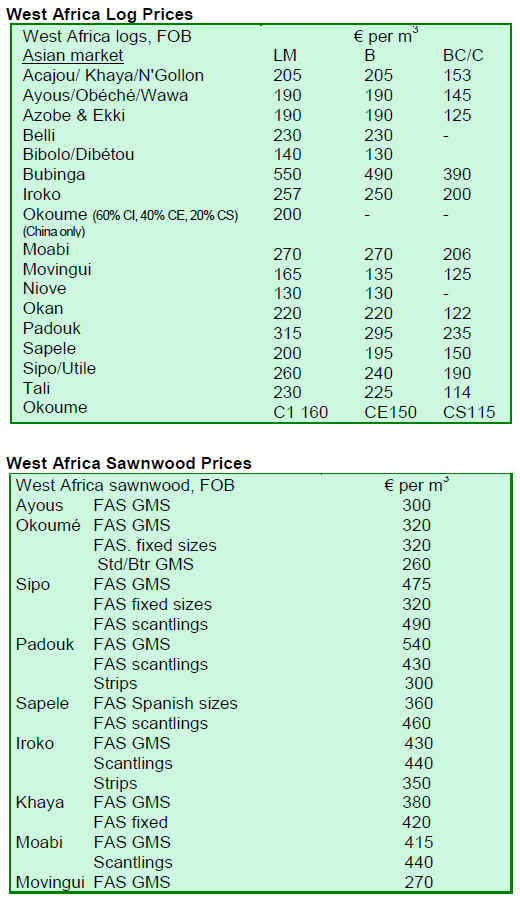

CENTRAL/ WEST AFRICA

Clarification on Gabon log ban

At a recent meeting with Gabon¡¯s Minister for Forests,

executives of the country¡¯s timber industries were advised

of the official position concerning the ban on the export of

logs that was introduced as from 1st January 2010. The

meeting was told that the ban is irrevocable.

During the discussions estimates were provided of current

log stocks. These indicate that the volume of logs already

cut in the forest, in the industry log yards and those logs

currently being transported by rail and road is in the order

of 500,000 to 600,000 cubic metres.

It has been reported that logs that are already at the port

and in storage yards (rail storage and SEPBG storage

yards) can be exported immediately by industry to fulfill

existing contract commitments. Other log stocks can be

exported, but only through the State agency SNBG and not

directly by the industry. The existing log stocks can be

exported only up until the 30th April 2010. After that date

all log exports are banned.

The meeting heard that government policy is now to be

geared towards downstream processing, beyond sawn

lumber and veneers into finished products. It is expected

the industry will have to move into the production of

mouldings, components and semi-finished products.

It was reported that government is now considering ideas

for preferential customs tariffs, import and exports tax

incentives and other revenue incentives to attract inward

investment into downstream processing facilities.

As previously reported, some producers are now

considering re-starting work to complete the construction

of mills that were in the course of construction and reopening

others that were closed because of the downturn

in sawn lumber and veneer markets.

Relaxed log exports

The Cameroon government¡¯s relaxation of exports of

secondary log species from 5% up to a notional 30% of

production is said to be in response to industry concerns

over difficult market conditions for sawn lumber that has

led to revenues falling below break-even point in the

industry.

Mills cut production

Congo Brazzaville has a tightly controlled quota system

allowing only 25% of total log production to be exported

against 75% that must be domestically processed. Because

of the current worldwide downturn in the sawnwood

markets, some operators have been forced to reduce total

production as they are unable to sell the full 75% as milled

sawnwood.

Logs from Equatorial Guinea

Equatorial Guinea had previously implemented a total log

export ban but it is now reported that some log exports are

now being allowed. However, this is not likely to be of

significant volume.

No market disruption

So far as can be determined, the Gabon log ban has not

caused any major disruption in the market. Modest price

increases for okoume logs and for okan have been reported

but prices for all other timbers have not moved to any

large extent.

The Cameroon government action in releasing for export a

larger proportion of production, plus the now clarified

position for 3 months of log exports coming from Gabon

seems to have held the market prices stable.

The clarification of the situation in Gabon now gives

importers time to assess where and how to source future

log supplies and how their processing industries will have

to adapt to changing circumstances, much as the European

trade has done in that past decade by drastically reducing

log imports.

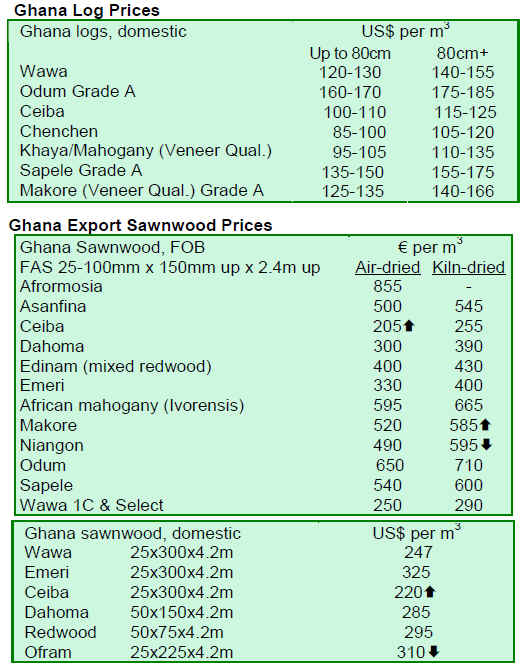

2. GHANA

Access to Global Climate Fund

The Minister of Environment, Science and Technology

has announced, that Ghana is to access a US$30 billion

global fund set aside by developed countries on climate

change. Funds would be used to implement climate change

related socio-economic activities.

The Minister said the government was in the process of

developing a low carbon emissions growth plan which

would anchor Ghana¡¯s sustainable development agenda.

According to the minister, Ghana has a low level of carbon

emissions compared to developed countries and even

when compared to the large developing countries but still

steps are needed to reduce emissions further.

The government aims to reduce deforestation and forest

degradation and has also committed one per cent of the

District Assemblies Common Fund to a massive tree

planting programme.

Economy to grow 5.7%

Ghana¡¯s economy is expected to grow by at least 5.7

percent this year, compared to the 5% achieved in 2009.

This should be possible as the global economy is

stabilising and Ghana will begin oil production this year.

The oil reserves found are estimated to contain 1.8 billion

barrels of crude oil. The government is now considering

setting up a sovereign wealth fund for some revenues

generated from oil sales.

3.

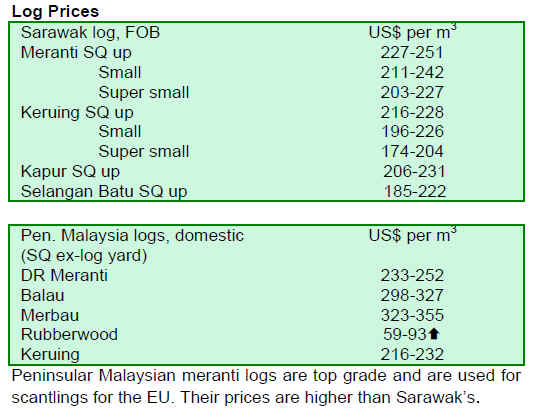

MALAYSIA

Malaysia progresses with VPA

The advisor to the Malaysian Ministry of Plantation,

Industries and Commodities said that progress has been

made in the negotiation between the European Union (EU)

and Malaysia concerning the Voluntary Partnership

Agreement (VPA).

The advisor added that further consultation between the

various stakeholders in the country needed to be held

before the agreement is concluded.

The Ambassador and Head of the EU mission commented

that, apart from a few technical issues that needed to be

resolved, he wass hopeful that VPA will be concluded

between June and July 2010.

If that is the case, Malaysia will be the first country in

Asia to conclude the agreement. It will also provide

Malaysian timber products with smoother access to the EU

market.

Timber export recovery

Malaysia is expecting commodity exports, particularly

exports of timber products, to recover in line with the

economic recovery in both the EU and the US.

Exports of Malaysian commodities declined from RM112

billion in 2008 to only RM90 billion in 2009 due to the

global economy slowdown.

Demand for Malaysian timber fell from RM22.8 billion in

2008 to RM19.8 billion in 2009.

Exporters cautious

Malaysian timber exporters are closely watching

developments in the EU and US markets. Currently

economic recovery in the two main markets is considered

weak and may not be sustained.

With the US dollar weakening against the Malaysian

ringgit, timber exporters will face a tough time in the US

market if they cannot trim prices.

In addition, because of the advantageous exchange rate of

the Chinese renminbi against the US dollar, competition

from Chinese manufacturers, especially of furniture, will

continue to be fierce.

New Year slow down

Prices of Malaysian timber products remain relatively

stable as most businesses wind down for the annual

Chinese Lunar New Year holidays.

Price increases for sawn rubberwood lead the charge as

there has been less felling of rubberwood trees because

prices of natural latex rubber continues to climb upwards.

The sharp rise in prices for natural rubber and palm oil

could lead to a sharp drop in the supply of rubberwood

logs and oil palm fibres.

A prolonged shortage of rubberwood logs may take root

and this could impact the local furniture and panelproducts

industry after the Chinese New Year holiday.

4.

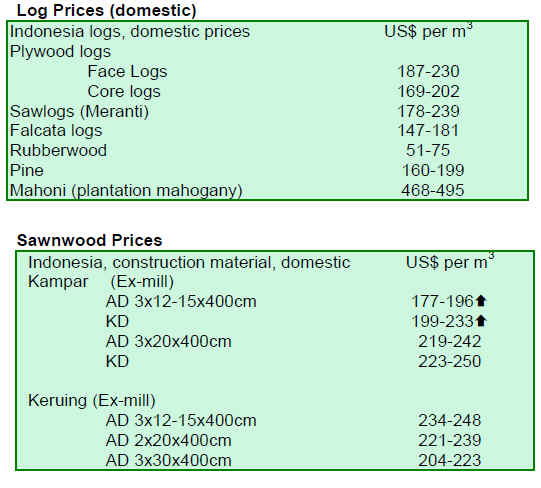

INDONESIA

Plywood push in India

Indonesian manufacturers are working hard to further

penetrate the Indian plywood market according to the

Indonesian Wood Panel Association (APKINDO).

India imports up to 16 million cubic metres of timber

annually, domestic consumption is currently around 95

million cubic metres. According to APKINDO, Indonesia

is in a strong position to compete for a bigger share of the

Indian market for 2.7 mm thickness plywood which is in

high demand in India.

Certification in Kalimantan

Reports suggest some large timber concessionaires in

Kalimantan are seeking certification as part of their

corporate governance development to try and secure a

long-term future in the sector.

Certification is also seen as a means for providing job

security as well getting production onto a more sustainable

track.

Reports indicate that some concessionaires have

approached The Borneo Initiative

(www.theborneoinitiative.org/about_tbi.html), a Dutch

non-governmental organization specializing in sustainable

forest management. This organisation apparently provides

support during the certification process which will be via

the Indonesian Ecolabeling Institute.

Up to one million ha. of forests are said to be ready for

certification, with 600,000 ha. in Kalimantan alone.

5.

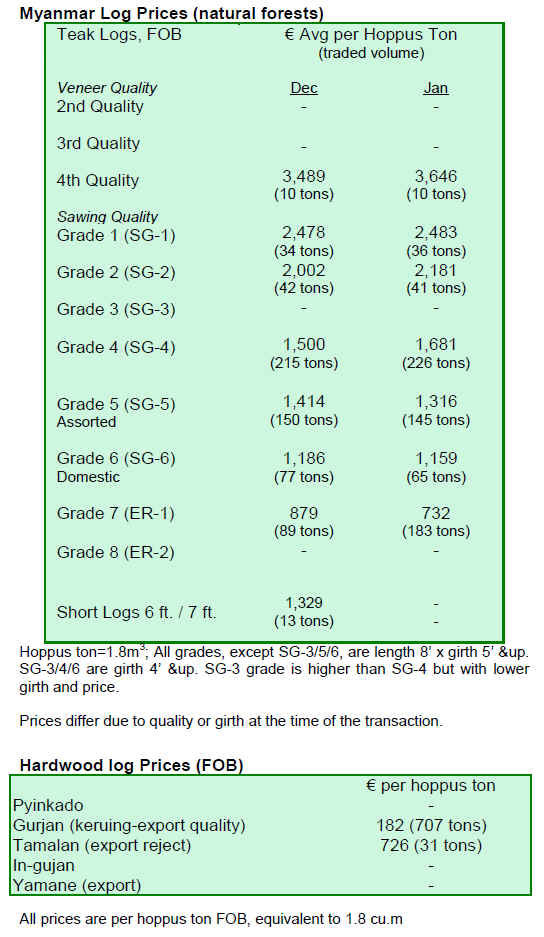

MYANMAR

Buyers now have more choice

The trade is saying that market conditions remain almost

the same as reported in January. The demand for Teak and

Gurjan remains firm and Pyinkado logs are still selling

very well.

At this time of year fresh logs have started arriving at the

log depots and buyers will now become more selective,

given the wider choice of grades.

Timber pundits often predict that buying activity will slow

down after the Myanmar New Year in April when there is

an even better choice of more fresh logs.

Demand influenced by neighbours output

Export trends in the neighbouring timber producing

countries play a crucial role in forming buyer sentiment.

For example, buyers say that prices of Pyinkado climbed

recently mainly because Malaysia and Indonesia are

selling much lower volumes of similar hardwood species

like Merbau, Balau, and Selangan Batu.

6. INDIA

Call for lower import duties

A submission to the ministry of finance by the timber

sector for changes in import duty levels in the next

national budget has been made. A reduction in the

maximum duty from 10% to 7.5% will help lower

production costs and thus make exports more competitive

says the industry.

Such a reduction would also help the government meet its

commitment to align import duties to Asean levels, say

analysts. The Indian government has progressively

reduced the import duties over the past decade and the

eyes of the timber industry are on the 26th February

deadline for the budget announcements.

Jatropha plantations

Indian Oil Co. is looking to acquire 50,000 hectares of

wasteland in various Indian states. They have reportedly

already acquired 30,000 ha. in Chhatisgarh and another

2,000 ha. in Madhya Pradesh. The company is seeking

more land in Uttar Pradesh for planting Jatropha.

Jatropha is resistant to drought and most pests and

produces seeds containing 27-40% oil. After oil extraction

the residue could also be considered for energy

production.Jatropha curcas oil has potential for biofuel production.

Government policy may involve financial incentives for

forest plantations as they will help the country meet its

carbon emission mitigation targets absorb carbon, extend

green cover and provide a bio-fuel option.

Interest in rubber plantations

With natural rubber prices having doubled in a year, from

Rs65 per kg last year to Rs128 per kg today, rubber

plantations will also get a boost. Besides rubber, the trees,

once latex yields fall to uneconomic levels, provide log

raw materials for the wood based industries.

India¡¯s trade statistics

India¡¯s log imports for fiscal 2008-9 are reported by

CAPEXIL at 3,875,300 cubic metres as against 3,931,400

cubic metres during 2007-8. Value-wise 2008-9 imports

were Rs. 51, 264 million as against Rs. 47,124 million for

2007-8 a rise of almost 9% despite the economic

downturn. Imports of sawn timber have seen a steep rise

from Rs. 1,025 million in 2007-8 to Rs. 1,449 million for

2008-9.

On the export front there has been a sharp increase (86 %)

in shipments of sawn timber and a 29 % rise in exports of

other articles of wood. These increases have helped offset

the declines in exports of plywood and wooden furniture.

CAPEXIL, a non-profit making organization, was setup in

March 1958 by the Ministry of Commerce, Government of

India to promote export of chemical and allied products

from India. And since then has been the voice of Indian

business community.

Total exports of wood and wooden products rose

marginally by 2.5 % during 2008-9 and stood at Rs. 20,

118 million as against Rs. 19, 620 million for 2007-8.

Exports of wooden furniture, mainly antique reproduction

styles are not covered by Capexil but other sources

indicate exports in 2008-9 of around Rs. 8, 000 million.

7. BRAZIL

Illegal sawnwood seized in Par¨¢

IBAMA has reported that about 800 cubic metres of

sawnwood was seized at Bel¨¦m port in mid-January. This

volume is equivalent to more than 30 truckloads and

comprised Amazonian timber species, such as quaruba

cedar, angelim, cupi¨²ba and mandioqueira.

According to the information provided by IBAMA, the

timber company involved has a history of trading in

illegally sourced timber. The company had been given a

warning in 2005 but apparently did not take any action to

comply with environmental legislation.

The market price of the seized timber was reportedly much

lower than that for timber harvested legally, this distorted

the market and made trading in legal wood products that

much more difficult.

Forest residue targets for industry

Members of the Par¨¢ Timber Exporters Association

(AIMEX) met with representatives of the State Secretariat

of Environment (SEMA) to discuss recommended

modifications to the forest licensing system in the state.

The main issue raised by AIMEX was the wood yield

conversion factor being applied. The current rate applied

was determined by the National Council for the

Environment (CONAMA) and is 45% log to sawnwood, a

rate that has been generally accepted since the application

of the 2009 State Forest Control System (Sisflora).

The current rate for forest residues is set at 13.0% but

there is a proposal to lower this to 2.25%. However,

AIMEX argues that a rate of 2.25% does not represent the

reality of the Para¡¯s timber industries.

AIMEX stressed that a federal resolution by CONAMA

established a conversion rate of 45% (log to sawnwood),

but it leaves the determination of forest residue conversion

rates up to each State.

Alta Floresta timber exports down

Data from the Ministry of Development, Industry and

Foreign Trade (MDIC) show that wood products exports

by companies in Alta Floresta dropped sharply in 2009.

Wood products are the best selling product in Alta Floresta

but sales in 2009 were low.

Exports of non-coniferous wooden parts were 6% lower in

2009 compared to 2008. In 2009 exports were worth

US$11.1 million against US$ 11.8 million the previous

year. The decline in sawnwood and veneer exports was

even greater, dropping by almost 80%; from US$ 1.9

million in 2008 to just US$363,800 in 2009.

On the other hand, exports of wood products such as

blocks, planks, strips, profiles did well in 2009 compared

to 2008.

The main consumers of wood products from Alta Floresta

in 2009 were the United States (US$6.5 million), Canada

(US$2 million) and Spain with US$1.2 million. The US

and Spain cut back their imports from the region by 14%

and 42%, respectively. Canada, in turn, expanded imports

from the region.

Timber industry on recovery path

Brazilian timber exports now seem to be recovering.

While the overall picture for 2009 was bleak, with a 45%

drop in the value of exports compared to 2008, data for

December 2009 showed a marked improvement.

Export values in December 2009 were close to the same

period of 2008 (around US$38 million). In the second half

of 2009, Brazilian timber exports were US$ 172.7 million

and although this represented a 34% drop on 2008 this was

an improvement on the first half numbers, signaling that

markets are beginning to recover after the global economic

crisis.

8.

PERU

Forest law review

The Ministry of Agriculture has decided to extend until 31

March this year, the deadline for the General Directorate

of Forestry and Wildlife to complete the updating of the

forest and wildlife law.

In July 2009, the Ministry of Agriculture launched a

review and update of the Forestry and Wildlife law within

the framework of a decentralized participatory process at

national level. The new draft law will contain proposals

for change and will be termed the National Forestry Policy

and Law Project for Forestry Policy and Law Project and

Wildlife.

Stepping up concession monitoring

The Agency for Supervision of Forest Resources and

Wildlife (OSINFOR) has started to undertake monitoring

of forest concessions, this began in Inapari, Madre de

Dios, where concessions extend to 1.2mil ha. The

monitoring began in the SAC Pumaquiro timber forest

concession located in Inapari, Tahuamanu province. Peru

has 556 forest timber concessions, covering 7.1 million

hectares and the aim is for intensive monitoring to cover

all forest concessions.

Tough stance on concessions

Richard Bustamante, president of the Agency for

Supervision of Forest Resources and Wildlife (OSINFOR)

has indicated that, following the 2009 monitoring of 78

forest concessions, it found that 46 of the 78 have

breached the concession contracts.

Because of this OSINFOR has initiated an administrative

process to address these contract breaches and some 44 of

the errant 46 concessionaires could have the concession

agreements declared invalid. The defendants could not

only lose the concession, but also could also be fined.

Some forest concessions could be declared cancelled "due

to violation of their annual operating plans and general

forest management plans, as they are removing more wood

than they should¡±.

OSINFOR president also reportedly said that "it is

necessary to take stock of the progress to date and identify

and correct the negative aspects for future concessions. In

addition, we must discuss how we can turn wood into

products with a high added value¡±.

8.

Guyana

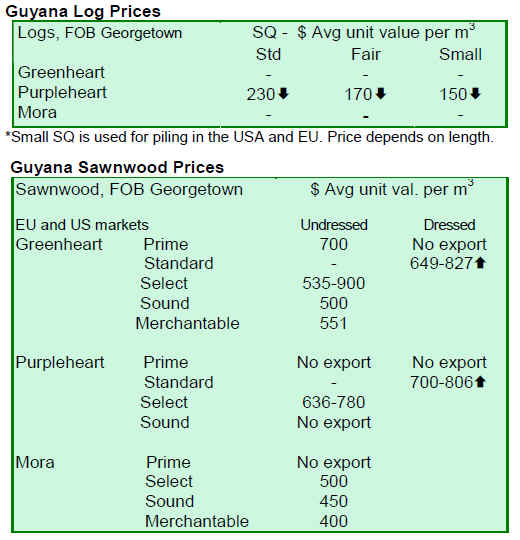

Encouraging trends continue

The positive market sentiment continues and the trend

towards more processing and lower log exports seems to

be gaining momentum. There was some trade in

Purpleheart logs and prices remain stable.

There was encouraging and positive production of rough

sawn (undressed) Greenheart, and average prices moved

up reaching as high as US$900. Sawn Purpleheart

(undressed) saw active buying for only Select grades with

very satisfactory average prices.

Mora sawnwood continues to be traded at stable prices.

Dressed Greenheart sawnwood achieved favourable prices

recently between US$742-827 which is better than during

the previous two weeks.

The demand for Baromalli plywood has been positive and

price levels have encouraged producers with

improvements in prices for both the BB/CC and Utility

grades.

For the period up to the end of January, export of value

added products has been good and this has contributed

significantly to total export earnings. The market has been

firm for products such as doors, mouldings, outdoor

garden furniture, spindles, and wooden utensils. The main

species used for added value production include

crabwood, (andiroba) locust, (courbaril) and purpleheart.

Industry reassured of support

The growing and expanding role of the Guyana Forestry

Commission (GFC) in ensuring that forests are pivotal to

mitigating climate change, will be performed without

compromising its support and promotion of the timber

industry, according to a statement released by the Ministry

of Agriculture.

Over the past two years efforts have been made to

strengthen the capacity of the GFC to address climate

change issues such as Reduced Emissions from

Deforestation and Degradation (REDD) and Guyana¡¯s

Low Carbon Development Strategy (LCDS).

However, the GFC has not lost sight of its goal of

achieving a competitive and sustainable wood processing

sector where the emphasis is on valued-added products.

The Forest Products and Marketing Development Council

(FPMDC) was established to focus on the development

production capacity and markets for wood products and to

encourage investments in the sector.

According to the Minister of Agriculture ¡°notwithstanding

our efforts in terms of looking for incentives arising from

the role our forests play in climate change mitigation,

there will continue to be a role for the forestry sector. The

changes will not affect the timber sector in any way that

will see it downsized or lead to loss of jobs or closure. In

fact, the measures will allow growth within the context of

the emphasis on sustainable forestry management.¡±

|