|

1.

CENTRAL/ WEST AFRICA

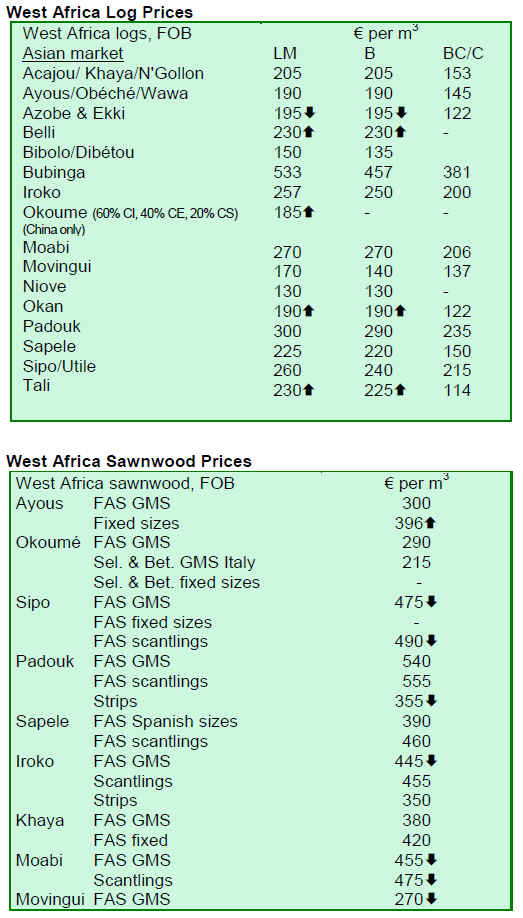

West Africa trade not likely to pick up in third quarter

West African markets remained subdued over the month

of August and little change was expected through the rest

of the third quarter. The trading pattern established over

most of 2009 continued, with an emphasis on logs to Far

East destinations, very depressed business into Europe and

no signs of recovery in the global markets for sawn

lumber. West African producers and log exporters report

good business for a limited range of log species and prices.

Where prices have hardened in recent months, these have

now firmed again with further price increases for the more

popular logs. While trade has not been brisk over the past

months, regular log shipments for China, India and

Vietnam have kept prices very steady and recent modest

gains for the most favored species have been maintained.

Some exporters report possible further small increases

because of low supply.

In Gabon, there were rumors of operators already either

running short of their log export quota allowance or even

on the brink of running out of quota altogether during

August. By mid-September, some producers in Gabon did

exhaust their allowable log export quota. As previously

mentioned, there had been protracted negotiation with the

government to increase the quotas and reports are that

several producers have now received further allocations.

At the current demand levels for export volumes it may be

likely that even these may not be sufficient to carry

through to the end of the year. Congo Brazzaville seems

also to have postponed limitations on log exports and there

is no doubt governments have relaxed intended constraints

in order to keep the timber industry solvent and maintain

employment through the difficult trading conditions.

Although most sawn lumber prices have also remained

steady overall, with very few falls in the past three

months, it is unlikely that exporters would restart sawmills

and other processing facilities or even increase production

on those still running unless and until there is a surge in

buying for Europe. Up to present there are no signs that

European business will revive even though the Continental

vacation period is now ended and importers are reviewing

trade prospects for the autumn and winter. Building and

construction activity have not improved, the downturn has

been fairly evenly spread across Europe, Spain and UK

possibly the worst hit.

Sawn lumber is in the doldrums and business with Europe

has been very dull as the usual autumn surge in purchases

by UK and Continental European buyers has not occurred

this year. Although the UK construction industry is said to

be more active, this has not so far translated into new

timber imports and at this time the only reasonably bright

spot is Italy where there has been over the past months,

and is, a steady level of imports of favorite species in logs

and lumber. Sawn lumber prices have changed a little for

the very few species that are being actively traded, while

the majority have kept steady over several months through

the absence of demand or extremely low offtake matching

the very low level of production and low stocks at

producer mills.

Cameroon reports heavy rains hampering production and

Gabon producers are expecting early onset of the rainy

season.

2. GHANA

TIDD contact volume jumps nearly 21%

According to the Timber Industry Development (TIDD)

Division of the Forestry Commission (FC), a total contract

volume of 129,580 m³ of wood products and 5,388 pieces

of furniture were processed and approved during the

second quarter of the 2009. These compared to the first

quarter of the same year show increases of 20.9% in the

total contract volume for wood products. The timber trade,

which was severely hit by the global economic slowdown

during late 2008, has shown signs of recovery from the

crises as shown in figures since October 2008.

All the major products experienced significant increases in

volume. Teak poles/billets/logs/lumber, plywood, sliced

veneer, and mouldings/processed lumber increased by

44%, 56.5%, 31.3%, and 124.5% respectively as compared

to the previous quarter figures to reflect volumes of 52,377

m³, 41,216 m³, 8,371 m³, and 4,163 m³. There was a

marginal increase of 2.1% for rotary veneer by volume

(3,795 m³) when compared to figures for the previous

quarter, although the market was generally down.

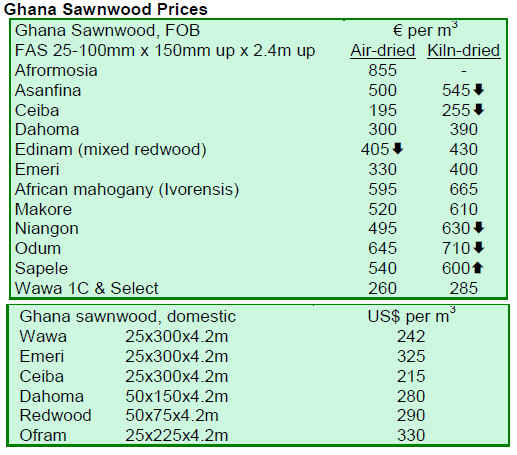

Price levels improve during second quarter

During the quarter under review, timber and wood product

exporters found it difficult to achieve the Guiding Selling

Prices (GSP) of the TIDD. However, the general price

levels achieved were much better when compared to those

achieved during the first quarter.

Prices of mahogany (Khaya Ivorensis) sawnwood

improved significantly during the quarter under review.

There were improvements of between USD60 and

USD80/m³ from the previous quarter. Prices reached

USD700/m³ and USD720/m³ for 25mm thickness, though

still falling below the GSP of USD788/m³. Wawa also

improved during the quarter under review although the

improvement was dependent on the exporter and the

volume involved. Many of the large scale and wellestablished

companies such as Logs and Lumber Ltd., the

Naja David Group of Companies, John Bitar Company

Limited and other medium scale companies were able to

achieve the GSP, and even above in most cases, small

scale companies found it difficult to achieve the GSP.

While the former were achieving between EUR5 and

EUR15 more on the GSP of EUR282/m³ for 25mm

thickness, the latter were achieving between EUR5 and

EUR18 below the GSP.

For the main species to the Middle East market, only the

dahoma showed signs of improvement, while prices of

edinam, danta, candollei, and mahogany

(Anthotheca/Grandifolia) did not improve during the

quarter under review. Prices of dahoma were up by

between USD10 and USD20/m³ in most cases from the

previous quarter.

The market for odum which had been generally down

since the middle of 2008, showed signs of recovery. A

significant number of contracts were submitted during the

quarter under review though prices were still EUR20 and

EUR45 below the GSP of EUR665/m³ and EUR670/m³

for 25mm and 50mm respectively. The US markets saw

some improvement, with the main buyers (Baystates Inc.,

MBS Trading and Munro Brice) signing contracts with

encouraging prices during the quarter under review.

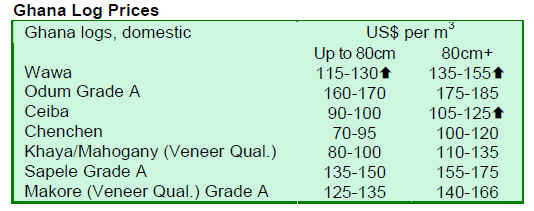

Second quarter exports slump

Ghana¡¯s timber exports trade declined as exporters traded

in few volumes of timber and wood products. For the first

half of the year ended June 2009, the value of exports

slumped by 35% as the result of a 30% fall in the export

volume of timber and wood products, when compared to

the same period last year. Total value of timber exports for

the first half of June 2009 was EUR62.72 million as

compared to EUR96.50 million, as shown in the table

below:

During the period under review, most products recorded

losses both in export volume and value. Ghana¡¯s trade

with African markets for the period under consideration,

however, increased in both volume and value. Total

revenue increased to EUR27.49 million (43.8%) in 2009,

from EUR22.05million (22.8%) in 2008. Ghana¡¯s trade

with major markets in America and Europe also declined

during the period, attributed largely to limited cash flow of

most buyers in these countries. Logging activities from the

forest was also difficult due to the rainy season.

3.

MALAYSIA

Malaysia expects to reach furniture target

According to Bernama, the Malaysian government says it

is confident the country will be able to achieve a RM10

billion export target for its furniture exports by the end of

2009. The country has already registered RM3.57 billion

in furniture exports for the first half of 2009 compared to

RM4.11 for the same period last year.

To further promote its furniture products, Malaysian

traders will participate in the upcoming Malaysian

Furniture and Furnishings Fair. Its organizing chairman

Gan Tai Hwa expects total sales turnover is projected to

increase to RM50 million this year compared with RM40

million registered in last year¡¯s fair.

Rubberwood gets a boost from latex demand

The continual usage of rubberwood as the main raw

material by the furniture industry has captured the

attention of investors, who are now interested in the

cultivation of rubber trees on a very large scale. One of the

latest joint ventures in the rubber plantation business by

the private sector involves Guangdong Guangken Rubber

Group, from China, and Bornion Timber Sdn Bhd, from

Malaysia, a 12,000 hectare rubber tree forest plantation

estate in Sabah with an initial investment of RM230

million.

Rubber experts claimed in The Star that those who have

invested in rubber tree plantations could expect an internal

rate of return (IRR) of up to 12.8% from rubberwood

alone. Over a 15-year period and with latex production

factored in, the IRR could reach up to 13.7% in

comparison with other plantation forest species, which

yield an IRR ranging from 5.1% to 15%. The IRR of

rubber tree plantations is comparable to the IRR of oil

palm plantations, which stands at 15.6%.

Companies undertaking new forest plantation projects in

Malaysia are provided a 10 year tax holiday beginning the

first year the company begins to make a profit. Those

involved in reinvestments will receive five years tax free

beginning the first year it makes a profit.

4.

INDONESIA

Indonesia works to approve S4S exports

The Indonesian government is working on a plan to

legalize the exportation of S4S (surface-machined to a

smooth finish on all four sides) categories of wood and

logs from natural forests, which are currently banned, in

an effort to boost revenue from the forest products

industry. Indonesian officials are of the opinion that

despite of the current global economic crisis, there is

demand for S4S and log products in particular markets,

especially in the Middle-East. Officials added that

countries like Malaysia and China had benefited from

Indonesia¡¯s absence in the global market.

The Jakarta Post reports that the Ministry of Forestry has

set quotas allowing harvesting of up to 9 million m³ of

logs per year. However, official statistics state that only 3

million m³ of logs actually entered into production.

Officials are questioning whether the remaining 6 million

m³ was harvested and processed illegally, including to

process products into S4S. Conservationists and a number

of NGOs noted that the Indonesian government must

improve on a mechanism that allows for transparency and

good governance in forestry management before

embarking on a plan to legalize exportation of S4S.

5.

MYANMAR

Community forestry plantation boosts agarwood

availability

A community forestry plantation situated about eight miles

from Myitkyina, Kachin State, in Northern Myanmar was

established under a directive from the Ministry of

Forestry¡¯s aims to replenish agarwood (Aquilaria

agallocha- Thymelaeaceae family) saplings. As reported in

The New Light of Myanmar, agarwood is considered to be

on the verge of extinction. The community forestry

plantation had started sowing agarwood seeds in April

2008 and by June 2009 planted 12 acres. About 500 acres

are expected to be planted under the initiative.

The seeds for the plantation were initially collected from

trees in the nearby villages. About 100,000 seedlings were

planted last year and sold to those interested in

establishing plantations at the rate of Kyats 500 (about 50

US cents) per sapling. The Ngwe Pyaw Agarwood

Plantation expects to plant another 100,000 seedlings this

year. About 500 trees with a spacing of 10 feet by 10 feet

can be planted per acre.

Agarwood trees are injected with microbes at three years,

and can be utilized at five years. Old agarwood trees in

nearby villages have straight boles and can grow up to

about fifty feet in height. Agarwood is known to have

medicinal properties and is highly popular in the Middle

East. Prices are reported to vary up to USD20,000 per

kilogram.

Plans designed to restore tidal forests

According to the Flowers News Journal, plans are being

drawn up to rehabilitate tidal forests in the Tanintharyi

Division. Records show that in 1980 the tidal forests

extended to 647,571 acres. However, the area only

spanned 587,776 acres in the year 2000 and 489,025 acres

in 2008. Deforestation levels between 1980 and 2008 are

attributed to human intervention such as the establishment

of embankments and subsistence farming in the lowlands;

expansion of fish farms; and fuel wood and charcoal

production. Plans are now underway to rehabilitate

mangroves that have been cut for various purposes and to

provide effective protection the remaining tidal forests,

thereby preserving the flora and marine life.

Tidal forests are to be found in Ayeyarwaddy, Yangon,

and Taninthatyi Divisions and in Rakhine and Mon States.

The largest areas of mangroves are to be found in the

Rakhine State, Ayeyarwaddy Division and the

Taninthatryi Division.

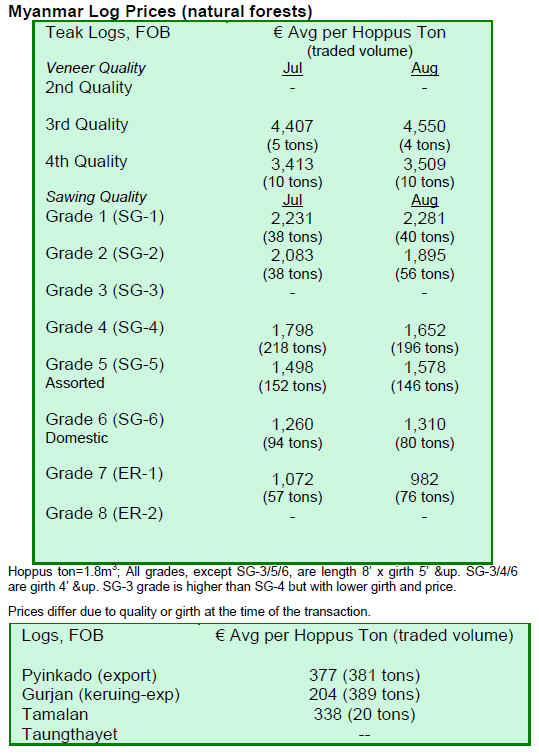

Market situation in Myanmar continues to be slow

The market situation remains as it was in July except some

buyers reported a glut of pyinkado logs in Vietnam.

Shipments to Vietnam are weakening. Teak was being

shipped to India and the Indian teak market was reported

to be quite firm.

6. INDIA

Expansion of Special Economic Zones to increase wood exports

Annual tree planting programmes have been quite active

in many Indian states during 2009. Forest departments of

all states, non-government organizations (NGOs) and

members of the public have planted a large number of

saplings of teak, eucalyptus, casuarinas, poplar, leucanea

leucocephala, Dalbergia sissoo Bamboo and other species

by local wood-based industries. In certain areas, emphasis

has been on planting fruit and shade giving trees.

Sandalwood is also an important but rare species. Recent

reports indicate that the number of sandalwood trees has

increased in the Marayur sandalwood division from

57,767 to 58,514. There has been sufficient regeneration

of this species in the wild and vigilance and protective

measures by local forest departments have shown to

reduce smuggling cases as well.

India¡¯s Foreign Trade Policy for the period 2009-2014 has

been just announced. In the new policy, the government

looks forward to achieve an annual export growth of 15%

over 2010-2011 with a target of USD 200 billion by

March 2011.

Special Economic Zones are expected to produce goods

for export. The first wood-based products areas will be

established in the State of Gujarat close to two of west

coast ports Kandla and Mundra. Timber processing zone

with about 400 licensed saw mills and about 35 plywood

units exists in the same district, providing direct

employment to 40-50,000 people. The planned size of the

SEZ is 100 hectares and is expected to attract Rs.10 billion

in investment for wood-based industries.

Indian exporters and industry will benefit from the

recently signed Association of South East Asian Nations

(ASEAN) Free Trade Agreement as it will eliminate

import duties on over 4000 items in intra-regional trade in

ASEAN markets. The measures are expected to enlarge

volumes traded and boost economic return for all the

participants. Under the new Agreement, India can export

more units of plywood, MDF, particleboard, but is limited

by availability of raw material. This FTA has generated lot

of optimism and opportunities.

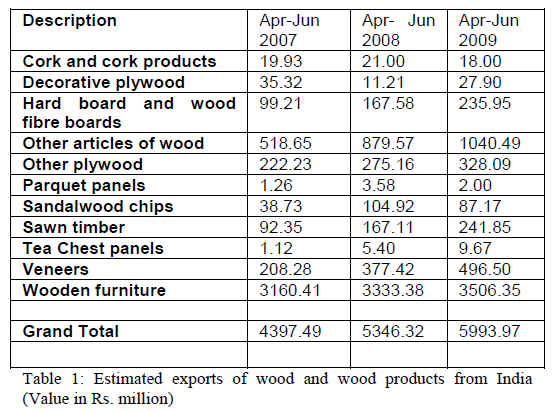

The global recession has affected India¡¯s imports and

export levels. In fact imports have declined more than

exports so trade balances are being well managed. Exports

of wood products are performing better than the second

quarter of 2008. A comparison of figures is presented

below:

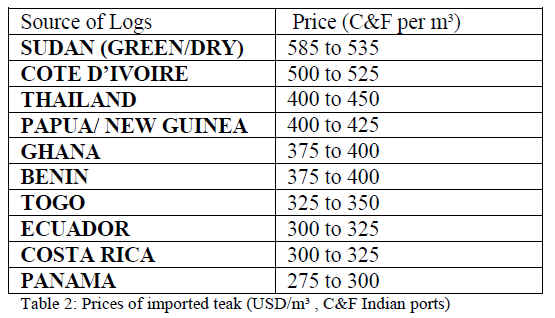

Teak prices show firm price trends

Teak prices have been strong over the last fortnight.

Below are countries which export teak to India (from

sources other than Myanmar) at current C&F prices for

Indian ports:

7. BRAZIL

Para authorities discuss alternatives for timber production

The government of state of Par¨¢ and forest sector

entrepreneurs have come up with alternatives for the

timber production chain. In August 2009, the State

Secretary of Development, Science and Technology

(SEDECT) discussed the main shortcomings of the sector.

Representatives indicated that the Forest Management

Support Program (PAMFLOR) could help promote forest

industry. According to Ag¨ºncia Par¨¢, the program aims to

improve sustainable forest management in Par¨¢ with more

transparency, stronger management, and greater

environmental control over forest resources. The

government, entrepreneurs and research institutes are

expected to be part of an independent and integrated

network system to increase the capability and swiftness of

the State Secretary of the Environment (SEMA) in the

process of analyzing and monitoring forest management

projects. PAMFLOR will provide a system of remote

monitoring and independent verification of forestry

practices in the field; technical assistance; capacity

building and training; technological improvements in

forest industry; and, production of studies that provide

strategic information on the forest sector.

New research aims to map wood production

A study carried out by the Economics Department of the

State University of Mato Grosso (UNEMAT) aims to map

the wood production processes in the Amazon region. The

purpose is to check the volume of wood residues produced

by the forest activities (furniture and timber industry) and

its potential as an alternative source of income. There are

many types of wood residues subject to utilization because

they may harm the environment and cause problems such

as forest fires. The alternative is to diversify the work and

income sustaining small companies and cooperatives.

The data collection for the completion of research is

expected to end by mid-July of 2010, reported S¨® Not¨ªcias.

According to the proposal, the data collection will take

place in an area equivalent to 400 to 500 km². The Timber

Industry Association of Northern Mato Grosso

(Sindusmad), the Brazilian Support Service for Micro and

Small Enterprises (Sebrae) and Fapemat (funding agency)

are partners on this initiative. For the coordinators, the

Northern region has potential to transform wood residues

(sawdust, wood chip and others) into manufactured

products for commercialization.

The map being prepared in the region shows that only in

Santa Carmen (since the beginning of timber exploitation)

over 100,000 tons of wood waste has been produced. In

Marcelândia, such a figure tops 10 million tons.

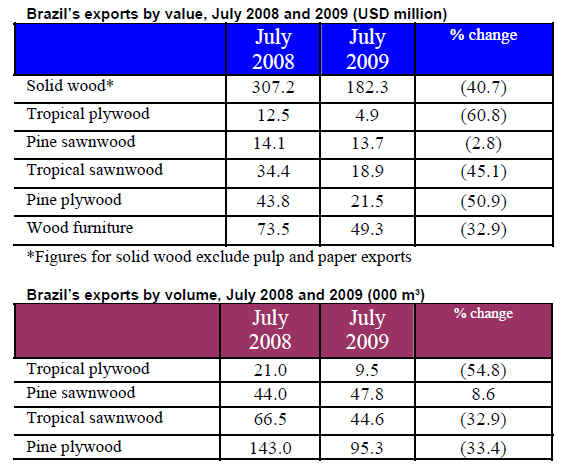

Brazil¡¯s exports show no sign of improvement

Brazil¡¯s wood products exports for July 2009 (except pulp

and paper) plunged 41% by value, nearly the same amount

as in June 2009, compared to the same period in 2008. The

charts below show the volume and value of Brazil¡¯s

exports for July 2009 compared to the same month a year

earlier:

Timber exports decrease in Roraima

Few timber companies in the Amazon meet the

environmental and labor law requirements of Brazil. In

Roraima, out of 54 timber companies, only one exports

certified wood mainly to the European market. The

business sector argues the global financial crisis is the

main factor that leads them to abandon plans for

certification, indicated Portal Amazônia.

To avoid uncontrolled deforestation, mainly in the

Amazon, some measures have been established to

stimulate investors¡¯ interest in self-sustaining actions.

Forest certification is one of them and serves as a passport

for companies that export processed timber.

Certification is a guarantee that timber companies comply

with forest management requirements. For instance, rare

or young trees are kept intact and are replanted every 25

years to allow forest regeneration. In the first half of 2008,

companies in the state of Roraima exported about USD

5,536 million. This year, in the same period, exports fell to

USD4,674 million. According to the Timber Industries

Union, this fall was due to the international financial

crisis.

Biom¨®vel seeks to boost Northern Santa Catarina¡¯s competitiveness

According to Ag¨ºncia Sebrae de Not¨ªcias, most furniture

companies of the Northern Santa Catarina region used to

export 100% of its production from 2003 until 2008.

However, the global economic slowdown that began last

year reduced exports by 50%.

The region produces high quality furniture, made of solid

wood and following strict European quality standards, but

adverse exchange rates resulted in a loss of

competitiveness. One of the solutions to reverse this

situation was to shift production to the domestic market, a

measure promoted by the Local Productive Furniture

Arrangement (LPA) of the Northern Santa Catarina.

To further promote products from the region, 27

companies in the region created a label called ¡®Biom¨®vel¡¯,

launched in May 2009 to promote the concept of

sustainability in their products. To apply for the right to

use the label Biom¨®vel, a company must be a member of

the LPA Northern Santa Catarina and are subject to the

evaluation of a certification committee, the Conformity

Assessment Body.

The creation of this concept has come as a result of

extensive research on certification processes already used

by furniture manufacturers in other countries and by other

sectors. The strategy of Biom¨®vel integrates all levels of

product development, by linking competitive advantages

such as utilizing materials from planted forests and

reducing waste and producing environmentally friendly

products.

8.

PERU

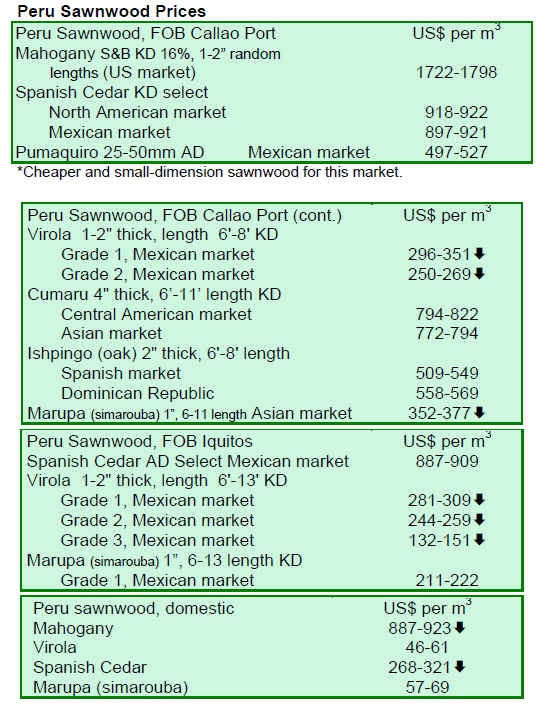

Peru¡¯s wood exports plummet 45%

According to the Export Association of Peru (ADEX),

wood exports from January to June 2009 were valued at

USD66.01 million while for the same period in 2008 were

USD119.76 million, a drop of 45%. The three main export

destination markets were China, Mexico and the US,

which together represented nearly 78% of wood sector

exports. The Bolivian market increased its imports and

New Zealand¡¯s market continued to grow. On the other

hand, Mexico curtailed its imports by 71% following a

substantial reduction in imports of mouldings. China,

Mexico and the US all reduced their imports in the month

of June 2009 when compared to the same month of 2008.

In contrast, Venezuela increased its imports of 56% in the

month June 2009 compared with the same month 2008.

Semi-manufactured products during the period comprised

40.2% of wood exports worth USD26.54 million. The

main destination market for products from this sub-sector

was China. Hong Kong SAR also increased it imports of

semi-manufactured products by 80.7% in the same period.

Sawnwood amounted to 36% of wood exports in the

sector, although overall exports fell 58% by value from

2008 levels. Exports of veneer wood and plywood for the

January ¨C June 2009 period were USD6.96 million, about

55% less than the same period in 2008.

Exports of furniture and parts also dropped to USD3.66

million by value in 2008. A large drop in demand from the

US contributed to the overall 47.7% decrease in wood

exports by value.

9. BOLIVIA

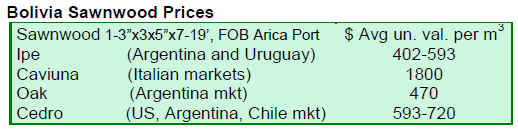

FSC covers over 2 million hectares of Bolivia¡¯s forests

Bolivia is the world leader in voluntary forest certification

with more than 2 million hectares certified in tropical

forests. According to the FSC, Bolivia¡¯s FSC certified

wood products exports are worth about USD16 million

annually, about 25% of total wood products. Only those

organizations or companies with chain of custody

certification can use FSC stamps in their products.

The FSC has an international office located in Bonn,

Germany, four regional offices (Europe, America, Africa

and Oceania - South East Asia) and a network of National

Initiatives. In Bolivia the FSC National Initiative is the

Bolivian Council for Voluntary forest certification - CFV.

10. MEXICO

National Forest Agency sees change of leadership

On 1 September 2009, Emilio Flores Dominguez was

appointed as the new Attached General Director of the

National Forest Agency (CONAFOR), replacing Carlos

Rodriguez Combelles, who is retiring from public service.

Flores was Federal Deputy in the National Action Party in

the LX Legislature, where he was part of the committees

of Environment and Natural Resources and Public

Finance. During his tenure as Federal Deputy, he

introduced various initiatives for the protection of wildlife,

aquifers and forests. He previously served as

commissioner of Banobras in the state of Chihuahua for

nearly four years. The National Forest Agency was created

as part of a decree that states gives the Attached General

Director clearance to conduct CONAFOR¡¯s affairs in the

absence of the General Director.

Drought and arid conditions affect reforestation processes

The prolonged drought and lack of rainfall in large parts of

Mexico have affected the process of reforestation. Given

this situation, the CONAFOR has postponed the

establishment of nurseries where the drought continues.

As part of the ProTree program, about 25% of the

seedlings dedicated to reforestation in 2009. CONAFOR

expects that rainfall conditions be regularized in order to

meet the goals of reforestation programs at national and

state level. Otherwise, the plant would be sheltered in the

country¡¯s forest nurseries.

Reforestation in the rural colony of Los Lirios, in the city

of Chihuahua, has been particularly high during the second

half of July this year. It was feared that a scenario of low

rainfall could present a similar drought occurred in the

summer of 1997 or 1982.

11.

Guyana

Greenheart continues positive gains

A comparison of the present period (16 ¨C 31 August 2009)

and previous fortnight reveals a significant increase in the

prices for Greenheart logs. Greenheart small sawmill

quality and Purpleheart standard sawmill quality maintains

price stability. India was the main export destination

attracting logs. Both dressed and undressed sawnwood

prices have been very positive. Dressed greenheart has

shown a positive increase (1150/742 USD) for the period

16 ¨C 31 August 2009 when compared to the previous

fortnight in August. However, dressed purpleheart remains

firm. Roundwood prices were favorable the second half of

August against the previous period. Splitwood prices

showed positive increases for the period 16 ¨C 31 August

2009 when compared to the previous period (1st -15th

August 2009). Plywood prices for the BB/CC and utility

category have increased significantly for this period in

comparison to the first half of August.

Indoor and outdoor furniture and doors have revealed

higher prices for the second half of August while

mouldings, spindles, windows and wooden utensils and

ornaments also contributed to value-added products that

gained significant export value earnings for these

products.

FPDMC strengthens ties with forest industry

A recent consultation held between the Forest Producers

Association (FPA) and the FPDMC resulted in discussions

on areas relevant to Guyana¡¯s forest industry.

Collaborative efforts are being made between the Guyana

Forestry Commission (GFC), the FPDMC and the FPA to

improve on export of wood and wood products in Guyana.

Eight Lesser Used Species (LUS) recently tested have

shown comparable properties with the more popular

species and have been accepted in accordance to ITTO

standards. Currently three of them are among the top ten

exports from Guyana to international markets. This has

resulted in part from a pro-active initiative undertaken by

the FPDMC to support the GFC in the initiative to

increase an awareness of the Lesser Used Species (LUS)

of accepted standards. Additional efforts by the FPDMC

are in progress in the areas of promotion and marketing of

LUS.

During the consultation it was noted the next phase in the

LUS promotion program would encourage local lumber

yards and traders to stack and sell LUS. It is anticipated

that eight additional LUS and their abundance will be

identified and quantified in the near future.

Another initiative that is supported by the FPDMC places

emphasis on industry efficiency and product development

within the sector. In order to achieve this, efforts to train

persons working in the sawmilling industry has

commenced and will be ongoing. In-house training will be

embarked upon in the near future in areas such as mill

design, saw doctoring and quality control.

|